キャプティブ 2020.04.09

CA12 キャプティブのためのリスクマネジメント Risk Management for Captives

目次

Copyright © Shinichiro Hatani 2020 All rights reserved

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

「キャプティブを設立したい」という企業に対して、「では、まず、リスクマネジメントをおこないましょう」とお伝えすると、「リスクマネジメントの目的は、リスクを全部分類して、その対処方法をすべて考えることですね?」という質問がほぼ100%返ってくる。リスクマネジメントをこのように考えている企業が実に多いことに気づかされる。

「企業、環境に潜在している、もしくは、既に顕在化しているリスク」を分類していくと大小合わせて100以上あるのが普通である。それらすべてに対策を講じる作業をしていくと、何年も掛かるものである。

しかし、リスクには、数十年に一度程度しか起こらず、かつ起きた時の損害額も数十万円程度と予測されるものも多い。リスクマネジメントをおこなう際に一番重要なことは、「優先的に対応すべきリスクを10~20洗い出すこと」であり、そのためにリスクを「定量化(見える化)」する作業をおこなうことである。

定量化のファクター(要因)は「リスクの発生確率」と「リスクの強度」であり、これらを基にリスクをマッピング、優先的に取り組むべき、つまり、企業に「かなりの高い確率」で、「かなりの強度」を与えるリスクを特定して、対処策を検討することである。

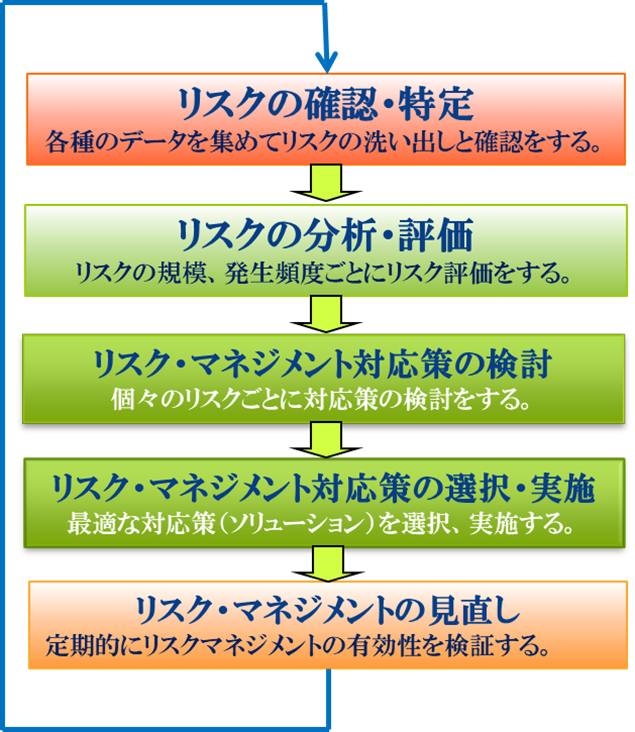

1.リスクマネジメントのステップ

企業や団体は、さまざまなリスクに遭遇、また自らの組織のなかにリスクを内包している。このリスクを予測、検証、対処方法の検討・決定をしていく作業が、リスクマネジメントである。リスクは、とかく「危険なモノ」と考えられ、その除去に多くの人は関心を持つが、リスクは、的確な分析と評価、そして対応をおこなえば、決して「除去すべき存在」としてではなく、むしろ「事業収益を産み出す存在」にさえ変化させていくことが可能である、「Turning Risk to Profit®」(リスクの収益化)は可能であるとグローバル・リンクは考えているからであり、現実にグローバル・リンクのお客様は、「的確なリスクマネジメントをおこない、ソリューション・キャプティブ®を設立したことによってこのことを現実化しているから」である。

そのような視点で、優先対応を決めたリスクごとに下図のプロセスで、リスクマネジメントをおこなっていく。ここで、留意すべき重要な点は、一旦選択、実施したリスクマネジメント対応策も、事業や活動の進展、変化にともない、また「想定外」の事態を惹起させないためにも、その有効性と適格性の検証をその後も定期的に専門家とともにおこなっていく必要があるということである。

2.リスクの種類

前述の通り、一般的に企業、団体が内包、また遭遇しているリスクは100以上あるが、リスクマネジメントをおこなう際、分類しやすいように、その代表的なリスク分類の一例を挙げる。

A. 災害・事故などのリスク

1.自然災害

①台風・高潮、②水災・洪水、③竜巻・風災・落雷、④地震・津波・噴火、⑤天候不良・

異常気象

2.事故

①火災・爆発、②停電・インフラ麻痺、③交通事故、④航空機事故・列車事故・船舶事

故、⑤設備の不備による事故、⑥労災事故、⑦建設中の事故、⑧運送中の事故・海賊、

⑨盗難・不法侵入、⑩放射線汚染・放射線漏れ、⑪有害微生物、⑫細菌の漏えい、⑬バ

イオハザード、⑭ネットワークシステム故障、⑮コンピューターウイルス・サイバーテ

ロ、⑯コンピューターデータの消滅B. 経営に関するリスク

1.経営

①敵対的M&A、②企業買収・合併・吸収の失敗、③新規事業・設備投資の失敗、④経

営者の死亡、⑤経営層の執務不能、⑥乱脈経営、⑦グループ会社の不祥事、⑧顧客から

の賠償請求、⑨金融支援の停止

2.知的財産権

①著作権侵害、②特許紛争、③商標権侵害

3.環境

①環境規制強化、②環境賠償責任・環境規則違反、③環境汚染・油濁事故、④廃棄物処

理・リサイクル

4.製品・生産

①瑕疵、②製造物責任、③リコール・欠陥製品、④海外生産拠点の停止、⑤生産技術革

新による自社製品の劣後化

5.労務

①差別(国籍、宗教、年齢、性)、②使用者責任、③労働争議・ストライキ・デモ、④

エイズ、伝染病・新型インフルエンザ等による「パンデミック」、⑤集団離職、⑥従業員の過労死・過労による自殺、⑦外国人不法就労、⑧従業員の雇用調整、⑨従業員の高齢化、⑩海外駐在員の安全、

⑪産業スパイ

6.コンプライアンス

①独禁法違反・カルテル・談合、②金融商品取引法違反、③会社法違反、④巨額申告漏

れ、⑤プライバシー侵害、⑥情報管理の不備・顧客情報漏洩、⑦役員賠償責任・株主代

表訴訟、⑧役員のスキャンダル、⑨セクシャルハラスメント・パワーハラスメント、⑩

不正取引・詐欺・横領・贈賄・収賄、⑪各種法令・条例違反

7.財務

①デリバティブの失敗、②取引先倒産、③格付けの下落、④不良債権・貸し倒れ

8.マーケティング

①開発製品の失敗、②競合・顧客のグローバル化、③市場ニーズの変化、④価格戦略の

失敗C. 政治・経済・社会リスク

1.政治

①法律の制定・制度改革・税制改革、②国際社会の圧力、③貿易制限・通商問題、④戦

争・内乱

2.経済

①経済危機・景気変動、②株価変動・為替変動・金利変動・地価変動、③原料・資材・

原油の高騰、④格付けの下落

3.社会

①テロ・暴動、②誘拐・人質、③反社会的勢力による脅迫、④インターネット

を用いた批判・中傷、⑤マスコミによる批判・中傷、⑥マスコミ対応の失敗、⑦宣伝・

広告の失敗、⑧風評、⑨不買運動・消費者運動・地域社会との関係悪化、⑩人口減少・

少子化・労働力不足

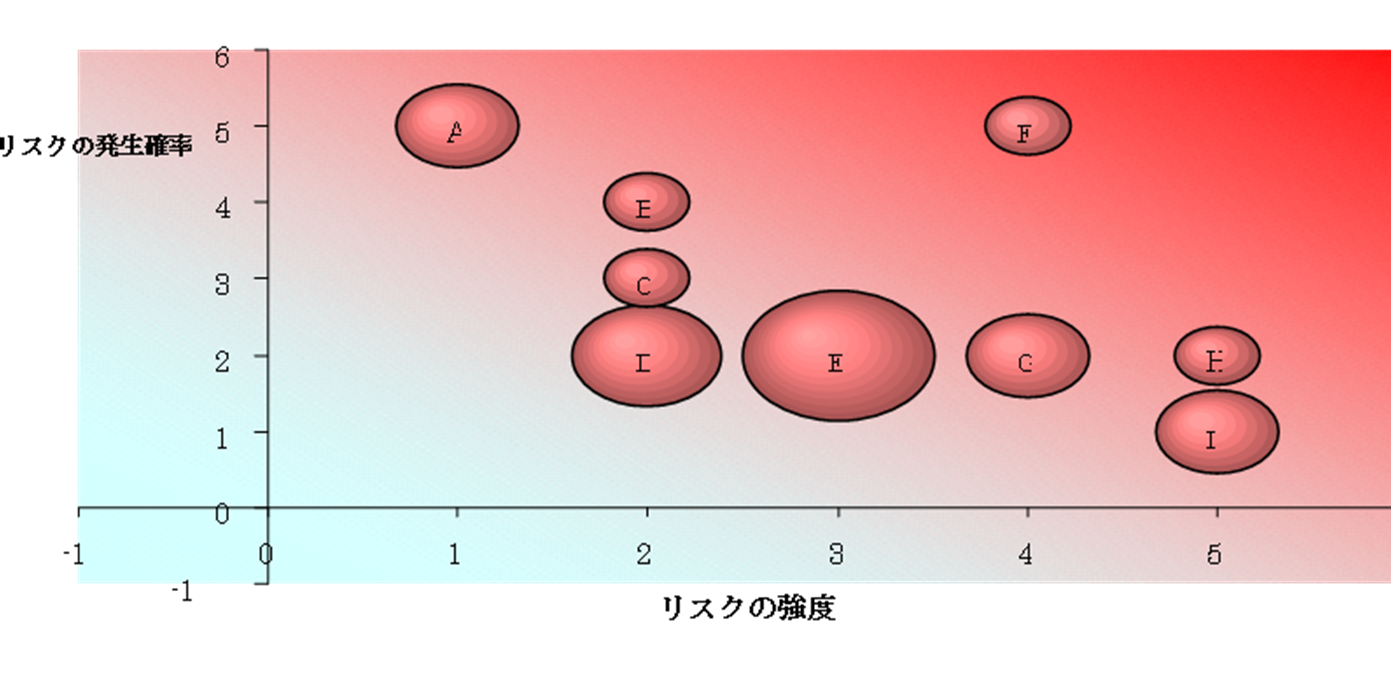

3.リスクマッピング

これらのリスクのうち、先に述べたとおり、10~20のリスク、それらを下図のようにマッピングして「見える化」をしていくとリスクの実態により近づいた判断が可能となる。

企業によっては、既にリスクマネジメントを実行しているため、大きなリスクの数が減少している企業もある。

下図は、グローバル・リンクが、以前おこなった実際のリスクマップであり、キャプティブを設立して3年が経過、毎年リスクマネジメント委員会の主導で全社リスクマネジメント運動をおこなってきた成果で、当初20以上あったものが、9になったケースである。

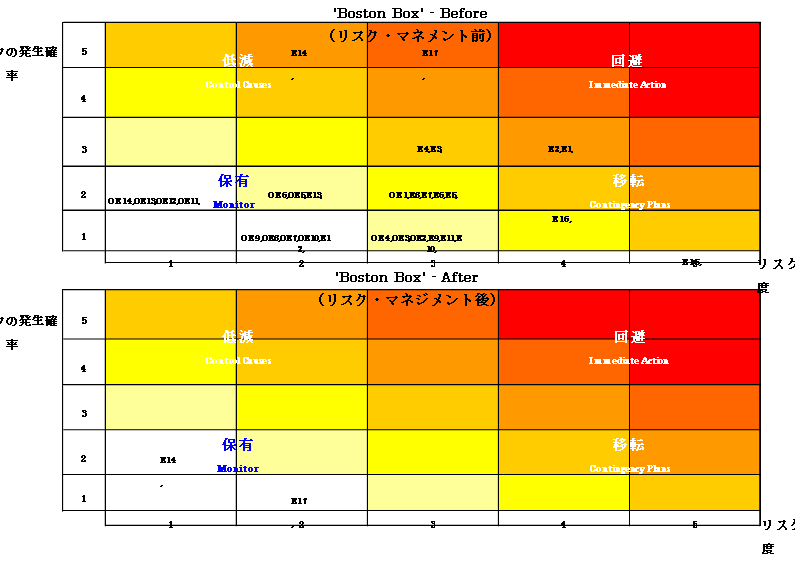

4.リスク対応の選択

マッピングしたリスクは、既に優先順位付けの結果、10~20になっているため、それらを下記の4区分に従い、リスクマネジメント対応策を検討する。

A. 「リスクの強度が強く、発生確率が高い領域に所在するリスク」(上図、「右上の部分」)に対しては、リスクの「回避」をおこなう。「即座の対応」が求められるリスクであり、「強度を弱める」対応策をとるか、「発生確率を低減させる」対応策をとることが肝要だが、そのいずれも不可能な場合は「すぐさま該当業務、事業を廃止、中止すること」も検討する必要がある領域である。

B. 「リスクの強度が強く、発生確率が低い領域に所在するリスク」(上図、「右下の部分」)に対しては、リスクの「移転」をおこなう。この領域にあるリスクに対しては、リスクが顕在化した時にとるべき対応策は、「保険」を含めて「自社が蒙る損害の減少を目的とする各種対応策」を実行することが必要な領域である。「キャプティブにリスク移転することに最も適しているリスク区分」である。

C. 「リスクの強度が弱く、発生確率が高い領域に所在するリスク」(上図、「左上の部分」)に対しては、リスクの「軽減・低減」であり、「リスクの制御」をおこなう領域である。個々の損害は小さいため、発生確率を減じるような対応策を講じることができれば、事業収益の向上に寄与することができる領域でもある。

D. 「リスクの強度が弱く、発生確率も低い領域に所在するリスク」(上図、「左下の部分」)に対しては、特に対策はとらず、自社で「保有」する。リスクの「監視」をおこない、発生した場合のみ対応する領域である。ただし、「保有」の限界をどこに定めるかが重要な点であるので注意が必要。このためには、列挙されたリスクに対してどこまで自社の財務諸表で対応できるか、その分岐点を決める「自己保有分析」が有効となる領域である。

上記を図式化したものが下記である。これもグローバル・リンクでの実際例であり、上図がリスクマネジメントをおこなう前、下図がその後である。リスクマネジメントをおこない、「移転」分野はキャプティブへ移転等、種々の対応策をおこなった結果である。

5.キャプティブを持つ意義と効用

キャプティブを持つ意義と効果には、次の4つがある。

A. 保険コストの低減

B. 保険事業収益・運用益の獲得

C. リスクマネジメントの強化

D. 保険対応が困難なリスクへの対応

これらの目的のために、リスクマネジメントを的確に実行する手法として、「リスク対策に先進的な企業」が採っている手法が、キャプティブの設立である。キャプティブを設立した後は、自らがリスクをとる「再保険者」となるため、自らの努力で損害率を下げれば、保険コストの低減につながり、また企業・団体内にリスク管理の意識を醸成・徹底することができ、企業経営にも非常に好ましい影響を与えることができるからである。

今回のまとめ

キャプティブは、その目的によって、一般的には次の3つに別れる。

A. 企業のリスクマネジメント強化のため

B. 収益を向上させるため

C. 上記A.とB.両方のため

グローバル・リンクでは「C.」を推奨している。その理由としては、リスクネジメントに的確に取り組めば、リスクの低下が起き、保険にも損害率の優良化という現象が起きる。そうなれば、保険を掛けること自身を事業収益に変えていこうとする、リスク・ファイナンス、キャプティブ(自家保険会社)の設立が視野に入ってくるものである。これをグローバル・リンクでは、「Turning Risk to Profit®」(リスクの収益化)と呼び、それを可能にするキャプティブを「ソリューション・キャプティブ®」と呼んでいる。

新型コロナ・ウイルスによる全世界パンデミックの発生、つい半年前までは「不測のリスク」であったこのリスクがいま顕在化している。

日本は「地震リスク」という更に巨大なリスクを抱えている国である。その国に存在する企業としては、この巨大なリスク、首都圏直下地震、南海トラフ大地震への対応を本格化させるべきタイミングが今ではないだろうか。大地震は一瞬で多くの生命、財産を奪っていく可能性が高いからである。

執筆・翻訳者:羽谷 信一郎

English Translation

Captive 12 – Risk Management for Captives

When a company wants to set up a captive, I tell them, “Well, let’s start with risk management. “The purpose of risk management is to categorize all the risks and figure out how to deal with them all, right? ” This type question comes back almost 100%. It is interesting to note that there are indeed many companies that think of risk management in this way.

If you categorize the risks that are latent in a company or environment, there are usually more than 100 risks, both large and small. It would take years to take measures against all of them.

However, there are many risks that occur only once every few decades and are expected to cost hundreds of thousands of yen in damages. The most important thing in risk management is to identify 10 to 20 risks that need to be dealt with as a matter of priority, and in order to do so, the process of quantification (visualization) of the risks is necessary.

The factors for quantification are the probability of occurrence of risks and the intensity of risks, and based on these factors, risks are mapped, risks that have a fairly high probability of being significantly high and risks that have a significant intensity to the company are identified, and countermeasures are considered.

1. The steps of risk management

Companies and organizations are exposed to a variety of risks, as well as risks within their own organizations. Risk management is the process of predicting, verifying, and considering and deciding how to deal with these risks. Risks are often considered to be “dangerous” and many people are interested in their elimination. Because we believe that”Turning Risk to Profit®” is possible, and Global Link’s clients are actually making it a reality through good risk management and the creation of their Solution Captives®. There is a process for risk management from this perspective.

From this perspective, risk management is carried out in the process shown in the figure below for each of the risks for which priority action has been determined. It is important to note that the effectiveness and appropriateness of the risk management measures, once selected and implemented, must be verified on a regular basis in cooperation with experts to ensure that the measures do not evolve with the progress and changes in business and activities and that unexpected situations are not triggered.

2. Types of risks

As mentioned above, there are more than 100 risks that companies and organizations generally involve or encounter.

A. Disaster and accident risks

1. natural disasters

(1) typhoon and storm surge, (2) flood and flood, (3) tornado, windstorm and lightning, (4) earthquake, tsunami and eruption, (5) bad weather and

abnormal weather

2. Accidents

(1) fires and explosions, (2) power outages and infrastructure paralysis, (3) traffic accidents, (4) aircraft accidents, train accidents and ship accidents

Accident, (5) Accident due to inadequate equipment, (6) Industrial accident, (7) Accident during construction, (8) Accident and piracy in transit, and

(9) Theft/illegal invasion, (10) Radiation contamination/leakage, (11) Harmful microorganisms, (12) Bacterial leakage, (13) Biohazard, (14) Network system failure, (15) Computer virus/cybertechnology, (16)The disappearance of computer data

B. Management Risks

1. Management

(1) hostile M&A, (2) failure of acquisitions, mergers and acquisitions, (3) failure of new businesses and capital investment, (4) failure of mergers and acquisitions

(5) death of a manager, (5) inability of management to perform their duties, (6) disorganized management, (7) scandals at group companies, and (8) customer complaints, and (9) suspension of financial support

2. Intellectual Property Rights

(1) copyright infringement, (2) patent disputes, and (3) trademark infringement.

3. Environment

(1) stricter environmental regulations, (2) environmental liability and violations of environmental regulations, (3) environmental pollution and oil pollution accidents, (4) waste disposal management and Recycling.

4. Products and Production

(1) defects, (2) product liability, (3) recalls and defective products, (4) stoppage of overseas production bases, and (5) Inferiority of own products due to production technology innovation.

5. labor relations

(1) Discrimination (nationality, religion, age, sex), (2) Employer responsibility, (3) Labor disputes, strikes and demonstrations, (4)A pandemic caused by AIDS, contagious diseases, new strains of influenza, etc., (5) Group turnover,(6) suicide of employees due to overwork or overwork, (7) illegal foreign employment, (8) employment adjustment of employees, (9) aging of employees, (10) safety of expatriate employees, (11) industrial espionage.

6. Compliance

(1) violations of the Antimonopoly Law, cartels and collusion, (2) violations of the Financial Instruments and Exchange Law,(3) violations of the Companies Act, and (4) massive omissions of tax returns. (5) invasion of privacy, (6) inadequate information management and leakage of customer information, (7) directors’ and officers’ liability, (8) officer scandals, (9) sexual and power harassment, (10) Unfair trade, fraud, embezzlement, bribery, and bribery, (11) Violation of various laws and ordinances.

7. Finance

(1) derivative failures, (2) counterparty bankruptcy, (3) downgrade of credit ratings, and (4) non-performing loans and loan losses.

8. Marketing

(1) failure of developed products, (2) globalization of competition and customers, (3) changes in market needs, and (4) Failed pricing strategy.

C. political, economic and social risks

1. politics

(1) legislation, institutional and tax reform, (2) pressure from the international community, (3) trade restrictions and trade issues, (4) war,conflict and civil war.

2. Economy

(1) economic crisis and fluctuations in the economy, (2) fluctuations in stock prices, foreign exchange rates, interest rates and land prices, (3) raw materials, materials and high oil prices, (4) Falling credit ratings.

3. Society

(1) terrorism and riots, (2) kidnapping and hostage taking, (3) threats by anti-social forces, (4) Criticism and defamation using the Internet,(5) criticism and slander by the media, (6) failure to respond to the media, (7) propaganda and advertising failures, (8) rumors, (9) boycotts, consumer movements, and deteriorating relations with local communities, (10) population decline, low birthrate and labor shortage.

3. Risk mapping

As mentioned earlier, among these risks, 10 to 20 risks, as shown in the figure above, can be mapped and “visualized” to make decisions that are closer to the reality of the risks.

For some companies, the number of major risks has been reduced because they already have risk management in place.

The figure below above an actual risk map conducted by Global Link in the past. Three years after the captive was established, the number of risks has increased from more than 20 to nine as a result of the annual company-wide risk management campaign led by the Risk Management Committee.

4. Selection of risk response

Since the mapped risks have already been prioritized as 10 to 20, they will be considered for risk management measures according to the following four categories.

A. “Avoidance of risks that are high risk intensity and high probability of occurrence (the upper right-hand corner of the diagram above). This is a risk that requires an immediate response, and it is important to take measures to either reduce the intensity or to reduce the probability of occurrence.

B. For “risks that are located in areas with high risk intensity and low probability of occurrence” (the lower right-hand corner of the diagram above), transfer the risks. For risks in this area, it is necessary to take various measures, including insurance, to reduce the amount of damage the company suffers when the risk becomes apparent. This is the most appropriate risk category for risk transfer to captives.

C. “Risks that are located in areas of weak risk intensity and high probability of occurrence” (the upper left-hand corner of the diagram above) are mitigated or reduced, and risk control is carried out in this area. Since each loss is small, this area can contribute to the improvement of business profits if countermeasures are taken to reduce the probability of occurrence.

D. “Risks with weak risk intensity and low probability of occurrence” (the lower left-hand side of the figure above) should be “retained” by the company without taking any special measures. This is an area where risks are monitored and responded to only when they occur. However, it is important to note that it is important to determine the limits of “retention”. For this purpose, this is an area where “proprietary analysis” is effective, which determines a turning point in determining the extent to which the enumerated risks can be handled by the company’s financial statements.

A graphical representation of the above is shown above. The above diagram is also an actual example of a global link, with the upper diagram being before risk management and the lower diagram being after. This is the result of risk management and various measures, such as transferring the “transfer” field to a captive.

5. Significance and benefits of having captives

The significance and benefits of having a captive are fourfold.

A. Lower insurance costs.

B. Earning Insurance Business Income and Investment Income

C. Strengthen Risk Management

D. Addressing Risks that are Difficult for Insurance to Address

To achieve these goals, the establishment of a captive is a method adopted by companies that are “advanced in risk management” as a method of accurately implementing risk management. Once a captive is established, it becomes a “reinsurer” that takes risks on its own, so lowering the loss ratio through its own efforts can lead to lower insurance costs and foster and instill an awareness of risk management within a company or organization, which can have a very positive impact on corporate management.

Summary of this issue

Captives are generally divided into three categories, depending on their purpose

A. To enhance enterprise risk management

B. to increase revenue

C. for both A. and B. above

Global Link recommends “C”. The reason for this is that if risk management is properly addressed, risk will be reduced and insurance companies will experience a superior loss ratio. If this happens, the establishment of a risk financing or captive (self-insurance company) will become an option to turn insurance into a business profit. This is what Global Link calls “Turning Risk to Profit®”, and we call the captives that make this possible “Solution Captives®”.

A global pandemic caused by a new type of coronavirus was an “unforeseen risk” just six months ago, but this risk is now becoming more apparent.

Japan has an even greater earthquake risk. Now is the right time for companies in this country to get serious about dealing with this huge risk, an earthquake with an epicenter directly below the Tokyo metropolitan area and a major earthquake in the Nankai Trough. This is because a major earthquake is likely to take away many lives and property in an instant.

Author/translator: Shinichiro Hatani