キャプティブ 2025.09.16

CA77 ロイズ(Lloyd’s of London)連載第4回 ー キャプティブからリスクが行き着く先ー

目次

Copyright © Shinichiro Hatani 2025 All rights reserved

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

10.ロイズ(Lloyd’s of London)の仕組みと構造

仕組み

「ロイズ(Lloyd’s of London)」は、よく「英国の保険会社ロイズ」と紹介されるが、本小論考で繰り返し述べてきたとおり、「ロイズ(Lloyd’s of London)は保険会社ではなく保険市場」である。

2018年築地から豊洲に移転した「豊洲市場」を思い浮かべると「ロイズの仕組み」が理解できるのではないだろうか。

世界から集まる水産物や青果物を流通させる重要な拠点である「豊洲市場」は、マグロの競り(せり)など、国内外から集まる水産物や青果物の取引が行われる「卸売場」、卸売業者から仕入れた水産物や青果物を、飲食店や小売店に販売する仲卸業者の店舗が集まる「仲卸売場」 から成り立っている。

一方、「保険市場」であるロイズ(Lloyd’s of London)は、「リスクの売買」をおこなう場として、「リスクを売りたい(=買って欲しい)人々」が、「ロイズ・ブローカー」を仲介者として、「シンジケートのアンダーライター」と「個別の競り(せり)をおこない、売買をおこなう場」と言えるだろう。

「豊洲市場の『卸売場』と『仲卸売場』を一か所」にして、取引所である「アンダーライティング・ルームに集めた仕組み」、それがロイズ(Lloyd’s of London)である。

「ロイズ保険組合」とよく日本語訳されている「ロイズ(Lloyd’s of London)」。Lloyd‘sの公式WEBサイトで、「市場の評判を保護および維持するために行動し、業界の知識ベースにサービスと独自の調査、レポート、分析を提供する独立した組織および規制当局である」とされている、「ロイズ(Lloyd’s of London)」全体の運営管理をおこなう組織がある。

それが、ロイズ(Lloyd’s of London)の公式WEBサイトで、大きく「Lloyd’s Corporation」(ロイズ・コーポレーション)と紹介されている組織である。しかし、そのページの下には「Lloyd’s Copyright 2025 Lloyd’s and Corporation of Lloyd’s are registered trademarks of the Society of Lloyd’s. 」( ロイズの著作権 2025 ロイズおよび「Corporation of Lloyd’s」は、「Society of Lloyd’s」の登録商標です)とある。

(出典:「ロイズ(Lloyd’s of London)公式WEBサイト」)

ロイズ法での正式名称は「Corporation of Lloyd’s」(コーポレーション・オブ・ロイズ)であるが、なぜか「これら2つの名称が同時に「ロイズ(Lloyd’s of London)」によって使用されている」のである。

このことについて、筆者は「Lloyd’s Corporationは通称だろう」と考えたが、2つの名称が混在していることが理解できなかったので、ロイズ・ブローカーとして数十年の経験を有するプロ中のプロの旧友に、「For some reason, Lloyd’s official website introduces it as “Lloyd’s Corporation”, yet its official name under the Lloyd’s Act is “Corporation of Lloyd’s”. Why is that? (なぜかロイズの公式ウェブサイトでは「ロイズ・コーポレーション」と紹介されているが、ロイズ法に基づく正式名称は「コーポレーション・オブ・ロイズ」である。なぜだろうか?)」と聞いたところ、返ってきた答えが以下であった。

「No, do not really know why the two forms of reference are used !!(いや、なぜ2つの参照形式が使われているのか、全くわからない!!)」、と。彼でさえ理解できないとのこと。まことに不可思議な現象である。

いずれにしても、ロイズ(Lloyd’s of London)は、機能的には保険の引受をおこなう「シンジケートの集合組織体」とその組織を管理、統治する組織である「Corporation of Lloyd’s」(コーポレーション・オブ・ロイズ)(Lloyd’s Corporationとも通称される)に、コーポレート・ガバナンスの点で分化しているということである。

構造

この「Corporation of Lloyd’s」(コーポレーション・オブ・ロイズ)は、ロイズという巨大な「保険市場」の規則を定め、規制、管理、運営する法人であるが、個々の保険契約を引き受けるのは、あくまでも「シンジケート」である。そして、これら全体を指して「ロイズ(Lloyd’s of London)」と呼んでいる。

英国の議会法である、前述のロイズ法(Lloyd’s Act 1982)が、ロイズ(Lloyd’s of London)における管理構造と規則を定めている。

この法律では、ロイズ(Lloyd’s of London)の正式名称は、「Society of Lloyd’s(ソサイエティ・オブ・ロイズ)」と定められているが、知り合いのアンダーライター、ブローカーの誰もがそうは呼ばず、「Lloyd’s of London」と呼んでいる、これまた不思議な事象である。

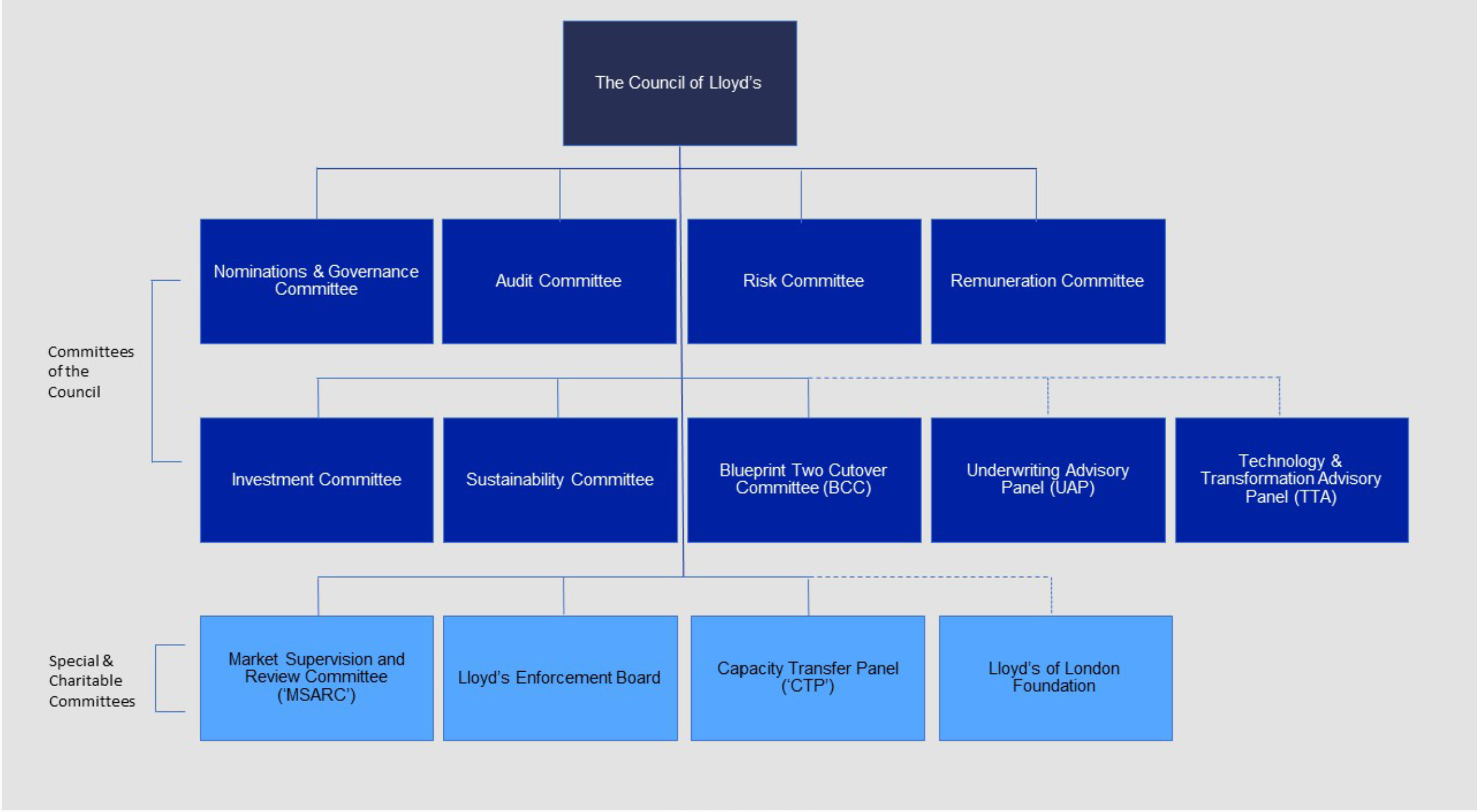

ロイズ法(Lloyd’s Act 1982)には、ロイズ評議会(Council of Lloyd’s)が、「ロイズ(Lloyd’s of London)全体の管理と監督に関する責任を負っている」と定められている。

評議会には、通常、3人の実務委員、3人の外部委員、9人の指名委員がいる。実務委員と外部委員は、ロイズ(Lloyd’s of London)のメンバーから選出され。議長と副議長は、評議会によって、毎年、そのメンバーの中から選出される。

このロイズ評議会(Council of Lloyd’s)は、ロイズ(Lloyd’s of London)全体の規則、細則を決定するが、ロイズ・マーケットの運営に関連する日常的なガバナンスは、以前、そのほとんどはフランチャイズ委員会(Franchise Board)に委任していた、そういう趣旨のロイズ(Lloyd’s of London)に関する資料、レポート等もあるが、2019年この委任を廃止、ロイズ評議会(Council of Lloyd’s)にコーポレート・ガバナンスを一本化、組織も下記のとおり変更した。

(出典:「ロイズ(Lloyd’s of London)公式WEBサイト」)

このように、ロイズ評議会(Council of Lloyd’s)は、上記の組織を通じてロイズ(Lloyd’s of London)市場に存在する、すべてのシンジケートへの「ガイドライン」を定め、引受とリスク管理を適正におこなうための事業計画とその進捗を随時ウオッチしているが、個々の保険商品の開発、保険引受に関与することはない。それは「シンジケートがおこなう分野」だからである。

11.ロイズ・マーケットでの取引

① ロイズ・ビルへの入館

経営コンサルタントの時は、保険商品の開発、キャプティブ事業を開始してからは、キャプティブからの再保険の手配のため、提携している保険ブローカー、再保険会社との打ち合わせのために足繁く通ってきたロンドン。ロイズ・ビルの紹介で、「『バンク(Bank)駅』から、歩いて4,5分の場所に『ロイズ』(Lloyd‘s of London)の建物がある。」と紹介した。

これは、先に述べたとおり、筆者が長年、毎年6回、ロンドンに通っていた際に定宿にしていたホテルが、その駅に止まる地下鉄「セントラル・ライン」のランカスター・ゲート駅の真上にあり、この「セントラル・ライン」を使って、シティ、「ロイズ」(Lloyd‘s of London)に通っていたからである。この地下鉄がロンドン市街を初めて走ったのは、1863年であった。

この200年前、1666年、大火がこのロンドンを襲った。現在では、米国のウオール・ストリートとならび「国際金融街」として有名な「シティ」と言われる一角に通じる地下鉄の駅、その1つに「ディストリクト・ライン」や「サークル・ライン」の駅、モニュメント駅がある。

モニュメント駅に降り立つと、その駅前には、まさにその名のとおり、モニュメント(記念碑)が建っている。「街を焼き尽くす勢いであった」とその壁面のレリーフに彫り込まれている大火を記念した「ロンドン大火記念塔」(The Monument to the Great Fire of London)である。高さは、その場所から火元とされた「パン屋」までの距離と同じ62m。ここから、歩いて数分のところにロイズ(Lloyd ‘s of London)がある。

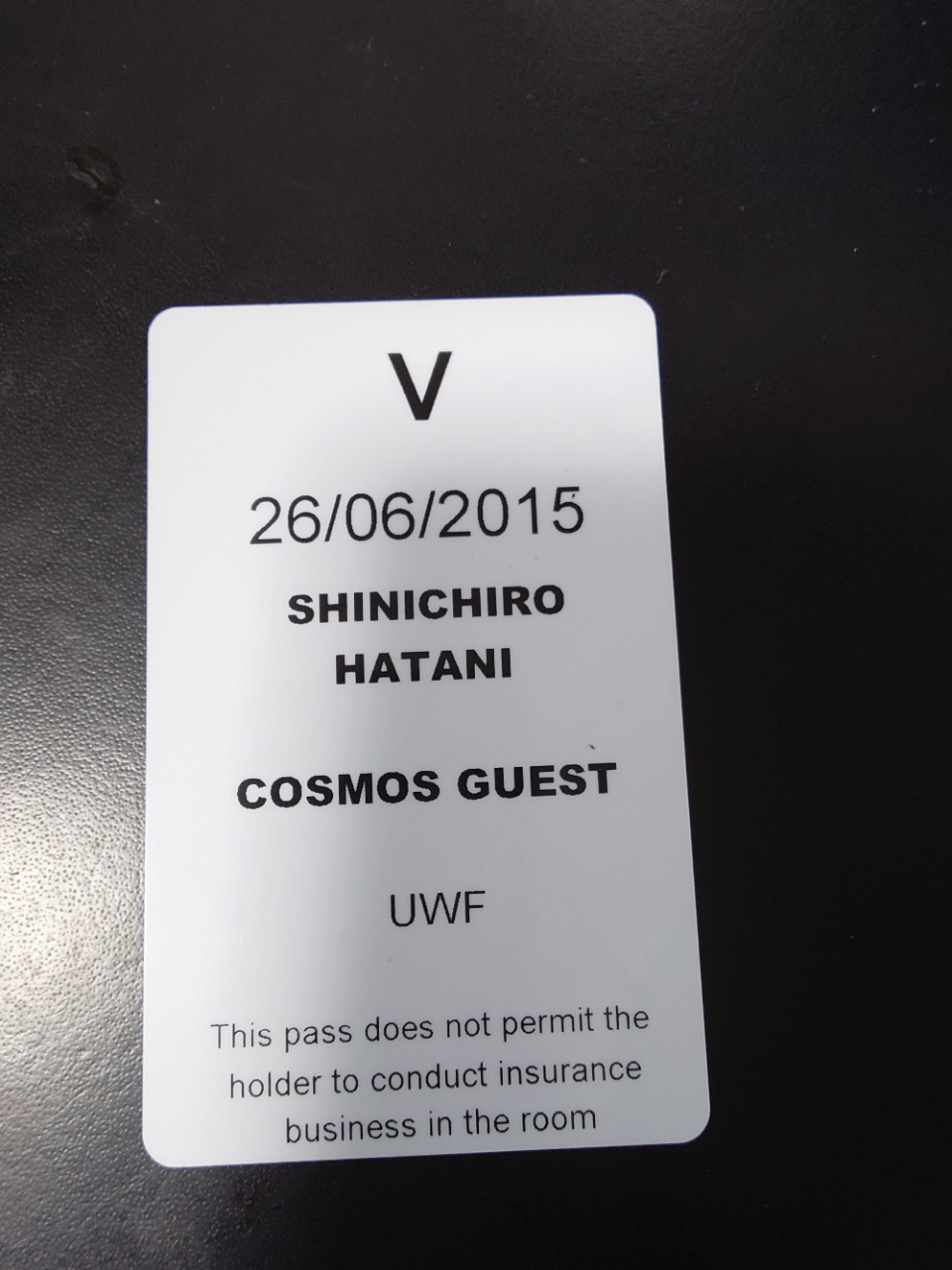

ロイズ(Lloyd‘s of London)に入るためには、連れてきてくれた紹介者は、「ロイズ・ビルへの入館証」を示す。その傍らで、同行者は「名刺」と「フォトID」(写真付きのIDカード)を示し、「日付限定の入館証」を受け取る。5年前、コロナ禍の直前にロンドンに行った際には、「紙」になっていたが、その前は、下の写真のようなプラスチック・カードであった。

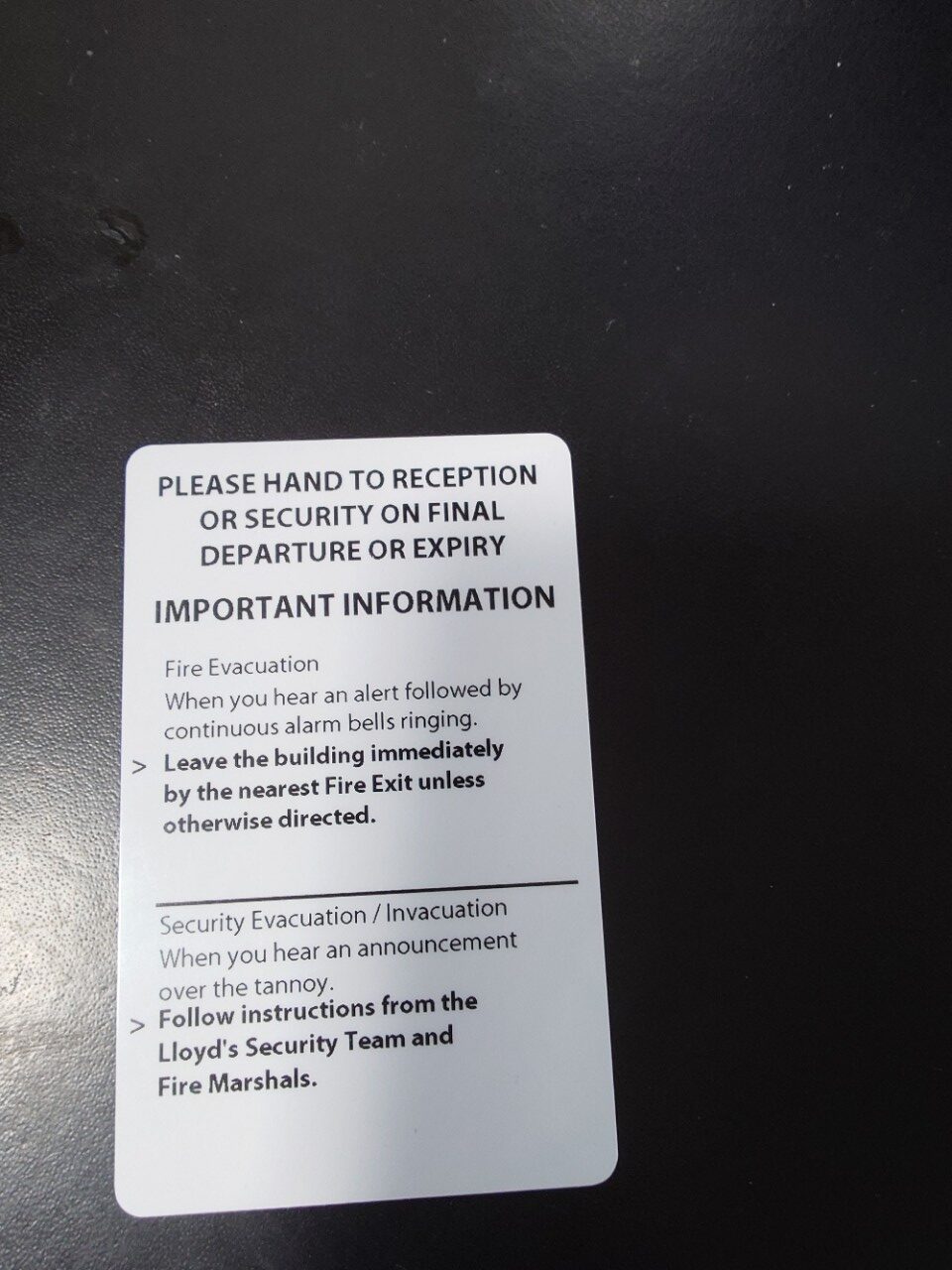

この「入館証」はその裏面に「Please hand to reception or security on final departure or expiry」(最終退出時または有効期限切れの際は、受付または警備員へご返却ください)と書いてある。

いつもは「Thank you」と言いながら受付に返していた。しかし、その日は、午前中にロイズ・ビルに入り商談、それからアンダーライターとランチに出かけた。それが「長いランチ」となり「ディナーまでとなった日」であった。このため返却できず今も手元にある。

日付が2015年6月26日、その下に筆者の名前が記されている。さらに、その下には、「COSMOS GUEST」とある。当時業務提携をしていた伊藤忠商事100%子会社の保険・再保険ブローカー、「Cosmos Rusk Solutionsの紹介でロイズ・ビルに入ったこと」が記されているのである。

「UWF」(Underwriting Floor)と記されている。「ロイズ・ビルの一般見学者」は入室が許可されない、つまり「実際の保険取引が行われるアンダーライティング・ボックスがあるアンダーライティング・フロアへの入室が許可されている」という意味である。

しかし、その下に更に「This pass does not permit the holder to conduct insurance business in the room」(この許可証は、所持者が当該室内で保険業務を行うことを許可するものではありません)とある。つまり、筆者はロイズ・ブローカーではないため、「アンダーライティング・ルーム(フロア)で、保険取引をすることを許可するものではない」と記され、「ロイズ(Lloyd’s of London)の中で保険取引ができるのは、ロイズ・ブローカーのみであること」を明確に示しているのである。

② ロイズ・ブローカー(The Lloyd’s broker)

このように、ロイズ・ビルのなかで、保険取引ができる権限を有しているのは、保険を引受けるシンジケートに所属するアンダーライターと、約400社が認定されているロイズ・ブローカー(The Lloyd’s broker)である。

したがって、ロイズ・ビルのなかで保険の商談をしようとする場合には、ロイズ・ブローカーと一緒に入館することが必須である。更に、上記Passの但し書き「アンダーライティング・ルーム(フロア)で、保険取引をすることを許可するものではない」とあるとおり、顧客が「ロイズ(Lloyd’s of London)」の中でロイズ・ブローカーも帯同せずアンダーライターと保険取引、開発等の話をすることはできないのである。

但し、2008年、前述のロイズ法が改正され、ロイズ・ブローカー以外でも、一定の要件を満たしたブローカーは取引できるようになったが、実態としては、従来とあまり変化せず、「ロイズ(Lloyd’s of London)での取引はロイズ・ブローカー」というのが業界の常識である。

しかし、これはあくまでも「ロイズ・ビルのアンダーライティング・ルームの中でのこと」であり、シンジケートがロイズ・ビルの外に有している事務所で保険取引の話をすること、それはまた、「話は別」である。

ロイズ(Lloyd’s of London)のシンジケートを所有・管理している、保険会社系を中心にしたマネージング・エージェントそしてシンジケートは、ロイズ・ビルの中に「アンダーライティング・ボックス」を有する以外、「保険会社の現地法人を有していること」も多く、「事務所で話をしよう」と言われることが多いはずである。

背景には、保険料収入のうち数%をロイズ・シンジケート全体の「安定化資金」として「セントラルファンド」に拠出することを避ける意味合いもあるが、更に重要なことは、アンダーライティング・ルーム内では、常にボックスの周りに立って待っている何人もの順番を待つブローカーの存在があり、「秘匿性の高い案件、大きなプロジェクトの会話をしていること」を周囲に悟らせないためである。

筆者が長年経営コンサルティングを委嘱されていた損害保険会社は、ロイズ(Lloyd’s of London)のあるシンジケートと一緒に保険商品を開発してそのシンジケートに再保険を出していた。

「損害率が抜群に良い=大いに儲かる」ためであろう、マネージング・エージェントから自社の親会社である再保険会社が設立した保険会社へ「再保険先を変更すること」を依頼されたことがある。その保険会社は、再保険のセキュリティ上も全く問題がなかったため、異論はなく再保険先を変更したことを記憶している。

1960年代、70年代は、再保険の「ロンドン・マーケット」と言えば「ロイズ(Lloyd’s of London)」を指すことが一般的であったが、以上のような理由から、また世界的規模の再保険会社がロンドンに大きな拠点を構えるようになってからは、「ロイズ(Lloyd’s of London)を含めたロンドン、シティに存在する保険会社、再保険会社の拠点」のことを指す意味合いが強くなっている。

執筆・翻訳者:羽谷 信一郎

English Translation

Copyright © Shinichiro Hatani 2025 All rights reserved

Unauthorised reproduction, quotation or duplication of the contents within this column is strictly prohibited.

Captive (CA) 77 – Lloyd’s of London – Part 4 — Where Risk Lands from Captives —

10.The Mechanism and Structure of Lloyd’s of London

Mechanism

Lloyd’s of London is often introduced as ‘the British insurance company Lloyd’s’, but as repeatedly stated in this brief essay, ‘Lloyd’s of London is not an insurance company but an insurance market’.

One might grasp the mechanism of Lloyd’s of London by considering the Toyosu Market, which relocated from Tsukiji in 2018.

The Toyosu Market, a vital hub distributing seafood and produce from around the world, comprises the “Wholesale Market” where transactions for seafood and produce from domestic and international sources, such as tuna auctions, take place, and the “Middle Wholesale Market” where shops of middle wholesalers, who purchase seafood and produce from wholesalers and sell them to restaurants and retailers, are concentrated.

Conversely, Lloyd’s of London, as an insurance market, can be described as a venue for the “buying and selling of risk”. It is a place where “those wishing to sell their risk (i.e., seeking buyers)” conduct “individual auctions” with underwriters, facilitated by Lloyd’s brokers, to buy and sell coverage.

The mechanism of consolidating Toyosu Market’s “wholesale market” and “intermediate wholesale market” into a single location, the exchange known as the “underwriting room”, is precisely what constitutes Lloyd’s of London.

Lloyd’s of London, often translated into Japanese as “ロイズ保険組合(Lloyd’s Insurance Association)”.

On Lloyd’s official website, it is stated that there exists an organisation responsible for the overall operational management of Lloyd’s of London, described as ‘an independent organisation and regulatory authority that acts to protect and maintain the market’s reputation, providing services and unique research, reports, and analysis to the industry’s knowledge base.’

This is the organisation prominently introduced on Lloyd’s official website as ‘Lloyd’s Corporation’.However, at the bottom of that page, it states: ‘Lloyd’s of London Copyright 2025 Lloyd’s and Corporation of Lloyd’s are registered trademarks of the Society of Lloyd’s.’

(Source: Lloyd’s of London official website)

The official name under the Lloyd’s Act is ‘Corporation of Lloyd’s’, yet for some reason ‘both names are simultaneously used by Lloyd’s of London’.

Regarding this, the author considered that ‘Lloyd’s Corporation must be the common name’, but as I could not grasp the true intent, I asked an old friend, a seasoned Lloyd’s broker with decades of experience: ‘For some reason, Lloyd’s official website introduces it as “Lloyd’s Corporation”, yet its official name under the Lloyd’s Act is ‘Corporation of Lloyd’s’. ‘Why is that?’ The response was as follows:

‘No, do not really know why the two forms of reference are used !!’Even he couldn’t understand it. Truly a baffling phenomenon.

In any case, Lloyd’s of London is functionally differentiated in terms of corporate governance into the ‘syndicate collective body’ that underwrites insurance and the organisation that manages and governs that body, the Corporation of Lloyd’s (also commonly referred to as Lloyd’s Corporation).

Structure

This “Corporation of Lloyd’s” is the legal entity that sets the rules, regulates, manages, and operates the vast “insurance market” known as Lloyd’s of London. However, it is the individual “syndicates” that underwrite the actual insurance policies. Collectively, this entire structure is referred to as “Lloyd’s of London”.

The aforementioned Lloyd’s Act 1982, an Act of the British Parliament, establishes the governance structure and rules within Lloyd’s of London.

Under this legislation, the formal name of Lloyd’s of London is defined as the “Society of Lloyd’s”. Yet, curiously, neither underwriters nor brokers one knows refer to it as such; they invariably call it “Lloyd’s of London”.

The Lloyd’s Act 1982 stipulates that the Council of Lloyd’s ‘has responsibility for the management and supervision of Lloyd’s of London as a whole’.

The Council typically comprises three Executive Members, three External Members, and nine Nominated Members. The Executive and External Members are elected from among the Members of Lloyd’s of London. The Chairman and Deputy Chairman are elected annually by the Council from among its members.

The Council of Lloyd’s determines the rules and regulations governing Lloyd’s of London as a whole, but the day-to-day governance relating to the operation of the Lloyd’s market was previously delegated, for the most part, to the Franchise Board. While materials and reports concerning Lloyd’s of London exist reflecting this approach, in 2019 this delegation was abolished. Corporate governance was consolidated within the Council of Lloyd’s, and the organisational structure was changed as follows.

(Source: Lloyd’s of London official website)

Thus, the Council of Lloyd’s, through the aforementioned organisation, sets guidelines for all syndicates operating within the Lloyd’s of London market and continuously monitors business plans and their progress to ensure appropriate underwriting and risk management. However, it does not engage in the development of individual insurance products or in underwriting activities. This is because these are areas for the syndicates to handle.

11.Trading on the Lloyd’s of London Market

① Accessing the Lloyd’s Building

During my time as a management consultant, I frequently travelled to London for meetings with partner insurance brokers and reinsurance companies—first to develop insurance products, and later, after launching the captive business, to arrange reinsurance from the captive. In the section introducing the Lloyd’s building, I described its location: ‘Lloyd’s of London is situated about four- or five-minutes’ walk from Bank station.’

As mentioned earlier, this is because the hotel where the author stayed regularly during his many years of travelling to London six times a year was located directly above Lancaster Gate station on the Central Line, which stops at that station. He used the Central Line underground to travel to the City and Lloyd’s of London. This underground line first ran through central London in 1863.

As mentioned above, around that time, the London Underground opened. This single event alone demonstrates how detrimental the Tokugawa shogunate’s three-hundred-year “sakoku”(national isolation) policy proved for Japan. It was likely a major factor in the flood of “samurai” who then poured out into the world.

Two hundred years before the closing days of the Tokugawa shogunate, in 1666, a great fire ravaged this city of London. Today, one of the underground stations serving the area known as the City – now famous as an “international financial district” alongside Wall Street in the United States – is Monument Station, served by the District Line and Circle Line.

Stepping out at Monument Station, one finds, true to its name, a monument standing before the station. It is the Monument to the Great Fire of London, commemorating the conflagration whose ‘fury was such it consumed the city’, as carved into its relief walls. Its height, 62 metres, matches the distance from this spot to the bakery identified as the fire’s origin. A few minutes’ walk from here lies Lloyd’s of London.

The introducer who brought us to Lloyd’s of London presented the “Lloyd’s Building Access Pass”. Beside them, the accompanying person showed their “business card” and “photo ID” (an ID card with a photograph) and received a “date-specific access pass”. Five years ago, just before the covid-19 pandemic, when I visited London, it was a “paper” pass. Before that, it was a plastic card, as shown in the photograph below.

This “access pass” has the following written on its reverse: “Please hand to reception or security on final departure or expiry”.

I usually returned it to reception with a “Thank you”. However, that day, I entered the Lloyd’s of London Building for business discussions in the morning, then went out for lunch with an underwriter. That lunch turned into a “long lunch” and a day that stretched into dinner. Consequently, I was unable to return it and still have it in my possession.

The date is 26 June 2015, with the author’s name written below. Further down, it states ‘COSMOS GUEST’. This indicates entry to the Lloyd’s of London Building was facilitated by Cosmos Rusk Solutions, an insurance and reinsurance broker and wholly owned subsidiary of Itochu Corporation, with whom we had a business partnership at the time.

It is marked ‘UWF’ (Underwriting Floor). ‘General visitors to the Lloyd’s of London Building’ are not permitted entry; this pass signifies ‘permission to enter the Underwriting Floor, where the actual underwriting boxes conducting insurance transactions are located’.

However, further down it states: ‘This pass does not permit the holder to conduct insurance business in the room’. Thus, as the author is not a Lloyd’s broker, it is explicitly stated that ‘this pass does not permit the holder to conduct insurance business in the underwriting room (floor)’, clearly indicating that ‘only Lloyd’s brokers may conduct insurance business within Lloyd’s of London’.

② The Lloyd’s broker

Thus, within the Lloyd’s of London building, only underwriters belonging to insurance syndicates and approximately 400 authorised Lloyd’s of London brokers possess the authority to conduct insurance transactions.

Therefore, to conduct insurance business negotiations within the Lloyd’s of London building, entry must be accompanied by a Lloyd’s of London broker. Furthermore, as stated in the proviso on the aforementioned Pass: ‘This does not permit insurance transactions to be conducted in the Underwriting Room (Floor)’, a client cannot discuss insurance transactions, development, or similar matters with an underwriter within Lloyd’s of London without being accompanied by a Lloyd’s broker.

In 2008, the aforementioned Lloyd’s Act was amended, allowing transactions to be conducted not only by Lloyd’s brokers but also by other brokers meeting certain requirements. In practice, however, little has changed from the previous situation, and it remains the industry convention that ‘transactions at Lloyd’s of London are conducted by Lloyd’s brokers.

However, this restriction applies solely to ‘conducting insurance transactions within the Underwriting Rooms of the Lloyd’s of London Building’. Conversations regarding insurance transactions held at an office maintained by a syndicate outside the Lloyd’s of London Building are a separate matter.

Managing agents and syndicates, which are insurance company-affiliated entities owning and managing Lloyd’s of London syndicates, often possess ‘underwriting boxes’ within the Lloyd’s Building. Furthermore, many also have local subsidiaries of insurance companies, meaning they frequently invite clients to ‘discuss matters at their offices’.

This practice stems partly from a desire to avoid contributing a percentage of premium income to the Central Fund as stabilisation capital for the entire Lloyd’s of London syndicate. More significantly, however, it is to prevent others from discerning that highly confidential deals or major project discussions are taking place, given the constant presence of brokers queuing around the underwriting boxes.

The non-life insurance company for which the author was commissioned as a management consultant for many years developed insurance products in collaboration with a Lloyd’s of London syndicate and provided reinsurance to that syndicate.

I recall an instance where the managing agent requested a change in reinsurance provider, directing the reinsurance to an insurance company established by its parent reinsurance firm. This was likely because the loss ratio was exceptionally favourable, meaning substantial profits. As the insurance company in question posed no security concerns whatsoever regarding reinsurance, the change was made without objection.

During the 1960s and 1970s, the term ‘London Market’ for reinsurance generally referred to Lloyd’s of London. However, for the reasons outlined above, and particularly since global reinsurance companies established significant bases in London, the term has increasingly come to denote the hub of insurance and reinsurance companies operating in the City of London, including Lloyd’s of London.

Author/translator: Shinichiro Hatani