キャプティブ 2025.09.23

CA78 ロイズ(Lloyd’s of London)連載第5回(最終回) ー キャプティブからリスクが行き着く先ー

Copyright © Shinichiro Hatani 2025 All rights reserved

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

③ ロンドン・マーケットから学ぶこと

ロイズ(Lloyd’s of London)そしてロンドン・マーケットの特徴は、「リスクをシェアすること」である。最近、日本では損害保険会社が大企業の保険取引で他の損害保険会社と「分担」(シェア)して引受けることが、なぜか問題視されたが、筆者の目にはまことに奇異に映る。

理由は、「損害保険で補償されるリスクは生命保険のそれと違い不確実性が高く、したがって不測の事態が起きる可能性が高いため、リスク・ヘッジ手段はできるだけ多く、手厚いことが重要だから」である。

そのために編み出された「リスク分散の手法」が再保険である。当然、一つの損害保険会社の再保険ネットワークでリスク分散するよりも、多くの損害保険会社の再保険ネットワークでリスク分散するほうが、「リスク分散網が大きくなり、補償の安定性が高まり、惹いては損害保険会社の安定性、また保険金支払いの確実性も高く」なる。こういった点からも推し進めるべきリスク分散の手法が「リスクをシェアすること」である。

ロイズ(Lloyd’s of London)が、なぜ、数々の困難な事態を潜り抜けることができて300年を超えて存在してきたか、それはひとえにこの「リスク分散」を徹底してきたからに他ならないと言えるだろう。

④ Line slip(ライン・スリップ)

ロイズ(Lloyd’s of London)、ロンドン・マーケットでおこなわれている、この「リスク分散の手法」、「リスクをシェアする方法」こそ、Line slip(ライン・スリップ)である。

「ロイズ(Lloyd’s of London)の公式WEBサイト」には、Line slip(ライン・スリップ)について、以下のように記されているので引用する。

A line slip is an agreement by which a Managing Agent delegates its authority to enter into contracts of insurance to be underwritten by the members of a syndicate managed by it to another Managing Agent or authorised insurance company in respect of business introduced by a Lloyd’s Broker named in the agreement.

Managing Agents do not need approval from Lloyd’s to operate under a line slip.

Once the Managing Agent or insurance company acting as the line slip lead underwriter has entered into a contract of insurance with the insured, the evidence of insurance will normally be issued by means of a MRC contract or via a certificate / policy. The format of the insurer authorised documentation will be determined within the line slip agreement.

(筆者訳)

ライン・スリップとは、マネージング・エージェントが、その傘下にあるシンジケートに属するメンバー(アンダーライター)が引受ける保険契約を締結する権限、それを当該契約書に指定されたロイズ・ブローカーが紹介する業務に関して、他のマネージング・エージェント、または承認を受けた保険会社に委任する合意文章のこと。

マネージング・エージェントは、ライン・スリップのもとでおこなわれる業務を執行する際にはロイズの承認を必要としません。

マネージング・エージェントまたはライン・スリップのリード・アンダーライターとして機能する保険会社が、被保険者と保険契約を締結した場合、保険の証明は通常、MRC契約書または証明書/保険証券を通じて発行されます。保険会社による承認書類の形式は、ライン・スリップ契約書内で決定されます。

まさに、「他のシンジケートや損害保険会社と『分担』(シェア)して引受ける」ことを示す書類が「Line slip(ライン・スリップ)」である。

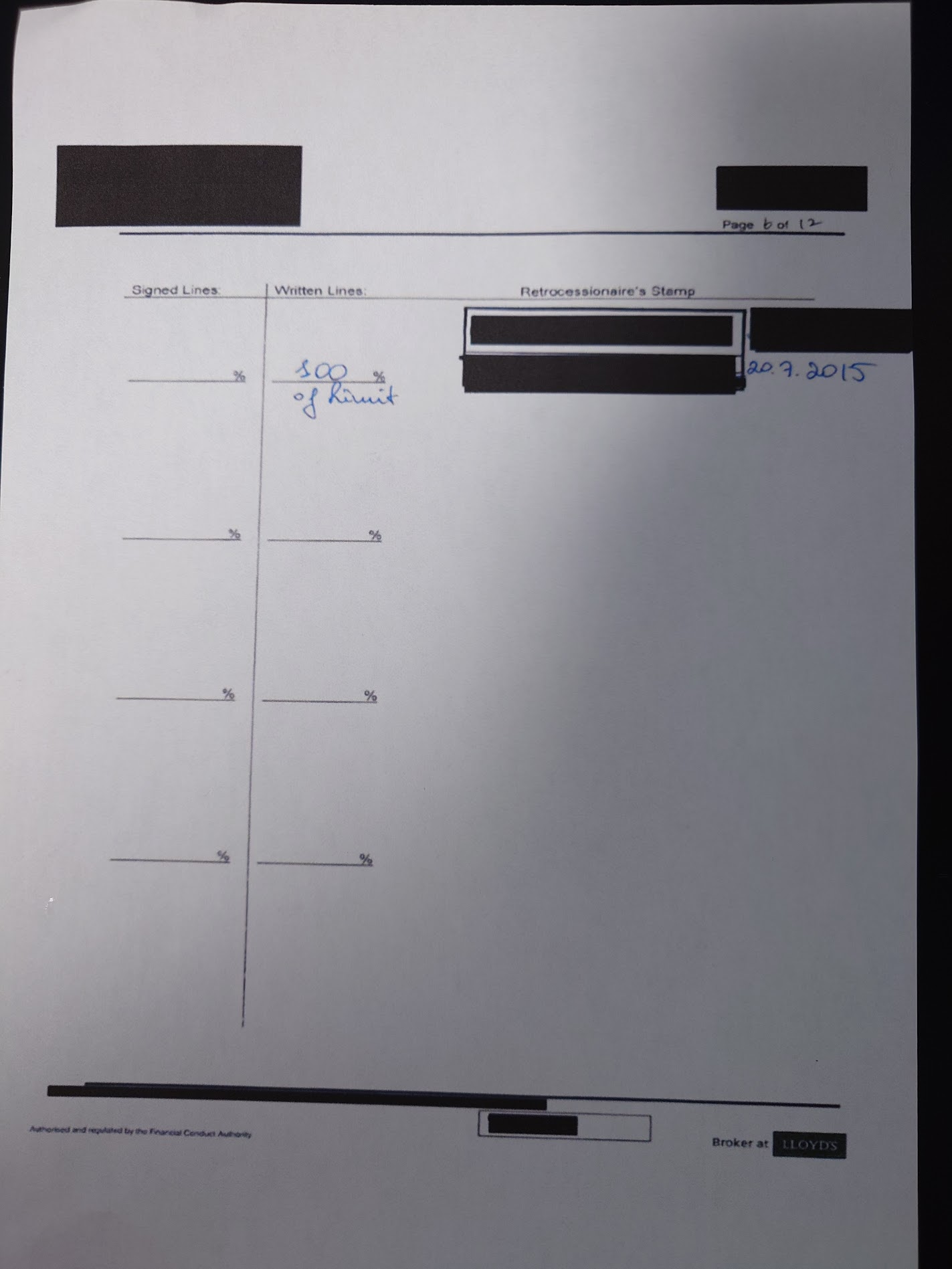

その実物は、上の写真のような形式の書類に、シンジケートもしくは保険会社のアンダーライターが、「補償対象の明細」、「約定文言」、「約款」等のページにサインをした書類が付帯されるものである。この写真の事例の場合「page 6 of 12」と右上にあるように、全部で12ページの書類である。

見えにくいが、右下に「Broker at Lloyd’s」とある。The Lloyd’s broker(ロイズ・ブローカー)が「作成した書類」という意味である。

日本では、「ほとんどの保険契約には、損害保険会社の『代理店』である『保険代理店』が関与する」ため、「補償を担保する保険証券類」は、全て損害保険会社で作成されるが、ロンドン・マーケットは「ブローカー・マーケット」であるため、このようなLine slip(保険証券と同じく補償を担保する)はブローカーが作成しアンダーライターのもとに持参する。

引受の承認を得られた場合は、その証として、このようにシンジケートもしくは保険会社の「スタンプ」が押され、アンダーライターが「サイン」することによってLine slipが完成、補償が開始される。

これは、今から10年前、2015年7月20日、弊社グローバル・リンクのコンサルティングによって、ある企業がハワイに設立した「キャプティブ」からの再々保険をロンドン・マーケットにも一大拠点を持つ、世界最大級の再保険会社が引受けた際のライン・スリップである。

「実物」を見ることが重要だと考えたので、「空欄のLine slip」ではなく、あくまでも「実物」という点に拘った。「実物」を掲載するにあたっては、守秘義務の点から「既に効力は無いライン・スリップ」であるが「できるだけ古いもの」を掲載することにして、更に「黒のマスキング」を施してあることはご容赦願いたい。

この案件の規模が、その再保険会社にとっては、「一社で容易に引受けることができる規模」であったため(といっても当時、そのキャプティブへの再保険を元受保険会社として引受けた日本のあるメガ損保では一社では引受られない規模であったが)、「Written lines: 」(保険引受額)のところには、他のロイズ・シンジケートや再保険会社の名前の記載がなく、この再保険会社のアンダーライターが手書きで「100% of Limit」、2015年7月20日を「20.7.2015」と英国式で記している。

日本の損害保険会社で「元受け」され、ハワイのキャプティブに「再保険」で出されたリスクを更にロンドン・マーケットへ「再々保険」で出したため、「Retrocessionaire‘s Stamp(再々保険スタンプ)」の個所に、この再保険会社のアンダーライターの「引受確認スタンプ」と「アンダーライターのサイン」が記されている。

この案件の場合、一社が再々保険を100%引受けたので「一枚のライン・スリップ」で事足りたが、「巨大なリスク」や「引受が困難なリスクでアンダーライターが高い割合を引受けない」、これらの場合は、多くのアンダーライターが関与するため、このライン・スリップが何枚も「再保険契約明細書:Bordereaux(ボルドロー)」に付帯される。

そうして、リスクが世界中の保険会社、再保険会社へ蜘蛛の巣のように「再保険の形」でリスク分散されていくのである、この方式が編み出され、発達してきた場所が「ロイズ(Lloyd’s of London)」なのである。

⑤ Lead Underwriter(リード・アンダーライター)

上の④Line slip(ライン・スリップ)の項で出てきた言葉に「Lead Underwriter(リード・アンダーライター)」がある。

「Lead Underwriter(リード・アンダーライター)とは、保険リスクの引受に於いて、そのリスクを最初に引受けることに同意したシンジケート、アンダーライターのこと」を言い、その選択はブローカーの腕の見せ所にもなるところである。

最初に「どのシンジケートのどのアンダーライターが、どれくらいの割合で引き受けたか」を見ることによって、次のアンダーライターは引受方針を決めていき、リスク全体が引受けられるか否かが決まると言っても過言ではないからである。

リード・アンダーライターは、「引受条件と保険料率」を決定して、他のシンジケートや保険会社がその保険の引受集団に入ってくるか否かの基準を決める重要な立場であり、「他の損害保険会社と『分担』(シェア)して引受ける」際の中心者となるアンダーライターである。

Lead Underwriter(リード・アンダーライター)が、その保険の分野で、「名前の知れた実績のあるアンダーライターであり、しかも高い割合で引き受けをしている場合」には、フォロー・アンダーライター(この案件をシェアして引受けるアンダーライター)は容易に集まる。

一方、それが「名前の知れた実績のあるアンダーライター」であっても、「低い割合の『引受』であった場合」や、「実績の乏しいシンジケートや名前が知られていないアンダーライター」がLead(リード)した場合には、「アンサポート(Unsupport)」、つまり「リスクが100%が引受けられず、引受不可」となることが多い。

このように、リード・アンダーライターは、保険契約の価格設定、条件の交渉、および他の引受会社(「フォロー市場」)を呼び込む上で中心的な役割を果たすため、ブローカーが、「誰をリード・アンダーライターにするか」を的確に把握しているか否かが重要であり、こういった点から、「The Lloyd’s broker(ロイズ・ブローカー)の選択」が非常に重要なのである。

「この保険分野はこのロイズ・ブローカーが良く知っていて強い、この保険分野はあのロイズ・ブローカー」と、弊社グローバル・リンクでも、保険の種類、必要な補償額等によって、業務提携しているブローカーのみならず、ロンドンで知り合った多くのブローカーのサポートも得ている。

「巨大なブローカーであれば大丈夫では?」という疑問が湧くかもしれないが、「そうとは言えない」のが実情である。「アンダーライターの好み」という点もよく考慮しなければいけないからである。

少なくとも、筆者が知っている約50人ほどのアンダーライター、そのほとんどは、巨大なブローカーより、専門的な知識を豊富に有する小さなブローカーを好んでいたことを憶えている。

「大きいブローカーは、専門的な会話より、ボリュームで引き受けさせようとする傾向が強いから好きではない」と、ある友人のアンダーライターはその意味を正直に語っていた。

だから、グローバル・リンクも、小さな、専門的なロイズ・ブローカー数社と業務提携をしているのである。「あのアンダーライターは、小さいけどあのブローカーと長年の付き合いがあり仲が良い」、実はこんなところからも「良い条件は出てくる」のである。

無論、「グローバル・リンク自身が、長年かけて築いてきた、キャプティブからの地震保険やサイバー保険などの再保険を引き受けてくれる、世界最大級の再保険会社の各部門のアンダーライター達、またロイズのそれらの分野を得意とするシンジケートの多くのアンダーライター達との信頼関係」という背景があるからできることであろう、そう手前味噌ながら思うほど、ロンドン・マーケットで重要なキーワードは「信頼関係」である。

アンダーライティングは「信頼という言葉が最も重要な、非常に人間臭い世界」である。

⑥ Face to Face(フェース・ツー・フェイス)

こういった点からも、ロンドン・マーケットで最も重要な言葉は「Face to Face」であると言える。直接会って、対面でのコミュニケーションを取ることである。

その理由は、「アンダーライティング」は、「目の前に置かれた申込用紙」を「どんな会社のどんな人が、どんな状態で、持参してきたか」というファクターによって、その信頼性や、それによる将来の不確実なリスクが変動するものだからである。「信頼の置けるコミュニケーションが成されたか否かが最も重要な世界」、それが「ロンドン・マーケットでの保険取引」である。

筆者は、今から40年前、1985年、当時勤務していた大手外資系損害保険会社で、米国ニューヨーク本社に研修に行き、1ヵ月後「引受権限(Authority)」を委ねられた。それ以前は、ニューヨーク本社のアンダーライターに全件照会して、引受可否、そして保険料率を決めてもらっていたが、「引受権限の委譲」以降、引受権限を委ねられた150万ドルまでは、「誰に尋ねることなく自分が決めることができる権限」であった。

権限委譲後、わずか1万ドル程の案件が目の前にもたらされたが、「引受可否を決めるのにかなり長い時間思案したこと」をいまだに憶えている。「リスクが怖かった」のである、「事故が起きること」が。

「アンダーライターのその怖さを払拭してあげる作業、それこそが直接会って、話をすること」である。

幸いにも多くの案件を引受けたが、事故は1件も起きることはなかった。しかし、その「怖さ」はずっと、アンダーライターを辞めるまで続いた。「アンダーライティングは、ヒマラヤの険しい切り立った稜線を歩いていくような仕事」と、昔一緒に働いてくれていたスタッフには「怖さを持つ重要性」をよく語ったものである。

損害保険会社の経営コンサルティングを委嘱されていた時、ロイズ(Lloyd’s of London)のあるシンジケートのActive underwriter(アクティブ・アンダーライター:主席保険引受人)とロイズ・ブローカーのCEOを日本に呼んで、営業を担ってくれていた大手財閥系生命保険会社の法人営業部門の全スタッフに対して、「ロイズ・セミナー」と銘打ったセミナーを開いたことがある。そのとき、アクティブ・アンダーライターの言ったことがいまだに耳朶に残っている。

彼は、「アンダーライティングは、ボックスに来た、目の前のトニー(ロイズ・ブローカーのCEO)を見て、『今日は奥さんと喧嘩はしていないかな』とまず観察するところから始まる」と、皆の笑いを誘いながら、しかも、「アンダーライティングの核」を見事に語ったのである。

「『目の前にある紙に書かれたデータ』だけで的確なアンダーライティングができるか」と問われたら、答えは「No」と、元アンダーライターの筆者としては答えるだろう。「紙に書いてあることを補完する事項、事象の方が重要なことが多いのが普通だから」である。目の前にいるブローカーが「言わなければいけないことを言わないようにしているのか」、「何かを隠しているのか」、それとも「紙にはこう書いてあるが、こういう事実も事象もある」と言ってくれるかどうか、それによって的確なアンダーライティングができるかどうかが決まる。だから、「Face to Face」が重要なのである。

「なぜ、10数年も2ケ月に1回もの頻度でロンドンに出張した」のか、その答えはこの「Face to Face」を実現するためであった。出張日のタイミングによっては、「See you next month(来月また会おう)」という出張も2度や3度ではなかった。

そのために「海外出張など無いに等しい生命保険会社の経理部門を相手」に、今は同僚となった菅原執行役員が、毎年その予算取りにどれほど苦労したかと感謝している。

その結果、ロイズ(Lloyd’s of London)のアンダーライター諸氏からは「羽谷はロンドンに通勤しているみたいだな」とさえ言わしめることができ、惹いては、それが「最高水準の再保険カバーを得る=比類なき競合優位性を持つ保険商品の開発と販売」を可能にした。

親会社は巨大な生命保険会社でありながらも損害保険会社の方は、同じ旧財閥グループ内の競合損保と比べて、「象と蟻」であったが、「その蟻が、多くの案件で、象を倒し、日本のその保険の市場全体の10%超の占有率を得ることができた、その核が『Face to Face(フェース・ツー・フェイス)』」だったのである。

12.終わりに

この小論考を書くにあたって、「Face to Face(フェース・ツー・フェイス)」をどれだけ実践してきたかを確かめるため、筆者が搭乗してきたメインの航空会社のマイレージを調べてみた。

| 生涯マイル |

855,606マイル (国内線 65,818 マイル 国際線 789,788 マイル) |

| 生涯搭乗回数 |

250回 (国内線 117 回 国際線 133 回) |

この生涯マイルは、地球約 34.4周、月まで約 1.8往復、総搭乗時間は約 2281.6時間に相当します。

こう記されていた。

但し、このマイレージは「航空券を買って搭乗した回数と距離」を示しているものであり、「最高時には300万マイルを超えたマイレージを利用して何十回もロンドン他の出張に利用」した。このため、コロナ禍でロンドンに出張できなくなる直前2020年1月までの全「生涯フライト記録」を調べてみた。

ロンドンに出張した回数は、合計で75回(搭乗回数150回)、ニューヨーク、シドニーへ出張した回数は36回(搭乗回数72回)となっていた。つまり、国際線の総搭乗回数は222回であった。

すべて「Face to Face(フェース・ツー・フェイス)」のためである。

保険ビジネス、特に再保険という「アンダーライターが直接顧客に会えない案件」の場合、アンダーライターは「その顧客の姿」そして「補償するリスク」の実像にできる限り迫りたいと思うものである、アンダーライターは「恐怖と戦いながら仕事をしているから」である。

コロナ禍のなかでも、「ロンドンに行こう」と何度も飛行機を予約した、しかし、次々に続いて出てくる「コロナの亜種ウイルスの蔓延」の状況から、スタッフまた家族から何度もその出張を止められ、ほとんどの仕事を「オンライン打ち合わせ」でおこなってきた。また、丸の内に借りているグローバル・リンクの事務所にもほとんど行くこともなく、これまたオンラインで済ますことがほとんどになった。

しかし、保険はやはり「Face to Face(フェース・ツー・フェイス)」が基本中の基本であることは、ロイズ(Lloyd’s of London)のことを本小論考にまとめながら思い出していた。ロイズ(Lloyd’s of London)に教えられた思いである。

そして、「メール」や「オンライン画面」だけで、長らく会えていない多くの旧友に会いに、「新たなビジネスの芽」を探しに、ロンドンに行くことを決めた。

この「ロイズ(Lloyd’s of London)ー キャプティブからリスクが行き着く先ー」と題した5回の連載を終えるにあたって、第1回から記し続けてきたロイズ(Lloyd’s of London)のことを改めて考えてみた。

英国は「歴史と伝統の国」と呼ばれる、ロイズ(Lloyd’s of London)も同様に「保険の歴史と伝統を体現している組織」と言えるだろう。

「歴史と伝統」と言うと何か古臭いものを想像しがちだが、ロイズ(Lloyd’s of London)が「常に状況に対応して変化しながら進化してきた」ことは、「『迅速な情報の入手が事業の進展のカギを握る』と考えてロンドン中央郵便局のすぐ隣に事務所を移転する」、「『リスクの分散が事業の安定性のカギを握る』と考えてLine slip(ライン・スリップ)を生み出す」等々、リスク・マネジメントの本義である「外的要因、内的要因を分析して対応してきた姿」で、明確にそれを示している。

だからこそ、本コラムに記した事柄も明日には大幅に変化している可能性もある。常に「進化」を考えている組織なのである。

「種の起源」(「進化論」)で有名なチャールズ・ダーウィンは、「この世に生き残る生物は、最も強いものではなく、最も知性の高いものでもなく、最も変化に対応できるものである」という考えを示したと言われている。

しかし、実のところ、「種の起源」にこの言葉はなく、「後世の創作」と言われているが、事業経営においてこれほど重要な言葉はないであろう。これを体現しているからこそ、ロイズ(Lloyd’s of London)は300年を超えて「損害保険の頂点」に立ち続けている。

これこそ、我々がロイズ(Lloyd’s of London)から学ぶべきことではないだろうか。

執筆・翻訳者:羽谷 信一郎

あとがき

長年、ロンドン・マーケットに通い詰め、ロイズ(Lloyd’s of London)については、シンジケートのアンダーライター達、ロイズ・ブローカー達から多くのことを学ぶことができました。また、「ロイズ(Lloyd’s of London)」全体の運営管理をおこなう組織である「Corporation of Lloyd’s」についても、同社の多くの方々と知り合う機会がありました。

その中心、「世界戦略を統括する取締役」であった、Jose Ribeiro(ホセ(英国人は、ジョセと発音)・リベイロ)」と初めて会ったのは、彼がロイズ(Corporation of Lloyd’s)に入社してすぐの2007年。それ以来、私のコンサルティング先であった損害保険会社にも何度も来社して親しい友人となり、ロンドンに出張した際には必ず彼と会っていました。

そんな彼を通して色々な方々とも知り合い、様々な情報にも接していたので、幸いなことにロイズ(Lloyd’s of London)についてはかなりの知見を得ることができていました。

(2015年:Jose Ribeiroと筆者)

因みに、彼はその後、ロイズ(Corporation of Lloyd’s)を退社、保険の格付会社のA.M.Bestの役員を経て、世界的に著名なロンドンのビジネス・スクール、インペリアル・カレッジ・ビジネス・スクール(Imperial College Business School))の客員講師に就任。

「(元々が教師だったので)落ち着いたのか」と思っていたら、数年前、また金融の世界にも関与することになり(https://www.nurole.com/news-and-guides/jose-ribeiro-non-executive-director-hansard-worldwide)、「NED(Non-Executive Director:非常勤取締役)」としてですが、非常勤としては異例の頻度、「月5日勤務」なので、客員講師、ポルトガルにあるワイナリーの経営と合わせて、忙しい日々を送っているようです。

コロナ禍も明けたようなので、彼をはじめ多くのアンダーライターやロイズ・ブローカーの友人たちに会いたいなと思っていたところ、弊社の公式WEBサイトに、「ロイズのことを色々と調べていたのですが、よく解らなくて困っていたところ、貴社のホームページのコラム記事を見て・・」というお問い合わせがあり、このことがきっかけとなり、本小論考の執筆を決めた次第です。

「お問い合わせに、正しく、適切にお答えするために」と、改めて色々と調べてみましたが、ロイズに関する本は少なく、かつどれも40年程前に出版されたものばかりでした。

当時は正しかったのでしょうが、状況が大きく変化しており、「富裕層がアンダーライターをしている・・」と、現況とは全く異なっている記述も多く、またネット情報を調べてみても古いものばかり、新しいものでも2019年のロイズの組織変更以前のものしか見つけることはできず、私が知る現状とは大きな乖離が感じられました。

また、「実際にロイズ(Lloyd’s of London)のシンジケートとビジネスをおこなってきた視点では書かれていないため、実像になかなか迫れないのでは・・・」とも感じ、「ロイズ(Lloyd’s of London)との実務経験者の視点で整理しておきたい」と思い立ちましたが、書き上げてみたら、「短く」と思っていたのですが、「5回連載の分量」となってしまいました。

これも、長年、ロイズ(Lloyd’s of London)にお世話になってきた身として、ロイズ(Lloyd’s of London)のことを正しく理解していただく一助になればと思った次第であり、ご容赦頂きたいと思っております。

English Translation

Copyright © Shinichiro Hatani 2025 All rights reserved

Unauthorised reproduction, quotation or duplication of the contents within this column is strictly prohibited.

Captive (CA)78 Lloyd’s of London – Part 5 (Final instalment) — Where Risk Lands from Captives —

③ Lessons from the London Market

Lloyd’s of London and the London Market are characterised by ‘risk sharing’.Recently in Japan, the practice of non-life insurers sharing underwriting responsibilities with other non-life insurers for large corporate insurance transactions has, for some reason, been viewed critically. To this writer, this appears truly peculiar.

The reason is that risks covered by non-life insurance, unlike those in life insurance, are highly uncertain and the likelihood of unforeseen events occurring is high. Therefore, it is crucial to have as many and as robust risk hedging measures as possible.

The technique devised for this risk dispersion is reinsurance. Naturally, dispersing risk across the reinsurance networks of multiple non-life insurers yields greater benefits than relying on a single insurer’s network. It creates a larger risk dispersion network, enhances the stability of coverage, and consequently increases the stability of the non-life insurers themselves, as well as the certainty of claims payments. From these perspectives too, the risk dispersion technique that should be promoted is precisely ‘sharing the risk’.

Lloyd’s of London has endured for over 300 years, navigating numerous challenging circumstances, and this can be attributed solely to its thorough implementation of this “risk diversification” principle.

④ Line slip

The very method of risk diversification and risk sharing practised at Lloyd’s of London and in the London Market is the line slip.

The official website of Lloyd’s of London states the following regarding line slips, which is quoted below.

A line slip is an agreement whereby a Managing Agent delegates its authority to enter into contracts of insurance to be underwritten by the members of a syndicate managed by it to another Managing Agent or authorised insurance company in respect of business introduced by a Lloyd’s Broker named in the agreement.

Managing Agents do not require approval from Lloyd’s to operate under a line slip.

Once the Managing Agent or insurance company acting as the line slip lead underwriter has entered into a contract of insurance with the insured, the evidence of insurance will normally be issued by means of a MRC contract or via a certificate / policy. The format of the insurer authorised documentation will be determined within the line slip agreement.

A line slip is an agreement whereby a Managing Agent delegates to another Managing Agent or an authorised insurance company the authority to conclude insurance contracts underwritten by members (underwriters) belonging to syndicates under its umbrella, in respect of business introduced by a Lloyd’s of London Broker named in the agreement.

The Managing Agent requires no approval from Lloyd’s of London to execute business under the Line Slip.

When the Managing Agent or an insurance company acting as Lead Underwriter under the Line Slip enters into an insurance contract with the assured, proof of insurance is typically issued via the MRC contract or a certificate/policy. The format of the insurer’s authorised documentation will be determined within the line slip agreement.

Indeed, the document indicating “sharing” (share) of underwriting with other syndicates and/or non-life insurance companies is the “Line slip”.

The actual document consists of a form like the one pictured above, to which the syndicate or the insurance company’s underwriter attaches a signed document containing pages such as “Details of Cover”, “Agreed Terms”, and “Policy Conditions”. In the example pictured, as indicated by “page 6 of 12” in the top right corner, the document comprises a total of 12 pages.

Though faint, the words ‘Broker at Lloyd’s’ appear in the bottom right corner. This signifies that the document was ‘prepared by’ a Lloyd’s broker.

In Japan, ‘most insurance contracts involve an “insurance agency”, which is an “agent” of the non-life insurance company’. Therefore, ‘insurance policy documents guaranteeing cover’ are all prepared by the non-life insurance company. However, the London Market is a ‘broker market’. Consequently, such Line slips (which, like insurance policies, guarantee cover) are prepared by the broker and brought to the underwriter.

Upon obtaining underwriting approval, the Line slip is finalised and cover commences when the syndicate or insurer’s “stamp” is applied as evidence of this approval and the underwriter “signs” it.

This is a line slip from when, ten years ago on 20 July 2015, a major reinsurance company – one of the world’s largest with a significant presence in the London market – underwrote reinsurance from a captive established in Hawaii by a certain company, facilitated by our firm Global Link’s consultancy.

I considered it important to see the “actual item”, so I insisted on the “actual item” rather than a “blank line slip”. Whilst publishing the “physical document”, please understand that, due to confidentiality obligations, we have opted to display a “line slip that is no longer in force” whilst still being “as old as possible”, and have further applied “black masking”.

The scale of this deal was such that the reinsurance company could readily underwrite it alone (though at the time, it was too large for a single Japanese mega-non-life insurer, which had originally underwritten reinsurance for that captive). (Insurance Amount Underwritten) section contains no names of other Lloyd’s of London syndicates or reinsurance companies. Instead, the underwriter of this reinsurance company has handwritten ‘100% of Limit’, with the date 20 July 2015 written in British format as ‘20.7.2015’.

As the risk was originally underwritten by a Japanese non-life insurer, reinsured to a Hawaiian captive, and then retroceded to the London market, the ‘Retrocessionaire’s Stamp’ section bears the underwriter’s ‘acceptance confirmation stamp’ and ‘underwriter’s signature’ for this reinsurance company.

In this deal, as one company underwrote 100% of the retrocession, a single line slip sufficed. However, for ‘massive risks’ or ‘difficult-to-underwrite risks where underwriters won’t accept high proportions’, multiple underwriters become involved. Consequently, several line slips are attached to the reinsurance contract schedule: Bordereaux.

And thus, risk is dispersed like a spider’s web to insurance companies and reinsurers worldwide in the form of reinsurance. It was at Lloyd’s of London that this system was devised and developed.

⑤ Lead Underwriter

The term ‘Lead Underwriter’ appears in section ④ Line slip above.

A Lead Underwriter is the syndicate or underwriter that first agrees to underwrite the insurance risk. Selecting this underwriter is where the broker’s skill comes into play. It is no exaggeration to say that by first examining ‘which underwriter from which syndicate underwrote what proportion’, subsequent underwriters determine their underwriting policy, thereby deciding whether the entire risk can be underwritten.

The Lead Underwriter holds a crucial position, determining the ‘underwriting terms and premium rates’ and setting the criteria for whether other syndicates or insurance companies join the underwriting syndicate for that insurance.

When the Lead Underwriter is a well-known, experienced underwriter in that insurance field, and is underwriting a high proportion of the policy, follow underwriters (those sharing the underwriting of this deal) are readily attracted.

Conversely, even if the Lead Underwriter is a “well-known underwriter with a proven track record”, if they have a “low underwriting ratio” or if the Lead is a “syndicate with limited experience or an underwriter without a recognised name”, the result is often “Unsupport”, meaning “the risk cannot be underwritten at 100% and is therefore uninsurable”.

Thus, as the lead underwriter plays a central role in setting the insurance contract price, negotiating terms, and attracting other underwriting companies (the “follow market”), it is crucial that the broker accurately understands “who to appoint as the lead underwriter”. For these reasons, “the selection of the Lloyd’s broker” is of paramount importance.

At our firm, Global Link, we leverage the expertise of our partner brokers and numerous other brokers we’ve met in London, selecting the appropriate broker based on the insurance type and required coverage amount – for instance, ‘this Lloyd’s broker is well-versed and strong in this insurance field, while that Lloyd’s broker handles this other field.’

One might wonder, ‘Wouldn’t a large broker suffice?’ but the reality is that this is not necessarily the case. The “underwriter’s preference” is also a crucial factor that must be carefully considered.

At the very least, I recall that the vast majority of the approximately 50 underwriters I knew preferred smaller brokers with extensive specialist knowledge over large brokers.

‘I dislike large brokers because they tend to push for volume rather than engaging in specialised discussions,’ a friend who is an underwriter once candidly explained.

Consequently, Global Link has formed business partnerships with several small, specialist Lloyd’s brokers. ‘That underwriter has a long-standing, good relationship with that small broker’ – it is precisely through such connections that ‘favourable terms emerge’.

Naturally, this is possible because of the background of ‘the trust relationships Global Link itself has built over many years with underwriters from various departments of the world’s largest reinsurance companies who accept reinsurance for earthquake insurance and cyber insurance from captives, as well as with many underwriters from Lloyd’s of London syndicates specialising in those fields.’ It is no exaggeration to say that the key word in the London market is ‘trust relationships’.

Underwriting is ‘a profoundly human world where trust is paramount.’

⑥ Face to Face

For these reasons, the most crucial phrase in the London market is “Face to Face”. It means meeting directly and communicating face-to-face. Why? Because “underwriting” involves judging how to reduce the reliability and uncertain risks of the data written on the paper in front of you, based on the factor of “who brought it”.

Some forty years ago, in 1985, whilst working for a major foreign-affiliated non-life insurance company, I attended a training programme at the US headquarters in New York. One month later, I was entrusted with “underwriting authority”.Prior to this, every case required consultation with underwriters at the New York headquarters to determine acceptability and premium rates. However, after the “delegation of underwriting authority”, I possessed the authority to decide independently on cases up to $1.5 million without consulting anyone.

Shortly after this delegation, a deal worth merely around $10,000 was brought before me. I still vividly recall spending a considerable amount of time deliberating over whether to accept it. I was afraid of the risk – afraid that an accident might occur.

The task of dispelling that fear in the underwriter was precisely to meet face-to-face and talk.

Fortunately, I accepted many deals without a single accident occurring, yet that “fear” persisted until I left underwriting. “My work is like walking along the steep, jagged ridgelines of the Himalayas,” I often told staff who worked with me back then, stressing the “importance of maintaining that sense of fear”.

When commissioned to provide management consultancy for a non-life insurance company, I once hosted a seminar labelled the “Lloyd’s Seminar”. I invited the Active Underwriter (Chief Underwriter) of a Lloyd’s of London syndicate and the CEO of a Lloyd’s broker to Japan. The audience was the entire corporate sales department staff of a major zaibatsu-affiliated life insurance company responsible for our business. What the active underwriter said then still rings in my ears.

He remarked, ‘Underwriting begins with observing Tony (the Lloyd’s of London broker CEO) who has just arrived at the desk, thinking “I wonder if he’s had a row with his wife today?”’ This elicited lol from the audience, yet he brilliantly articulated the ‘core of underwriting’.

If asked, “Can you perform accurate underwriting based solely on the data written on the paper in front of you?”, the answer would be “No”, as I, a former underwriter, would respond. This is because, typically, the matters and circumstances that supplement what’s written on paper are often more crucial. Whether the broker sitting before you is “withholding something they ought to say”, “concealing something”, or whether they will say, “While the paper states this, there are also these facts and circumstances” – this determines whether accurate underwriting can be performed. That is why “Face to Face” is so important.

The reason for travelling to London every two months for over a decade was precisely to achieve this “Face to Face”. Depending on the timing of the trip, there were more than a few occasions where it was a “See you next month” visit.

For this reason, I am grateful to my colleague, Executive Officer Sugawara, who now handles the budget, for the considerable effort he expended annually to secure funding when dealing with the accounting departments of life insurance companies, where overseas business trips were virtually unheard of.

However, the result was that underwriters at Lloyd’s of London even remarked, ‘It seems Hatani is commuting to London,’ which in turn this enabled us to secure the highest level of reinsurance cover, leading to the development and sale of insurance products with unparalleled competitive advantage. Though our parent company was a giant life insurer, our non-life division was, within the same conglomerate group, a mere “ant” compared to competing non-life insurers. Yet that “ant” toppled the “elephant”, capturing over 10% of the insurance market. The core of that achievement was “Face to Face”.

12. Conclusion

While writing this brief essay, the author investigated the mileage accumulated with the main airline they have flown.

Lifetime Miles

855,606 miles

(Domestic: 65,818 miles / International: 789,788 miles)

Total Flights Taken

250

(Domestic: 117 International: 133)

These lifetime miles equate to approximately 34.4 times around the Earth, roughly 1.8 round trips to the Moon, and a total flight time of about 2,281.6 hours.

It was recorded thus.

However, these miles represent “the number of flights taken and distances flown after purchasing tickets”. At peak times, he utilised over 3 million miles for dozens of business trips to London. Consequently, I examined his entire “lifetime flight record” up to January 2020, just before the covid-19 pandemic prevented further London trips.

The total number of business trips to London was 75 (150 flights), while trips to New York and Sydney totalled 36 (72 flights). In other words, the total number of international flights taken was 222.

All were for ‘Face to Face’ meetings. In insurance business, particularly reinsurance – where ‘underwriters cannot meet clients directly in a deal’ – underwriters naturally wish to get as close as possible to the ‘actual presence of that client’ and the true nature of the ‘risk being covered’. This is because underwriters ‘work while battling fear’.

Even amidst the covid-19 pandemic, I repeatedly booked flights thinking ‘I must go to London’. However, the successive emergence of new covid-19 variants led to staff and family repeatedly advising against the trip, and most of my work was conducted via online meetings. Furthermore, I scarcely visited the Global Link office rented in Marunouchi, with most matters also handled online.

Yet, while compiling this brief essay on Lloyd’s of London, I recalled that insurance fundamentally relies on face-to-face interaction. This is a lesson imparted by Lloyd’s of London.

Thus, I resolved to visit London. To meet many old friends, I haven’t seen for a long time, relying only on emails and online screens, and to seek out new business opportunities.

As I conclude this five-part series entitled “Lloyd’s of London – Where risk ultimately ends up from captives”, I found myself reflecting once more on Lloyd’s of London, a subject I have covered since the very first instalment.

Britain is often called a ‘country steeped in history and tradition’, and similarly, Lloyd’s of London can be described as an organisation that ‘embodies the history and tradition of insurance’.

Whilst ‘history and tradition’ might conjure images of something antiquated, Lloyd’s of London has ‘constantly evolved by adapting to circumstances’. This is seen in decisions such as ‘relocating its offices immediately adjacent to the General Post Office, believing that “rapid access to information was key to business progress”’, and creating the line slip, believing that “risk diversification is key to business stability”. These actions clearly demonstrate the essence of risk management: analysing and responding to both external and internal factors. Precisely because it is an organisation constantly contemplating “evolution”, the matters recorded in this column may well change significantly tomorrow.

Charles Darwin, famed for The Origin of Species (the “theory of evolution”), is said to have expressed the idea that “the species that survive are not the strongest, nor the most intelligent, but those most responsive to change”.

However, in truth, these words do not appear in The Origin of Species and are considered a later addition. Yet, in business management, there are scarcely more important words. It is precisely because Lloyd’s of London embodies this principle that it has remained at the pinnacle of non-life insurance for over 300 years.

Is this not what we should be learning from Lloyd’s of London?

Author/translator: Shinichiro Hatani

Afterword

Over many years of frequenting the London Market, I learnt a great deal about Lloyd’s of London from syndicate underwriters and Lloyd’s broker in the London insurance market.

I also had the opportunity to become acquainted with many individuals at Lloyd’s of London.

My first meeting with Jose Ribeiro (pronounced “Jose” by the British), who was central to this and served as the Director overseeing global strategy, took place in 2007, shortly after he joined Lloyd’s of London.

Since then, he visited my consulting client, a non-life insurance company, on numerous occasions, becoming a close friend. Whenever I travelled to London on business, I would invariably meet with him.

Through him, I also came to know various other individuals and gained access to diverse information. Consequently, I was fortunate to acquire considerable insight into Lloyd’s of London.

(2015: Jose Ribeiro and the author)

Incidentally, he subsequently left Lloyd’s of London, served as an executive at the insurance rating agency A.M. Best, and then took up a position as a visiting lecturer at the globally renowned at the globally renowned London business school, Imperial College Business School.

I thought, “Has he settled down (since he was originally a teacher)?” But then, a few years ago, he became involved in the financial world again (https://www.nurole.com/news-and-guides/jose-ribeiro-non-executive-director-hansard-worldwide), as a Non-Executive Director (NED), but at an unusual frequency – working five days a month. Combined with his role as a visiting lecturer and managing a winery in Portugal, it seems he leads a busy life.

As a Non-Executive Director (NED), he works an unusually high frequency of five days per month. Combined with his role as a visiting lecturer and managing a winery in Portugal, he appears to lead a very busy life.

With the covid-19 seemingly behind us, I had been thinking how I’d like to meet him and many other underwriter and Lloyd’s broker friends again. Then, on our company’s official website, we received an enquiry stating: ‘I was researching various aspects of Lloyd’s of London but was struggling to understand it all, when I came across the column article on your company’s website…’ This prompted me to decide to write this short essay.

In order to respond correctly and appropriately to the enquiry, I revisited my research. However, I found very few books on Lloyd’s of London, and those that existed were all published around 40 years ago.

While they were likely accurate at the time, circumstances have changed significantly. Many descriptions, such as ‘the wealthy act as underwriters…’, are completely at odds with the current situation. Furthermore, when I searched online, I found only outdated information; even newer sources only covered the period before Lloyd’s of London organisational changes in 2019, creating a noticeable disconnect from the reality I know.

Moreover, I felt that ‘since they weren’t written from the perspective of someone who has actually conducted business with Lloyd’s syndicates, they struggle to capture the true picture…’. This led me to think, ‘I want to organise this from the perspective of someone with practical experience working with the Lloyd’s of London. However, once I finished writing, what I intended to be “short” ended up being ‘enough for a five-part series’.

As someone who has long been indebted to Lloyd’s of London, I hope this may serve to aid in a proper understanding of Lloyd’s of London, and I would ask for your indulgence.