キャプティブ 2025.09.30

CA79 ロイズ(Lloyd’s of London)連載(全5回分一括掲載) ー キャプティブからリスクが行き着く先ー

目次

- 1. はじめに

- 2. 損害保険の生成

- 3. ロイズ(Lloyd’s of London)の誕生

- 4. ロイズ(Lloyd‘s of London)の揺籃期

- 5. ロイズ(Lloyd’s of London)の発展

- 6. ネルソン提督

- 7. 現在のロイズ(Lloyd’s of London)

- 8. ロイズ(Lloyd’s of London)に関わる存在・関係者

- 9. ロイズ(Lloyd’s of London)の表す意味

- 10.ロイズ(Lloyd’s of London)の仕組みと構造

- 11.ロイズ・マーケットでの取引

- 12.終わりに

- 1. Introduction

- 2. The Origins of Non-Life Insurance

- 3. The Birth of Lloyd’s of London

- 4. The Formative Years of Lloyd’s of London

- 5. The Development of Lloyd’s of London

- 6. Admiral Nelson

- 7. Lloyd’s of London Today

- 8. Entities and stakeholders involved with Lloyd’s of London

- 9. The Meaning Represented by Lloyd’s of London

- 10. The Mechanism and Structure of Lloyd’s of London

- 11. Trading at the Lloyd’s Market

- 12. Conclusion

Copyright © Shinichiro Hatani 2025 All rights reserved

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

ロイズ(Lloyd’s of London)に関し、8月29日「CA74 ロイズ(Lloyd’s of London)ー 連載第1回」として投稿を開始した本連載ですが、「名前はよく知られていても、内容は損害保険会社の社員でも関係者を除き、あまり知られていない非常に専門的な分野」にも関わらず、思いのほか多くの方々にご覧いただき、また「これまでよく分からなかったロイズのことがよく分かりました」とのコメントも頂き感謝しております。

同時に、「今後とも参考にしたいので、内容を一覧できるように、全5回分を一括して投稿して欲しい」旨のご要望も合わせて寄せられた方も多かったため、シームレスに読んでいただけるように、以下に、全5回分を一括して再掲載することに致しました。

なお、5回分のコラムを1回にまとめたため、かなりの長文になりましたが、最後までご覧いただけると幸いです。

全5回分一括掲載

大手財閥系生命保険会社から、1997年設立したばかりの損害保険子会社及び同事業への経営コンサルティングを委嘱され13年間、毎年2カ月に1回、ロイズ(Lloyd’s of London)を中心としたロンドン保険市場(ロンドン・マーケット)へ通いつめ、キャプティブ事業を開始してからも、毎年数回ロンドンに出張してきた。このことによって得た知見から、日本ではあまりよく知られていないロイズ(Lloyd’s of London)について、以下の項目に沿って記していきたい。

|

目次 |

|

| 1. | はじめに |

| 2. | 損害保険の生成 |

| 3. | ロイズ(Lloyd’s of London)の誕生 |

| 4. | ロイズ(Lloyd‘s of London)の揺籃期 |

| 5. | ロイズ(Lloyd‘s of London)の発展 |

| 6. | ネルソン提督 |

| 7. | 現在のロイズ(Lloyd’s of London) |

| ① 市場(マーケット) | |

| ② ロイズ・ビル内の「アンダーライティング・ルーム」 | |

| ③ Marine(マリン:海上保険)フロア | |

| ④ Non-Marine(ノンマリン:海上保険以外の種目すべて)フロア | |

| ⑤ 再保険市場 | |

| ⑥ アンダーライター(引受権限保持者) | |

| 8. | ロイズ(Lloyd’s of London)に関わる存在・関係者 |

| 9. | ロイズ(Lloyd’s of London)の表す意味 |

| 10. | ロイズ(Lloyd’s of London)の仕組みと構造 |

| 11. | ロイズ・マーケットでの取引 |

| ① ロイズ・ビルへの入館 | |

| ② ロイズ・ブローカー(The Lloyd’s broker) | |

| ③ ロンドン・マーケットから学ぶこと | |

| ④ Line slip(ライン・スリップ) | |

| ⑤ Lead Underwriter(リード・アンダーライター) | |

| ⑥ Face to Face(フェース・ツー・フェイス) | |

| 12. | おわりに |

1. はじめに

第二次世界大戦後、世界経済の中心は「一つの例外」を除きすべてが英国を中心とするヨーロッパから米国に移り、米国を中心にして世界の経済活動が行われていると言っても過言ではないが、この「一つの例外」とは損害保険分野のことである。

「想定外の損害が起きることは殆ど考えられない」と言える生命保険分野と異なり、損害保険分野では、損害保険会社の存亡に関わるような巨大リスクを引き受けることも多く、「再保険の手配」はその企業戦略の最重要課題となっているが、この再保険手配の地は、米国ではなく、ロイズ(Lloyd’s of London)を中心とした英国、ロンドンの金融街、シティの地である。

世界中の保険会社、また顧客と保険会社との保険・再保険取引の仲介を行なう保険仲立人(ブローカー)が、数多くの事務所、事業所を開設している。日夜、保険取引や再保険取引を行っているロンドンは、世界の保険・再保険の中心地であり、「損害保険の開発、特にその再保険手配先」として、「ロンドン・マーケット」と呼ばれている。

2. 損害保険の生成

損害保険発祥の地については、中近東、ギリシャ等の諸説があるが、いずれの説も、その発祥理由は「外国との貿易のため海上輸送をおこなった際に損害を被った荷物」に関するリスク・ヘッジ(回避)の手段として生成したというものであり、現在の海上保険に類するものが損害保険の起源と考えられている。

この「海上保険」は、14世紀のイタリアでほぼ完成したと言われているが、その萌芽は、12~13世紀にイタリアを中心とした地中海交易で使われていた「冒険貸借」というものであると言われている。

ただ、この「冒険貸借」は、現在の海上保険の仕組みとは、少し異なっている。海上保険では、交易をしたいと思っている貿易業者が、保険会社に対し保険料を支払い、万が一貨物を失った場合には、保険会社より損失金額の補償を受けるものである。

一方、冒険貸借は、物を仕入れて船を借り交易をしたいと思っている貿易業者が、資本家から貿易に必要な資金を借り受けることに始まり、航海が無事に終われば、貿易業者は、借りていた元金に利息を上乗せして資本家に返済するが、もし事故や海賊に遭って貨物が全損となった場合は、貿易業者は、借入金を資本家に返済することを免除された仕組みであった。

その意味で、冒険貸借で資金を提供した資本家は、保険会社というよりは、現代のベンチャーキャピタルに近い存在と考えることができる。

その為もあってか、航海が無事に終わった時に資本家に支払う利息は、1航海につき20%~30%と非常に高い金利であった。このことは、また当時の地中海交易は、リスクが高いが、成功すれば、いかに莫大な富みを得ることができるベンチャーであったかを窺い知れる証拠にもなっている。

このように、冒険貸借は「資金調達」と「危険負担」という2つの機能を果たしていたが、「海上保険の理論と実務」(木村栄一編:「弘文堂」刊)によると、1230年頃、「貸し借りで高利を受取ることはキリスト教の教えである隣人愛に反する」との考えから、ローマ法皇グレゴリオ9世によって徴利禁止令(=利息禁止令)が発令され、冒険貸借は禁止された。

しかし、交易をする以上、資金調達と危険負担は必須のものであり、徴利禁止令に抵触しない手法が様々に案出され、資金調達と危険負担を完全に分離して、冒頭述べたとおり、14世紀頃、冒険貸借から危険負担機能のみを取り出した、現在の海上保険の原型がイタリアで完成した。

今日、国際貿易で使用されているロンドン保険業者協会(Institute of London Underwriters)の「協会貨物約款(=海上貨物保険約款)」 (ICC: Institute Cargo Clauses)にも大要が受け継がれているほど、当時の海上保険約款の完成度は非常に高く、その意味でも保険会社の安定経営に資するものであったことが想像できるものである。

3. ロイズ(Lloyd’s of London)の誕生

ロンドンに出張する際、ジョギングが趣味であった筆者が長年定宿にしているホテルは、その場所に恰好な「ハイドパーク」に面し、地下鉄「ランカスター・ゲート駅」の真上にある。

毎朝、シティに向かう地下鉄「セントラル・ライン」に乗り、「バンク(Bank)駅」に向かう。到着して地上に上がると、目の前には2つの道がシティへ、その中心地でもあるロイズ(Lloyd’s of London)へと向かっている。一つは「Cornhill(コーンヒル)」であり、もう一つは「Lombard Street(ロンバード・ストリート)」である。

「ロンバード・ストリート」は、英国王エドワード1世(1272〜1307年)によって、イタリア北部のロンバルディア地方からの移民に与えられた土地の区画であったため、この名称が残されている。移民の多くは、金細工職人であったが、当時の最先進国であったイタリアからは、金融、そして保険の仕組みも、英国の地に伝わった。

(ロンバートストリート16番地にある、第2代目ロイズ・コーヒーハウスの跡地)

このロンバード・ストリートは、400メートルほどでGracechurch street(グレースチャーチ・ストリート)にぶつかるところで終わり、道を挟んでその先はFenchurch street(フェンチャーチ・ストリート)に名前が変わる。

後述するが、ロンバード・ストリートの中程にあるのが、上記写真にある「青いプレート」(ブルー・プラーク (blue plaque) と呼ばれる、英国内に設置されている史跡案内板)、「ロイズ・コーヒーハウス(現ロイズ:Lloyd’s of London)が、1691年から1785年まであった場所を示す銘板」である。

この地は英国、ロンドンの金融の中心地として、1980年代までは、英国に本拠を置くほとんどの銀行の本店、本社は、ロンバード・ストリートにあった。

初めてロイズ(Lloyd’s of London)の名前が文献に顕れたのは、「1688年2月発行の新聞、ガゼット紙」、その広告面であった。これが、歴史上初めて、「保険業者としてのロイズ(Lloyd’s of London)」の名前が現れたものであった。

このようにして、当時の最先端のビジネスモデルであった、「金融」と「保険」が、ロンドンのシティ、ロンバード・ストリートを中心に成熟、発展、現在でもロンドンは「世界の損害保険の中心地」としての地位を保っているのである。

4. ロイズ(Lloyd‘s of London)の揺籃期

現在、「バンク(Bank)駅」から、歩いて数分の場所に、「ロイズ」(Lloyd‘s of London)の建物がある。

「One Lime Street(ライム・ストリート1番地)」と通称される、「ロイズ(Lloyd’s of London)ビル」。その正面玄関の入り口には、「大型の自動回転扉」がある、どこでもほんの少しでも触れるとすぐ止まる、またその傍には警備を兼ねたスタッフ2名が不測の事態が起きないようにいつも目を光らせている。

1600年代末、エドワード・ロイドが、当時の社交場、商取引の場所として人気が出始めていた「コーヒーハウス」(喫茶店)をロンドン観光の定番スポットである「タワーブリッジ」の傍ら、タワーストリートに開いた。その店は、彼の名前を冠して「エドワード・ロイドのコーヒーハウス(Edward Lloyd’s Coffee House)」と呼ばれた。Lloyd’s(Lloyd’s of London) の淵源である。

大西洋に注ぎ込むテムズ川の河口沿いにある街が、ロンドンである。このため多くの海運業者が店に集まり、海事ニュースを発行して有名になった。海運業者、荷主が集まれば、「海上運送リスクをどうするか」が当然、話題の中心、保険を引き受ける商人が自然と誕生した。

コーヒーハウスには、保険の引受の検討をするため、「船名、船歴、荷物、船長、航海のスケジュール等々」が描かれたボードが掲げられ、その下に「引き受ける人間」が引受割合を記し、サインをした。この伝統は、今でも「保険証券の下の方にサインすること」で受け継がれているが、そのためこの保険を引き受ける人のことを「Underwriter(アンダーライター)」と呼ぶようになったといわれている。

当時、保険会社は存在せず、商人が保険を引き受け、その使用人が、他の商人の間を持ちまわって、共同で保険を引き受けていた。保険のビジネスが大きくなっていくと、元々はアンダーライターの経営する会社の使用人だった人たちが独立して、アンダーライターと保険を掛けたい人たちの間を取り持つ「保険仲介業」をおこなうようになり、彼らのことを「ブローカー」(保険仲立人)と呼ぶようになった。彼らが相互に連携した「保険市場」が店のなかに生まれたのである。

この保険を引き受ける富裕者が集まった集団が構成され、時を経てその集団引受組織は「シンジケート」と呼ばれるようになった。さらに、ブローカーが仲介して、他のシンジケートとともに引き受けしてリスク分散を図るようになっていった、引受組織がブローカーの仲介によって、他のシンジケートとともに共同引受をして、リスク分散を図る、現在のロイズ(Lloyd’s of London)の淵源がここにある。

5. ロイズ(Lloyd’s of London)の発展

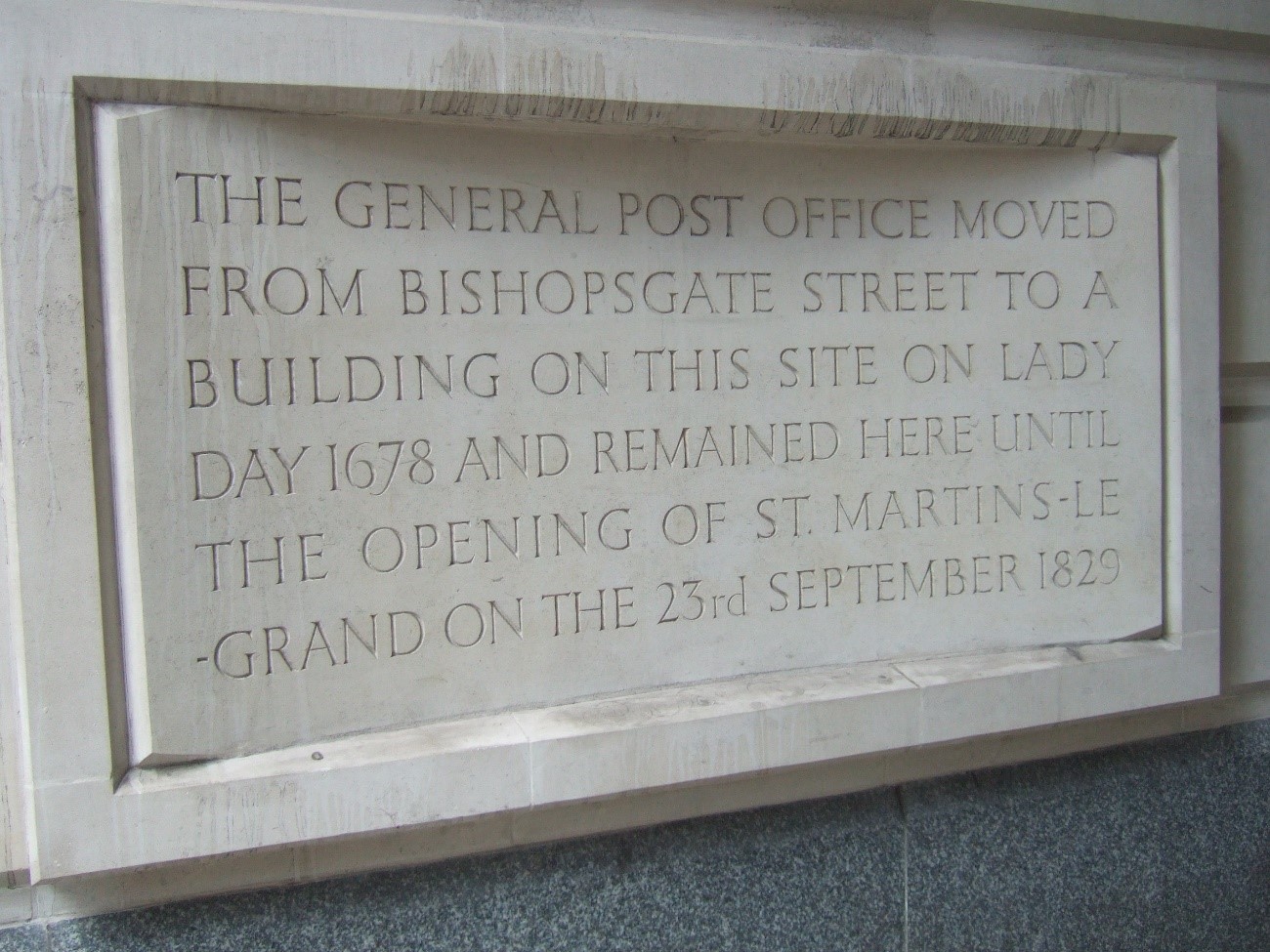

(「ロンドン中央郵便局」の銘板:1678年~1829年)

ビジネスの規模も大きくなってきたため、ロイズ・コーヒーハウスでは手狭となり、1691年、当時も、また今もビジネス街の中心地であるロンドンのシティの一角、前述の「青いプレート」がある「ロンバード・ストリート16番地」にロイズ(Lloyd’s of London)は移転した。

この移転の理由は、1678年この場所のすぐ隣にロンドン中央郵便局が建ち、世界中の情報が郵便という手段で集まってくる、その「中心地」に最も近い場所だったからである。郵便配達のシステムが完備された現代と違い、17世紀最も早く郵便を受け取る手段は、郵便局の中につくられた私書箱を開けることであった。

企業戦略上、この郵便制度の重要性に早くから気がつき、その恩恵を受けた世界的な機構が、ロイズ(Lloyd’s of London)である。

「なぜ、一保険取引業者にしか過ぎなかったロイズ(Lloyd’s of London)が、今日世界的規模の一大保険市場になり得たのか」と問われたら、「企業戦略上、自らの事業に於いて通信手段が如何に重要であるかということを的確に理解して、その戦略の策定と実行をおこなったからである」と答えるであろう。

ロイズ(Lloyd’s of London)は、「2代目ロイズ・コーヒーハウス」の建物に移転して以降、海外の情報をどの競合社よりも早く得ることができるようになった。18世紀になると海上保険を独占的に扱う保険業者として大きく成長した。

1770年代の米国独立戦争では、「海上保険が、如何に重要であるか」を実証、その最大規模の提供者としてロイズ(Lloyd’s of London)は、世界的規模で海上保険を支配するまでの存在になっていったのである。

もし、「ロンドン中央郵便局」の傍に移転していなければ、そうなってはいなかっただろう。ロイズ(Lloyd’s of London)は、「迅速な情報伝達の重要性」に気がつき世界規模の保険機構へ成長したのである。

6. ネルソン提督

ヨーロッパ大陸を席巻した皇帝ナポレオンの軍隊は、英国への上陸を果たすべく大侵攻軍を組織、1805年10月21日、スペイン沖トラファルガーで英軍と激突した。「トラファルガーの海戦」である。狙撃兵の銃弾に倒れながらも見事に指揮したネルソン提督のもと、英軍は一方的な大勝利を飾った。その戦勝を記念して、ロンドンの中心部に造られたのが「トラファルガー広場」である。

下の写真は、海上保険を通して海と縁が深いロイズ(Lloyd’s of London)の本拠地、ロイズ・ビルの1階にある、ネルソン提督の遺品や記念品が展示されている、「ネルソン提督コーナー」の一部を写したものである。

7. 現在のロイズ(Lloyd’s of London)

最も英国的な食文化は「Pub (パブ)」ではないだろうか、英国中の街や村には必ずと言っていいほどパブがある。ある意味「お酒の飲める喫茶店のような存在」と言えるだろうか、そのため日本語の「酒場」や「居酒屋」という言葉に翻訳するとニュアンスがかなり異なってくるため、日本でも「パブ」と呼ばれることが多い。

昔は、ロイズ・コーヒーハウス(Lloyd’s Coffee House)がその役目を果たしたが、ロイズ(Lloyd’s of London)や再保険会社のアンダーライター達と最初に案件の話しをする場は、ロイズ・ビルのなかでも、また彼らがロイズ(Lloyd’s of London)近くに持っている事務所のなかでもなく、ほとんどの場合パブでおこなうのが「ロンドンの保険業界の常識」である。

「なぜ飲みながら話をするか」、それは「その方が『ブローカーの本性』も『案件の本当のところ』もよく見えるから」である、アンダーライター達のリスクマネジメントでもある。

午前10時、「ロイズが開く」時間帯から、シティ中のパブが一斉に「保険市場」となる。昔のパブは、手頃な価格で宿泊施設を提供するだけでなく、実は旅人のための替え馬を用意、そのため厩舎も併設していたが、現代ではシティのパブは「保険市場」となり、多くのアンダーライターとブローカーが「パイント・グラス」を傾けながら、案件の話をして、「引受可能かどうか」を見極める、その「最初の場」がパブである。

(現在のロイズ・ビル)

① 市場(マーケット)

「モノを売り買いする場所」が市場(マーケット)である。築地市場は豊洲に移転して豊洲市場となり、水産物、青果物の売り買いをおこなっている。保険の売り買いをおこなっている「マーケット」とは、主にロイズ(Lloyd’s of London)を指す言葉であるが、ロイズを中心に世界中の何千という数の保険会社や保険ブローカー(保険仲立人)が事務所を構えているため、シティ(ロンドン金融街)の一角、「保険ブロック」全体が「マーケット」とも呼ばれている。いわゆる「ロンドン・マーケット」である。

(ロイズ・ビル内の「アンダーライティング・ルーム」)

保険の売り買いの仲介をするのが、保険ブローカー(保険仲立人)である。「保険市場のなかの保険市場」と言われるロイズ(Lloyd’s of London)、その取引場所(アンダーライティング・ルーム)は、上の写真のようになっている。

ロイズ(Lloyd’s of London)で保険引受けをおこなおうとする企業、その多くが損害保険関係の会社であるが、彼らが、保険引受けをおこなうアンダーライターが所属する組織体である、「シンジケート」を組成しようと考えた場合、ロイズ(Lloyd’s of London)全体の管理運営会社であるCorporation of Lloyd’s(コーポレーション・オブ・ロイズ:通称、the Lloyd’s Corporation:ロイズ・コーポレーション)の承認を受けるため、まずシンジケートを運営管理する会社を設立する。その会社は「マネージング・エージェント」(シンジケート保有管理会社)と呼ばれ、アンダーライター、事務職員等を雇用して保険引受を可能にしていくのである。

マネージング・エージェントは、いくつものシンジケートを傘下に置く場合もあるが、一つのシンジケートのみ保有する場合もある。

(ロイズ・ビルの内部、1階(米国、日本式では2階)から地上階(米国、日本式では1階)の海上保険のアンダーライティング・フロアを臨む)

② Marine(マリン:海上保険)フロア

メインフロアのGround Floor (地上階)は、Marine(マリン:海上保険)のアンダーライターのシンジケートが占有している。保険の引受可否、条件を決めるアンダーライターが所属する組織体が「シンジケート」である。「シンジケート=保険を引受ける会社=保険会社」と考えても差し支えないが、前述のとおり、保険会社そのものではなく、保険会社等がロイズ(Lloyd’s of London)のなかで保険を引き受ける際に設立する組織体である。

③ ルーティン・ベル

ロイズを説明するときに外せない言葉に「ルーティン・ベル」がある。ロイズ・ビルのGround floor(地上階:Marine(マリン:海上保険)フロア)に置かれている。「ロイズ(Lloyd’s of London)にとって、悪いニュースがあったときには1回、良いニュースがあったときには2回鳴らされる、「ロイズ(Lloyd’s of London)を象徴するベル」のことである。

1805年トラファルガーの海戦において、前述のネルソン提督率いる英国が仏ナポレオン軍に打勝ち、仏ナポレオン海軍のフリゲート艦、La Lutine(ラ・ルーティン)を拿捕してHMS Lutine(ルーティン)と改名、英国海軍に加えたが、25年後この船が沈没した。

この時、その船舶・貨物の保険を引き受けていたのは、当然ロイズ(Lloyd’s of London)であり、保険金の支払額は百万ポンドだったといわれている。これは、現在の価値では8000万ポンドに相当、円貨に換算すると100億円を超す金額となる。

ロイズ(Lloyd’s of London)は、回収のためこの船の引き上げに手を尽くすが成功せず、80年後の1859年、ようやく成功、その引き上げられたサルベージ品(遭難船からの引き上げ品)のなかで、「最も重要な品」とされたのが船の鐘、それがロイズ(Lloyd’s of London)に運び込まれ、以来ロイズ(Lloyd’s of London)を象徴するものとして、今に至るまで、ロイズ・ビルの保険引受場所(アンダーライティング・ルーム)の中心に置かれている。

(ロイズ・ビルの地上階にある「ルーティン・ベル」)

④ Non-Marine(ノンマリン:海上保険以外の種目すべて)フロア

First Floor(英国式呼び方では「1階」、日本式では「2階」)には、Non-Marine(ノンマリン:海上保険以外の種目すべて)のシンジケートのアンダーライターが「店を構えて」いる。

Second Floor(英国式では「2階」、日本式では「3階」)は、Company Marketと呼ばれ、保険会社のアンダーライターが所在する場所である。

筆者は、30年ほど前、当時世界最大と言われた、米国のCIGNA Corporation(フィラデルフィア本社)に勤務していたが、ロンドンに3ヶ月間OJT研修のため出張をした。その際、午前10時から午後4時までアンダーライターとして勤務した場所がこのSecond Floor。その前と後の時間帯は、ロイズ近くのCIGNAのビルで準備仕事や終了後のまとめをしていた。

シンジケートが、ロイズ(Lloyd’s of London)のなかで開いている、この「店のこと」をBox(ボックス)と呼ぶ。終日Boxにいるアンダーライターは背もたれのある椅子に座り、上の写真でも分かるとおり、通路側にある背もたれのない椅子にはそのアンダーライターとリスクの引受可否の交渉に来たブローカーが座る。

「なぜ、背もたれがないか」、それは「長時間アンダーライターを独占しない、させない」というロイズの不文律に起因すると聞く。

それが証拠に、ロイズのなかでアンダーライターと15分を超えて話しをしている「素人のブローカー」がいた場合、アンダーライターからやんわりと、もしくは直裁に「退席を求められる」ことがある。

⑤ 再保険市場

再保険とは、「保険会社(もしくは同様の保険機構)が引受けたリスクを別の保険会社(もしくは同様の保険機構)にリスクを移転するために保険を掛けることをいい、引受けた保険に「再」び「保険」を掛けるから、「再保険」という。

冒頭記したとおり、損害保険分野を除いてすべての産業が、第二次世界大戦以降、英国を中心とするヨーロッパより米国に移り、米国を中心にして世界経済は動いている。しかし、保険、特に損害保険は全く異なる。損害保険の世界の中心地はいまだにロンドンである。

保険数理士(アクチュアリー)の計算に基づき保険を引き受ける生命保険分野では、「想定外の損害」が起きることはほとんど無いため、生命保険分野において、再保険は一般的ではないが、損害保険分野では事業の存亡に関わる可能性のある巨大リスクを引き受けるため、「再保険の手配」は最重要戦略となっている。その再保険手配の世界の中心地が、前述のロイズ(Lloyd’s of London)を中心とした英国ロンドンの金融街、シティである。

保険契約者が保険会社から保険を購入することによって、「移転されたリスク」は、その更なるリスク移転(リスク・ヘッジ)のため再保険会社等が構成する再保険市場に移転されることになるが、この動きと流れはあたかも蜘蛛の巣のように多方面に移転されていく。このため、保険会社(元受保険会社)から再保険市場へのリスクの移転は、リスクの移転ではなくリスクの分散と呼ばれることが多い。

保険契約を保険契約者から引き受けた元受保険会社は、再保険専門の保険会社と再保険契約をすることが再保険手配の中心であるが、再保険専門の再保険会社だけが再保険事業を行っているのではない。再保険の引受部門(子会社)を有する元受保険会社グループが再保険を引き受けているケースも多い。

したがって、再保険市場は、再保険専門保険会社に限らず多数の保険会社(保険機構)が取引をする市場となっている。そのため、世界中の保険関係者にとってみると、再保険会社であろうと元受保険会社であろうと、「再保険を引受けてくれるプレーヤーが、世界で一番多く一箇所に集中している場所」での取引が、効率的にビジネスを進めることができるため好まれる。その場所、世界の再保険市場の地がロンドンなのである。

⑥ アンダーライター(保険引受人・引受権限保持者)

アンダーライターが別のシンジケート(別の保険会社)に転職すれば、顧客も一緒にそのシンジケートに移っていくことは非常に多い。それほど、「アンダーライターと顧客(保険契約者)との関係は深い」と言える。

8. ロイズ(Lloyd’s of London)に関わる存在・関係者

「ロイズ(Lloyd’s of London)の公式WEBサイト」では、ロイズ(Lloyd’s of London)に関係してビジネスをおこなう人たちを区分して、下記のように記している。 (邦訳:筆者)

The policyholder(保険契約者):

They could be businesses, organisations, other insurers and individuals from around the world looking to mitigate the impact of potential risks. And it’s not only the everyday risks they’re looking to cover. But also complex and unique ones, like protecting a business from cybercrime or insuring first-of-its-kind technology.

保険契約者は、潜在的なリスクが損害に至る衝撃を緩和しようとしている、企業、組織、また他の保険会社、世界中の人たちになるでしょう。 また、彼らが保険によって補償を得ようとしているものは日常的なリスクだけではありません、サイバー犯罪からビジネスを護る、最先端の技術を保険補償するなど、複雑でユニークなものもあります。

The local broker(現地(保険契約者の国)の保険ブローカー):

They are the first contact for a policyholder. They work in the local market where the policyholder is based. They’ll assess the policyholder’s needs and decide if it’s more suitable for the Lloyd’s marketplace.

彼らは、保険契約者の最初の連絡、相談先です。 彼らは、保険契約者が存在する現地の市場で事業をおこなっています。 彼らは、保険契約者のニーズ、意向を評価し、それがロイズの市場で保険の補償を得る方がより良いかどうかを判断します。

The Lloyd’s broker(ロイズ・ブローカー):

They work on the policyholder’s behalf, negotiating with underwriters to create a tailored policy to insure the risk.

彼らは、保険契約者の権益を代表して、リスクに対する補償を記したオーダーメイド型の保険証券を創りあげるため、保険引受人(アンダーライター)と交渉する業務をおこなっています。

この項には、弊社グローバル・リンクと業務提携しているロイズ・ブローカーの1社、大手総合商社丸紅の100%子会社、マルニックス、その子会社マルニックス(ヨーロッパ)の名前がロイズ・ブローカー約400社(2024年末現在)のうちの1社として、下記のように記されている。

Marnix Europe Limited

River Plate House、7-11 Finsbury Circus London United Kingdom EC2M 7AF

Tel: +44 (0)20 7826 8693 Fax: +44 (0)20 7826 8695

The underwriter(アンダーライター:保険引受人ー引受権限保持者):

They work with other specialist underwriters and the Lloyd’s broker to draw up the policy. Each underwriter will decide on the price and terms they’re willing to take.

彼らは、他の専門的なアンダーライターやロイズブローカーと連携して保険証券を発行します。それぞれのアンダーライターは、それぞれが保険を引受けるために望む保険料価格と保険の引き受け条件を決定します。

Active Underwriter(アクティブ・アンダーライター):

The individual at the underwriting box with principal authority to accept insurance and reinsurance risk on behalf of the members of a syndicate.

シンジケートの構成員を代表して、アンダーライティング・ボックスに於いて、保険および再保険のリスクを引き受ける、その主席権限を有する者。

The syndicate(シンジケート:保険引受組織):

They are made up of underwriters who group together to form a syndicate to write insurance at Lloyd’s. Underwriters enter into insurance contracts on behalf of Lloyd’s syndicates. Each syndicate is given a number by Lloyd’s to identify them.

彼らは、ロイズで保険証券を発行するためにシンジケートを形成してグループ化したアンダーライター達で構成された組織です。 アンダーライター達は、そのロイズのシンジケートを代表して保険契約の締結をおこないます。 各シンジケートには、ロイズによってそのシンジケートの識別番号が与えられます。

ロイズ(Lloyd’s of London)には、2024年末で80あまりのシンジケートが存在している。

The managing agent(マネージング・エージェント:シンジケート保有管理会社):

They are a company set up to manage one or more syndicates. Managing agents are responsible for employing the underwriters.

彼らは、1つもしくはそれ以上の数のシンジケートを管理するために設立された会社です。 マネージング・エージェントは、アンダーライター達を雇用する責任があります。

2024年末現在、約50社のマネージング・エージェントが存在している。

上の「登場人物・組織」に記されている、The Lloyd’s broker(ロイズ・ブローカー)とThe underwriter(アンダーライター)が保険の取引をする場所、つまり「保険市場」がロイズ(Lloyd’s of London)である。

したがって、ロイズ・アンダーライター、ロイズ・ブローカーへ、「ロイズとは?」と聞くと、みなすべてが「マーケット:市場」と答える、その場所がロイズ(Lloyd’s of London)である。

9. ロイズ(Lloyd’s of London)の表す意味

Lloyd(ロイド)という言葉が「人の姓」であるため、英国第4位の規模を有する銀行グループ、「ロイズ・バンキング・グループ (Lloyds Banking Group plc) 」をはじめ実に多くのLloyd(ロイド)という単語を冠した企業が存在する。そういった企業と区別するため、保険機構・市場であるロイズは、ロイズ(Lloyd’s of London)と保険関係者の間では呼ばれている。

この「ロイズ(Lloyd’s of London)」という言葉には次の2つの意味がある。

•「国際的な保険市場としてのロイズ」:英国ロンドンのシティにある保険市場であり「Lloyd’s Market (ロイズ・マーケット)」と呼ばれている。

•「法人としてのロイズ」:英国議会制定法によって法人化された団体である、ブローカー及びシンジケートを会員とする組織全体(日本では、ロイズ保険組合と呼称されることが多い)であり、「Corporation of Lloyd’s」 (Lloyd’s Corporationとも通称される)と呼ばれている。

このCorporation of Lloyd’s(ロイズ保険組合)は、ブローカーとアンダーライターを会員とする自治組織であるが、Corporation of Lloyd’s(ロイズ保険組合)自体が保険引受業務を行うのではなく、シンジケート(アンダーライター)が保険を引受け、Corporation of Lloyd’s(ロイズ保険組合)はロイズ・ビルを所有し、取引の場(アンダーライティング・ルーム)と保険引き受け業務に関する事務処理サービスを会員に提供するために存在しているのである。

従来、保険引受けをおこなうのは、保険金の支払に上限を定めない無限責任を負う個人の富裕層(Name:ネーム)であった。しかし、1990年代初頭に始まった「アスベストによる多額の保険金支払い」によって、多くのName(ネーム)が破産宣告され、急速にName(ネーム)は減少、現在では引受ボリュームの1~2%程度しか提供していない。

代りに、1994年に導入された有限責任の法人会員制度によって参入を許可された、多くの巨大企業がマネージング・エージェントを設立して多くのシンジケートを組成、現在では、ロイズの引受の太宗を占めている。

10.ロイズ(Lloyd’s of London)の仕組みと構造

仕組み

「ロイズ(Lloyd’s of London)」は、よく「英国の保険会社ロイズ」と紹介されるが、本小論考で繰り返し述べてきたとおり、「ロイズ(Lloyd’s of London)は保険会社ではなく保険市場」である。

2018年築地から豊洲に移転した「豊洲市場」を思い浮かべると「ロイズの仕組み」が理解できるのではないだろうか。

世界から集まる水産物や青果物を流通させる重要な拠点である「豊洲市場」は、マグロの競り(せり)など、国内外から集まる水産物や青果物の取引が行われる「卸売場」、卸売業者から仕入れた水産物や青果物を、飲食店や小売店に販売する仲卸業者の店舗が集まる「仲卸売場」 から成り立っている。

一方、「保険市場」であるロイズ(Lloyd’s of London)は、「リスクの売買」をおこなう場として、「リスクを売りたい(=買って欲しい)人々」が、「ロイズ・ブローカー」を仲介者として、「シンジケートのアンダーライター」と「個別の競り(せり)をおこない、売買をおこなう場」と言えるだろう。

「豊洲市場の『卸売場』と『仲卸売場』を一か所」にして、取引所である「アンダーライティング・ルームに集めた仕組み」、それがロイズ(Lloyd’s of London)である。

Lloyd‘sの公式WEBサイトで、「市場の評判を保護および維持するために行動し、業界の知識ベースにサービスと独自の調査、レポート、分析を提供する独立した組織および規制当局である」とされている、「ロイズ(Lloyd’s of London)」全体の運営管理をおこなう組織がある。

それが、ロイズ(Lloyd’s of London)の公式WEBサイトで、大きく「Lloyd’s Corporation」(ロイズ・コーポレーション)と紹介されている、前述の組織である。しかし、そのページの下には「Lloyd’s Copyright 2025 Lloyd’s and Corporation of Lloyd’s are registered trademarks of the Society of Lloyd’s. 」( ロイズの著作権 2025 ロイズおよび「Corporation of Lloyd’s」は、「Society of Lloyd’s」の登録商標です)とある。

(引用:「ロイズ( Lloyd’s of London)公式WEBサイト」)

ロイズ法での正式名称は「Corporation of Lloyd’s」(コーポレーション・オブ・ロイズ)であるが、なぜか「これら2つの名称が同時に「ロイズ(Lloyd’s of London)」によって使用されている」のである。

このことについて、筆者は「Lloyd’s Corporationは通称だろう」と考えたが、2つの名称が混在していることが理解できなかったので、ロイズ・ブローカーとして数十年の経験を有するプロ中のプロの旧友に、「For some reason, Lloyd’s official website introduces it as “Lloyd’s Corporation”, yet its official name under the Lloyd’s Act is “Corporation of Lloyd’s”. Why is that? (なぜかロイズの公式ウェブサイトでは「ロイズ・コーポレーション」と紹介されているが、ロイズ法に基づく正式名称は「コーポレーション・オブ・ロイズ」である。なぜだろうか?)」と聞いたところ、返ってきた答えが以下であった。

「No, do not really know why the two forms of reference are used !!(いや、なぜ2つの参照形式が使われているのか、全くわからない!!)」、と。彼でさえ理解できないとのこと。まことに不可思議な現象である。

いずれにしても、ロイズ(Lloyd’s of London)は、機能的には保険の引受をおこなう「シンジケートの集合組織体」とその組織を管理、統治する組織である「Corporation of Lloyd’s」(コーポレーション・オブ・ロイズ)(Lloyd’s Corporationとも通称される)に、コーポレート・ガバナンスの点で分化しているということである。

構造

この「Corporation of Lloyd’s」(コーポレーション・オブ・ロイズ)は、ロイズという巨大な「保険市場」の規則を定め、規制、管理、運営する法人であるが、個々の保険契約を引き受けるのは、あくまでも「シンジケート」である。そして、これら全体を指して「ロイズ(Lloyd’s of London)」と呼んでいる。

英国の議会法である、前述のロイズ法(Lloyd’s Act 1982)が、ロイズ(Lloyd’s of London)における管理構造と規則を定めている。

この法律では、ロイズ(Lloyd’s of London)の正式名称は、「Society of Lloyd’s(ソサイエティ・オブ・ロイズ)」と定められているが、知り合いのアンダーライター、ブローカーの誰もがそうは呼ばず、「Lloyd’s of London」と呼んでいる、これまた不思議な事象である。

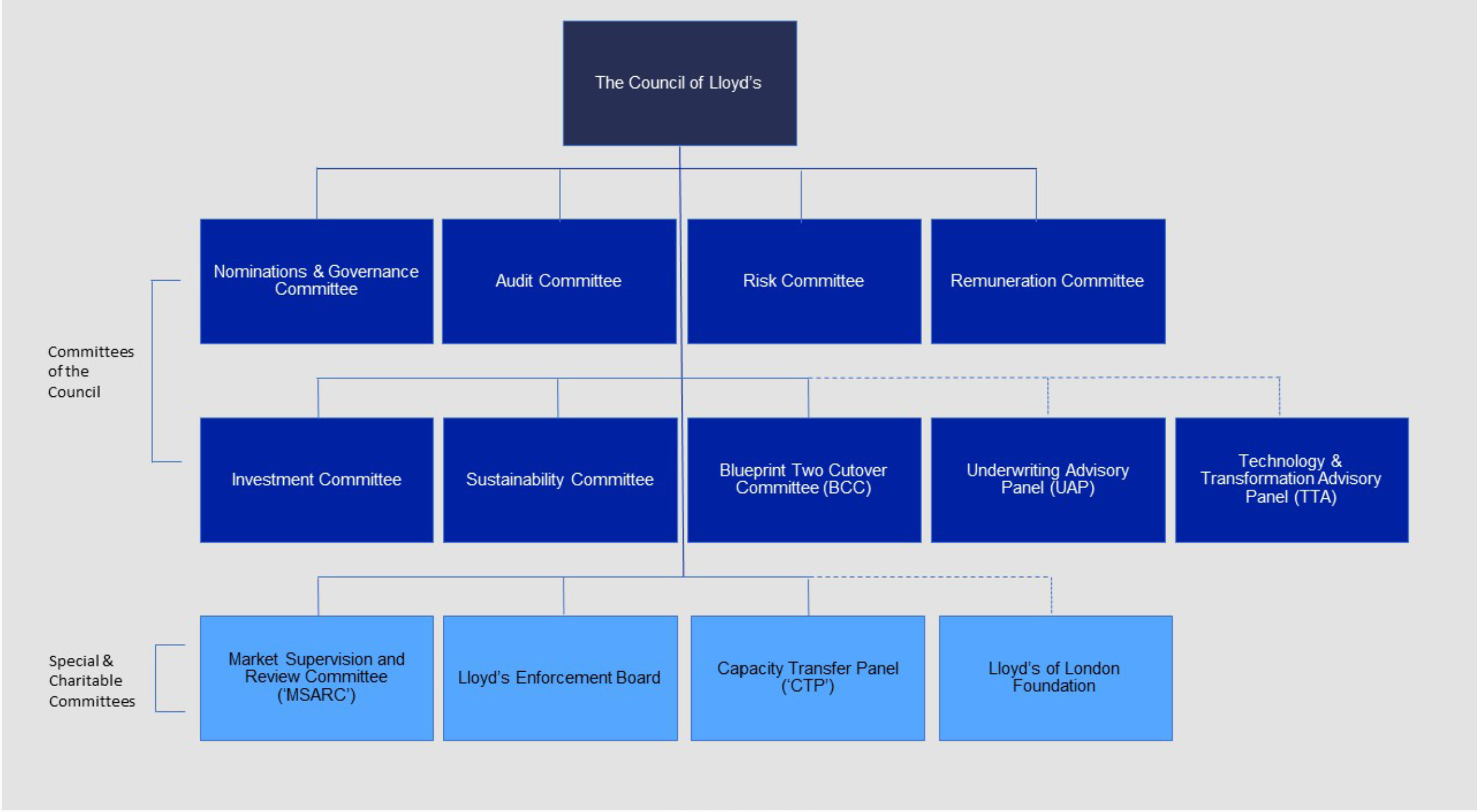

ロイズ法(Lloyd’s Act 1982)には、ロイズ評議会(Council of Lloyd’s)が、「ロイズ(Lloyd’s of London)全体の管理と監督に関する責任を負っている」と定められている。

評議会には、通常、3人の実務委員、3人の外部委員、9人の指名委員がいる。実務メンバーと外部メンバーは、ロイズ(Lloyd’s of London)のメンバーから選出され。議長と副議長は、評議会によって、毎年、そのメンバーの中から選出される。

このロイズ評議会(Council of Lloyd’s)は、ロイズ(Lloyd’s of London)全体の規則、細則を決定するが、ロイズ・マーケットの運営に関連する日常的なガバナンスは、以前、そのほとんどはフランチャイズ委員会(Franchise Board)に委任していた。そういう趣旨のロイズ(Lloyd’s of London)に関する資料、レポート等もあるが、2019年この委任を廃止、ロイズ評議会(Council of Lloyd’s)にコーポレート・ガバナンスを一本化、組織も下記のとおり変更された。

(出典:「ロイズ( Lloyd’s of London)公式WEBサイト」)

このように、ロイズ評議会(Council of Lloyd’s)は、上記の組織を通じてロイズ(Lloyd’s of London)市場に存在する、すべてのシンジケートへの「ガイドライン」を定め、引受とリスク管理を適正におこなうための事業計画とその進捗を随時ウオッチしているが、個々の保険商品の開発、保険引受に関与することはない。それは「シンジケートがおこなう分野」だからである。

11.ロイズ・マーケットでの取引

① ロイズ・ビルへの入館

経営コンサルタントの時は、保険商品の開発、キャプティブ事業を開始してからは、キャプティブからの再保険の手配のため、提携している保険ブローカー、再保険会社との打ち合わせのために足繁く通ってきたロンドン。先にロイズ・ビルの紹介で、「『バンク(Bank)駅』から、歩いて4,5分の場所に『ロイズ』(Lloyd‘s of London)の建物がある」と紹介した。

これは、前述のとおり、筆者が長年、毎年6回、ロンドンに通っていた際に定宿にしていたホテルが、その駅に止まる地下鉄「セントラル・ライン」のランカスター・ゲート駅の真上にあり、この「セントラル・ライン」を使って、シティ、「ロイズ」(Lloyd‘s of London)に通っていたからである。

この地下鉄がロンドン市街を初めて走ったのは、日本では「幕末時代」の1863年であった。その200年前、1666年、大火がこのロンドンを襲った。現在では、米国のウオール・ストリートとならび「国際金融街」として有名な「シティ」と言われる一角に通じる地下鉄の駅、その一つに、「ディストリクト・ライン」や「サークル・ライン」の駅、モニュメント駅がある。

モニュメント駅に降り立つと、その駅前には、まさにその名のとおり、モニュメント(記念碑)がたっている。「街を焼き尽くす勢いであった」とその壁面のレリーフに彫り込まれている大火を記念した「ロンドン大火記念塔」The Monument to the Great Fire of Londonである。高さは、その場所から火元とされた「パン屋」までの距離と同じ62m。そこから、歩いて数分のところにロイズ(Lloyd ‘s of London)がある。

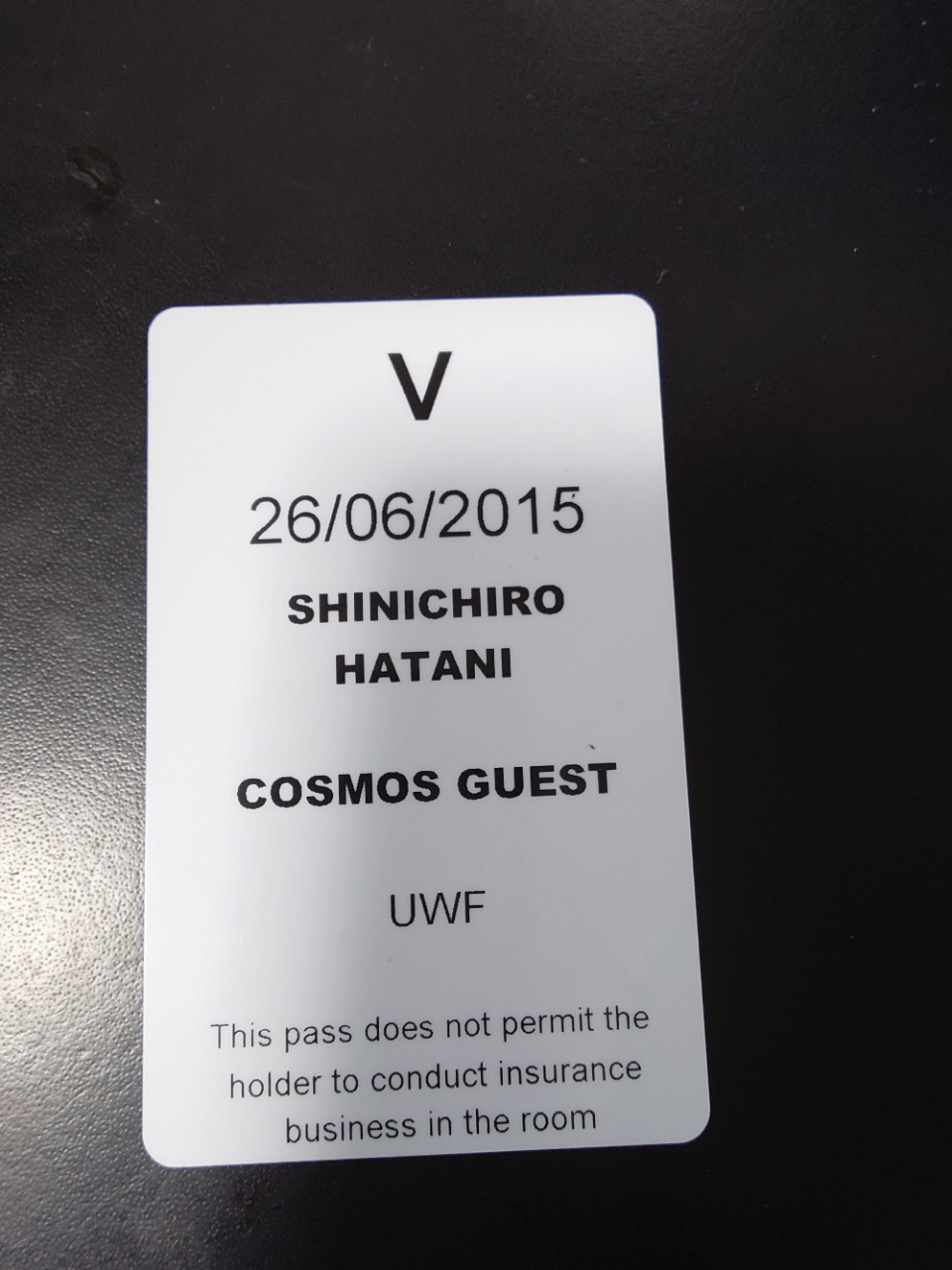

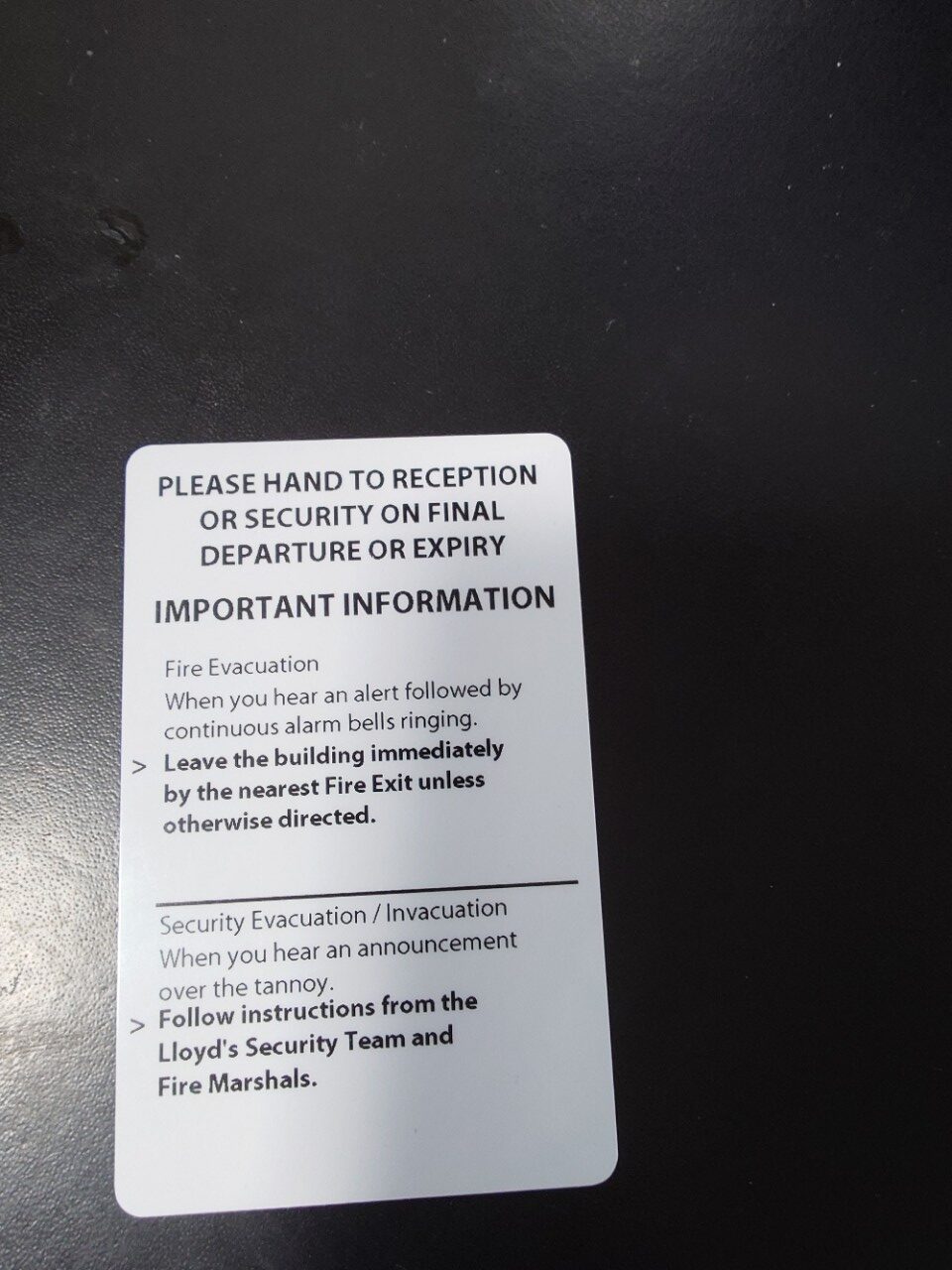

ロイズ(Lloyd‘s of London)に入るためには、連れてきてくれた紹介者は、「ロイズ・ビルへの入館証」を示す。その傍らで、同行者は「名刺」と「フォトID」(写真付きのIDカード)を示し、「日付限定の入館証」を受け取る。5年前、コロナ禍の直前にロンドンに行った際には、同じ内容を記した「紙」になっていたが、その前は、下の写真のようなプラスチック・カードであった。

この「入館証」はその裏面に「Please hand to reception or security on final departure or expiry」(最終退出時または有効期限切れの際は、受付または警備員へご返却ください)と書いてある。

いつもは「Thank you」と言いながら受付に返していた。しかし、その日は、午前中にロイズ・ビルに入り商談、それからアンダーライターとランチに出かけた。それが「長いランチ」となり「ディナーまでとなった日」であった。このため返却できず今も手元にある。

日付が2015年6月26日、その下に筆者の名前が記されている。さらに、その下には、「COSMOS GUEST」とある。当時業務提携をしていた伊藤忠商事100%子会社の保険・再保険ブローカー、「Cosmos Risk Solutionsの紹介でロイズ・ビルに入ったこと」が記されているのである。

「UWF」(Underwriting Floor)と記されている。「ロイズ・ビルの一般見学者」は入室が許可されない、つまり「実際の保険取引が行われるアンダーライティング・ボックスがあるアンダーライティング・フロアへの入室が許可されている」という意味である。

しかし、その下に更に「This pass does not permit the holder to conduct insurance business in the room」(この許可証は、所持者が当該室内で保険業務を行うことを許可するものではありません)とある。

つまり、筆者はロイズ・ブローカーではないため、「アンダーライティング・ルーム(フロア)で、保険取引をすることを許可するものではない」と記され、「ロイズ(Lloyd’s of London)の中で保険取引ができるのは、ロイズ・ブローカーのみであること」を明確に示しているのである。

② ロイズ・ブローカー(The Lloyd’s broker)

このように、ロイズ・ビルのなかで、保険取引ができる権限を有しているのは、保険を引受けるシンジケートに所属するアンダーライターと、約400社が認定されているロイズ・ブローカー(The Lloyd’s broker)である。

したがって、ロイズ・ビルのなかで保険の商談をしようとする場合には、ロイズ・ブローカーと一緒に入館することが必須である。更に、上記Passの但し書き「アンダーライティング・ルーム(フロア)で、保険取引をすることを許可するものではない」とあるとおり、顧客が「ロイズ(Lloyd’s of London)」の中でロイズ・ブローカーも帯同せずアンダーライターと保険取引、開発等の話をすることはできないのである。

但し、2008年、前述のロイズ法が改正され、ロイズ・ブローカー以外でも、一定の要件を満たしたブローカーは取引できるようになったが、実態としては、従来とあまり変化せず、「ロイズ(Lloyd’s of London)での取引はロイズ・ブローカー」というのが業界の常識である。

しかし、これはあくまでも「ロイズ・ビルのアンダーライティング・ルームの中でのこと」であり、シンジケートがロイズ・ビルの外に有している事務所で保険取引の話をすること、それはまた、「話は別」である。

ロイズ(Lloyd’s of London)のシンジケートを所有・管理している、保険会社系を中心にしたマネージング・エージェントそしてシンジケートは、ロイズ・ビルの中に「アンダーライティング・ボックス」を有する以外、「保険会社の現地法人を有していること」も多く、「事務所で話をしよう」と言われることが多いはずである。

背景には、保険料収入のうち数%をロイズ・シンジケート全体の「安定化資金」として「セントラルファンド」に拠出することを避ける意味合いもあるが、更に重要なことは、アンダーライティング・ルーム内では、常にボックスの周りに立って順番を待つ何人ものブローカーの存在があり、「秘匿性の高い案件、大きなプロジェクトの会話をしていること」を周囲に悟らせないためである。

筆者が長年経営コンサルティングを委嘱されていた損害保険会社は、ロイズ(Lloyd’s of London)のあるシンジケートと一緒に保険商品を開発してそのシンジケートに再保険を出していた。

「損害率が抜群に良い=大いに儲かる」ためであろう、マネージング・エージェントから自社の親会社である再保険会社が設立した保険会社へ「再保険先を変更すること」を依頼されたことがある。その保険会社は、再保険のセキュリティ上も全く問題がなかったため、異論はなく再保険先を変更したことを記憶している。

1960年代、70年代は、再保険の「ロンドン・マーケット」と言えば「ロイズ(Lloyd’s of London)」を指すことが一般的であったが、以上のような理由から、また世界的規模の再保険会社がロンドンに大きな拠点を構えるようになってからは、「ロイズ(Lloyd’s of London)を含めたロンドン、シティに存在する保険会社、再保険会社の拠点」のことを指す意味合いが強くなっている。

③ ロンドン・マーケットから学ぶこと

ロイズ(Lloyd’s of London)そしてロンドン・マーケットの特徴は、「リスクをシェアすること」である。最近、日本では損害保険会社が大企業の保険取引で他の損害保険会社と「分担」(シェア)して引受けることが、なぜか問題視されたが、筆者の目にはまことに奇異に映る。

理由は、「損害保険で補償されるリスクは生命保険のそれと違い不確実性が高く、したがって不測の事態が起きる可能性が高いため、リスク・ヘッジ手段はできるだけ多く、手厚いことが重要だから」である。

前述のとおり、そのために編み出された「リスク分散の手法」が再保険である。当然、一つの損害保険会社の再保険ネットワークでリスク分散するよりも、多くの損害保険会社の再保険ネットワークでリスク分散するほうが、「リスク分散網が大きくなり、補償の安定性が高まり、惹いては損害保険会社の安定性、また保険金支払いの確実性も高く」なる。こういった点からも推し進めるべきリスク分散の手法が「リスクをシェアすること」である。

ロイズ(Lloyd’s of London)が、なぜ、数々の困難な事態を潜り抜けることができて300年を超えて存在してきたか、それはひとえにこの「リスク分散」を徹底してきたからに他ならないと言えるだろう。

④ Line slip(ライン・スリップ)

ロイズ(Lloyd’s of London)、ロンドン・マーケットでおこなわれている、この「リスク分散の手法」、「リスクをシェアする方法」こそ、Line slip(ライン・スリップ)である。

「ロイズ(Lloyd’s of London)の公式WEBサイト」には、Line slip(ライン・スリップ)について、以下のように記されているので引用する。

A line slip is an agreement by which a Managing Agent delegates its authority to enter into contracts of insurance to be underwritten by the members of a syndicate managed by it to another Managing Agent or authorised insurance company in respect of business introduced by a Lloyd’s Broker named in the agreement.

Managing Agents do not need approval from Lloyd’s to operate under a line slip.

Once the Managing Agent or insurance company acting as the line slip lead underwriter has entered into a contract of insurance with the insured, the evidence of insurance will normally be issued by means of a MRC contract or via a certificate / policy. The format of the insurer authorised documentation will be determined within the line slip agreement.

(筆者訳)

ライン・スリップとは、マネージング・エージェントが、その傘下にあるシンジケートに属するメンバー(アンダーライター)が引受ける保険契約を締結する権限、それを当該契約書に指定されたロイズ・ブローカーが紹介する業務に関して、他のマネージング・エージェント、または承認を受けた保険会社に委任する合意文章のこと。

マネージング・エージェントは、ライン・スリップのもとでおこなわれる業務を執行する際にはロイズの承認を必要としません。

マネージング・エージェントまたはライン・スリップのリード・アンダーライターとして機能する保険会社が、被保険者と保険契約を締結した場合、保険の証明は通常、MRC契約書または証明書/保険証券を通じて発行されます。保険会社による承認書類の形式は、ライン・スリップ契約書内で決定されます。

まさに、「他のシンジケートや損害保険会社と『分担』(シェア)して引受けること」を示す書類が「Line slip(ライン・スリップ)」である。

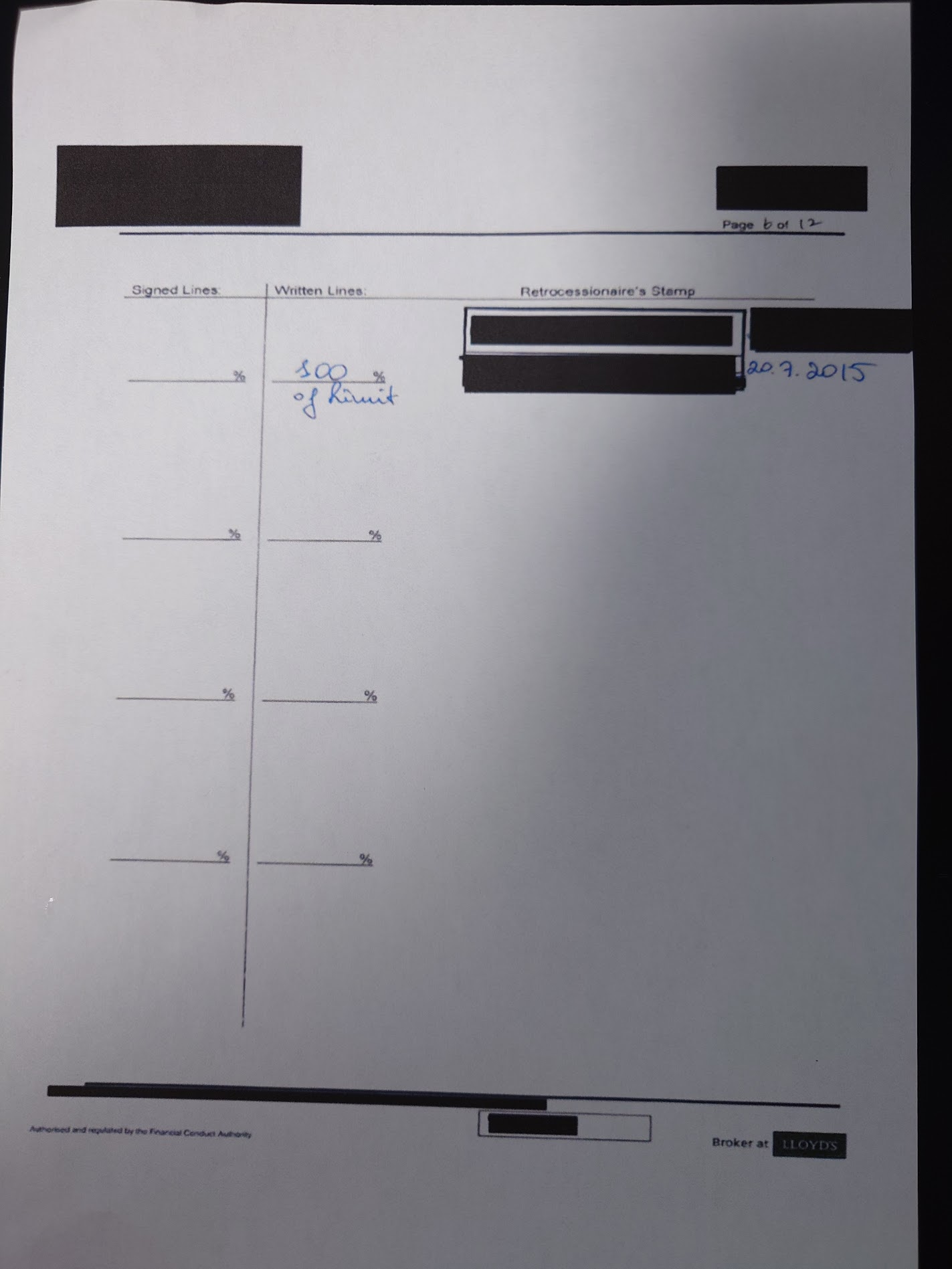

その実物は、上の写真のような形式の書類に、シンジケートもしくは保険会社のアンダーライターが、「補償対象の明細」、「約定文言」、「約款」等の各ページにサインをした書類が付帯される。この写真の事例の場合「page 6 of 12」と右上にあるように、全部で12ページの書類である。

見えにくいが、右下に「Broker at Lloyd’s」とある。The Lloyd’s broker(ロイズ・ブローカー)が「作成した書類」という意味である。

日本では、「ほとんどの保険契約には、損害保険会社の『代理店』である『保険代理店』が関与する」ため、「補償を担保する保険証券類」は、全て損害保険会社で作成されるが、ロンドン・マーケットは「ブローカー・マーケット」であるため、このようなLine slip(保険証券と同じく補償を担保する)はブローカーが作成しアンダーライターのもとに持参する。

引受の承認を得られた場合は、その証として、このようにシンジケートもしくは保険会社の「スタンプ」が押され、アンダーライターが「サイン」することによってLine slipが完成、補償が開始される。

これは、今から10年前、2015年7月20日、弊社グローバル・リンクのコンサルティングによって、ある企業がハワイに設立した「キャプティブ」からの再々保険をロンドン・マーケットにも一大拠点を持つ、世界最大級の再保険会社が引受けた際のライン・スリップである。

「実物」を確認することが重要だと考えたので、「空欄のLine slip」ではなく、あくまでも「実物」という点に拘った。「実物」を掲載するにあたっては、守秘義務の点から「既に効力は無いライン・スリップ」であるが「できるだけ古いもの」を掲載することにして、更に「黒のマスキング」を施してあることはご容赦願いたい。

この案件の規模が、その再保険会社にとっては、「一社で容易に引受けることができる規模」であったため(といっても、当時、そのキャプティブへの再保険を元受保険会社として引受けた日本のあるメガ損保では一社では引受られない規模であったが)、「Written lines: 」(保険引受額)のところには、他のロイズ・シンジケートや再保険会社の名前の記載がなく、この再保険会社のアンダーライターが手書きで「100% of Limit」、2015年7月20日を「20.7.2015」と英国式で記している。

日本の損害保険会社で「元受け」され、ハワイのキャプティブに「再保険」で出されたリスクを更にロンドン・マーケットへ「再々保険」で出したため、「Retrocessionaire‘s Stamp(再々保険スタンプ)」の個所に、この再保険会社のアンダーライターの「引受確認スタンプ」と「アンダーライターのサイン」が記されている。

この案件の場合、一社が再々保険を100%引受けたので「一枚のライン・スリップ」で事足りたが、「巨大なリスク」や「引受が困難なリスクでアンダーライターが高い割合を引受けない」、これらの場合は、多くのアンダーライターが関与するため、このライン・スリップが何枚も「再保険契約明細書:Bordereaux(ボルドロー)」に付帯される。

そうして、リスクが世界中の保険会社、再保険会社へ蜘蛛の巣のように「再保険の形」でリスク分散されていくのである、この方式が編み出され、発達してきた場所が「ロイズ(Lloyd’s of London)」なのである。

⑤ Lead Underwriter(リード・アンダーライター)

上の④Line slip(ライン・スリップ)の項で出てきた言葉に「Lead Underwriter(リード・アンダーライター)」がある。

「Lead Underwriter(リード・アンダーライター)とは、保険リスクの引受に於いて、そのリスクを最初に引受けることに同意したシンジケート、アンダーライターのこと」を言い、その選択はブローカーの腕の見せ所にもなるところである。

最初に「どのシンジケートのどのアンダーライターが、どれくらいの割合で引き受けたか」を見ることによって、次のアンダーライターは引受方針を決めていき、リスク全体が引受けられるか否かが決まると言っても過言ではないからである。

リード・アンダーライターは、「引受条件と保険料率」を決定して、他のシンジケートや保険会社がその保険の引受集団に入ってくるか否かの基準を決める重要な立場であり、「他の損害保険会社と『分担』(シェア)して引受ける」際の中心者となるアンダーライターである。

Lead Underwriter(リード・アンダーライター)が、その保険の分野で、「名前の知れた実績のあるアンダーライターであり、しかも高い割合で引き受けをしている場合」には、フォロー・アンダーライター(この案件をシェアして引受けるアンダーライター)は容易に集まる。

一方、それが「名前の知れた実績のあるアンダーライター」であっても、「低い割合の『引受』であった場合」や、「実績の乏しいシンジケートや名前が知られていないアンダーライター」がLead(リード)した場合には、「アンサポート(Unsupport)」、つまり「リスクが100%が引受けられず、引受不可」となることが多い。

このように、リード・アンダーライターは、保険契約の価格設定、条件の交渉、および他の引受会社(「フォロー市場」)を呼び込む上で中心的な役割を果たすため、ブローカーが、「誰をリード・アンダーライターにするか」を的確に把握しているか否かが重要であり、こういった点から、「The Lloyd’s broker(ロイズ・ブローカー)の選択」が非常に重要なのである。

「この保険分野はこのロイズ・ブローカーが良く知っていて強い、この保険分野はあのロイズ・ブローカー」と、弊社グローバル・リンクでも、保険の種類、必要な補償額等によって、業務提携しているブローカーのみならず、ロンドンで知り合った多くのブローカーのサポートも得ている。

「巨大なブローカーであれば大丈夫では?」という疑問が涌くかもしれないが、「そうとは言えない」のが実情である。「アンダーライターの好み」という点もよく考慮しなければいけないからである。

少なくとも、筆者が知っている約50人ほどのアンダーライター、そのほとんどは、巨大なブローカーより、専門的な知識を豊富に有する小さなブローカーを好んでいたことを憶えている。

「大きいブローカーは、専門的な会話より、ボリュームで引き受けさせようとする傾向が強いから好きではない」と、ある友人のアンダーライターはその意味を正直に語っていた。

だから、グローバル・リンクも、専門的な知見を有する小規模なロイズ・ブローカー数社と業務提携をしている。「あのアンダーライターは、小さいけどあのブローカーと長年の付き合いがあり仲が良い」、実はこんなところからも「良い条件は出てくる」からである。

無論、「グローバル・リンク自身が、長年かけて築いてきた、キャプティブからの地震保険やサイバー保険などの再保険を引き受けてくれる、世界最大級の再保険会社の各部門のアンダーライター達、またロイズのそれらの分野を得意とするシンジケートの多くのアンダーライター達との信頼関係」という背景があるからできることであろう、そう手前味噌ながら思うほど、ロンドン・マーケットでの重要なキーワードは、「信頼関係」である。

アンダーライティングは「信頼という言葉が最も重要な、非常に人間臭い世界」なのである。

⑥ Face to Face(フェース・ツー・フェイス)

こういった点からも、ロンドン・マーケットで最も重要な言葉は「Face to Face」であると言える。直接会って、対面でのコミュニケーションを取ることである。

その理由は、「アンダーライティング」は、「目の前に置かれた申込用紙」を「どんな会社のどんな人が、どんな状態で、持参してきたか」というファクターによって、その信頼性や、それによる将来の不確実なリスクが変動するものだからである。「信頼の置けるコミュニケーションが成されたか否かが最も重要な世界」、それが「ロンドン・マーケットでの保険取引」である。

筆者は、今から40年前、1985年、当時勤務していた大手外資系損害保険会社で、米国ニューヨーク本社に研修に行き、1ヵ月後「引受権限(Authority)」を委ねられた。それ以前は、ニューヨーク本社のアンダーライターに全件照会して、引受可否、そして保険料率を決めてもらっていたが、「引受権限の委譲」以降、引受権限を委ねられた150万ドルまでは、「誰に尋ねることなく自分が決めることができる権限」であった。

権限委譲後、わずか1万ドル程の案件が目の前にもたらされたが、「引受可否を決めるのにかなり長い時間思案したこと」をいまだに憶えている。「リスクが怖かった」のである、「事故が起きること」が。

「アンダーライターのその怖さを払拭してあげる作業、それこそが直接会って、話をすること」である。

幸いにも多くの案件を引受けたが、事故は1件も起きることはなかった。しかし、その「怖さ」はずっと、アンダーライターを辞めるまで続いた。「アンダーライティングは、ヒマラヤの険しい切り立った稜線を歩いていくような仕事」と、昔一緒に働いてくれていたスタッフには「怖さを持つ重要性」をよく語ったものである。

損害保険会社の経営コンサルティングを委嘱されていた時、ロイズ(Lloyd’s of London)のあるシンジケートのActive underwriter(アクティブ・アンダーライター:主席保険引受人)とロイズ・ブローカーのCEOを日本に呼んで、営業を担ってくれていた大手財閥系生命保険会社の法人営業部門の全スタッフに対して、「ロイズ・セミナー」と銘打ったセミナーを開いたことがある。そのとき、アクティブ・アンダーライターの言ったことがいまだに耳朶に残っている。

彼は、「アンダーライティングは、ボックスに来た、目の前のトニー(ロイズ・ブローカーのCEO)を見て、『今日は奥さんと喧嘩はしていないかな』とまず観察するところから始まる」と、皆の笑いを誘いながら、しかも、「アンダーライティングの核」を見事に語ったのである。

「『目の前にある紙に書かれたデータ』だけで的確なアンダーライティングができるか」と問われたら、答えは「No」と、元アンダーライターの筆者としては答えるだろう。「紙に書いてあることを補完する事項、事象の方が重要なことが多いのが普通だから」である。目の前にいるブローカーが「言わなければいけないことを言わないようにしているのか」、「何かを隠しているのか」、それとも「紙にはこう書いてあるが、こういう事実も事象もある」と言ってくれるかどうか、それによって的確なアンダーライティングができるかどうかが決まる。だから、「Face to Face」が重要なのである。

「なぜ、10数年も2ケ月に1回もの頻度でロンドンに出張した」のか、その答えはこの「Face to Face」を実現するためであった。出張日のタイミングによっては、「See you next month(来月また会おう)」という出張も2度や3度ではなかった。

そのために「海外出張など無いに等しい生命保険会社の経理部門を相手」に、今は同僚となった菅原執行役員が、毎年その予算取りにどれほど苦労したかと感謝している。

その結果、ロイズ(Lloyd’s of London)のアンダーライター諸氏からは「羽谷はロンドンに通勤しているみたいだな」とさえ言わしめることができ、惹いては、それが「最高水準の再保険カバーを得る=比類なき競合優位性を持つ保険商品の開発と販売」を可能にした。

親会社は巨大な生命保険会社でありながらも損害保険会社の方は、同じ旧財閥グループ内の競合損保と比べて、「象と蟻」であったが、「その蟻が、多くの案件で、象を倒し、日本のその保険の市場全体の10%超の占有率を得ることができた、その核が『Face to Face(フェース・ツー・フェイス)』」なのである。

12.終わりに

この小論考を書くにあたって、「Face to Face(フェース・ツー・フェイス)」をどれだけ実践してきたかを確かめるため、筆者が搭乗してきたメインの航空会社のマイレージを調べてみた。

| 生涯マイル |

855,606マイル (国内線 65,818 マイル 国際線 789,788 マイル) |

| 生涯搭乗回数 |

250回 (国内線 117 回 国際線 133 回) |

この生涯マイルは、地球約 34.4周、月まで約 1.8往復、総搭乗時間は約 2281.6時間に相当します。

こう記されていた。

但し、このマイレージは「航空券を買って搭乗した回数と距離」を示しているものであり、「最高時には300万マイルを超えたマイレージを利用して何十回もロンドン他の出張に利用」した。このため、コロナ禍でロンドンに出張できなくなる直前2020年1月までの全「生涯フライト記録」を調べてみた。

ロンドンに出張した回数は、合計で75回(搭乗回数150回)、ニューヨーク、シドニー、ミュンヘン等へ出張した回数は36回(搭乗回数72回)となっていた。つまり、国際線の総搭乗回数は222回であった。

すべて「Face to Face(フェース・ツー・フェイス)」のためである。

保険ビジネス、特に再保険という「アンダーライターが直接顧客に会えない案件」の場合、アンダーライターは「その顧客の姿」そして「補償するリスク」の実像にできる限り迫りたいと思うものである、アンダーライターは「恐怖と戦いながら仕事をしているから」である。

コロナ禍のなかでも、「ロンドンに行こう」と何度も飛行機を予約した、しかし、次々に続いて出てくる「コロナの亜種ウイルスの蔓延」の状況から、スタッフまた家族から何度もその出張を止められ、ほとんどの仕事を「オンライン打ち合わせ」でおこなってきた。また、丸の内に借りているグローバル・リンクの事務所にもほとんど行くこともなく、これまたオンラインで済ますことがほとんどになった。

しかし、保険はやはり「Face to Face(フェース・ツー・フェイス)」が基本中の基本であることは、ロイズ(Lloyd’s of London)のことを本小論考にまとめながら思い出していた。ロイズ(Lloyd’s of London)に教えられた思いである。

そして、ロンドンに行くことを決めた、「メール」や「オンライン画面」だけで、長らく会えていない多くの旧友に会いに、「新たなビジネスの芽」を探しに。

この「ロイズ(Lloyd’s of London)ー キャプティブからリスクが行き着く先ー」と題した5回の連載を終えるにあたって、第1回から記し続けてきたロイズ(Lloyd’s of London)のことを改めて考えてみた。

英国は「歴史と伝統の国」と呼ばれる、ロイズ(Lloyd’s of London)も同様に「保険の歴史と伝統を体現している組織」と言えるだろう。

「歴史と伝統」と言うと何か古臭いものを想像しがちだが、ロイズ(Lloyd’s of London)が「常に状況に対応して変化しながら進化してきた」ことは、「『迅速な情報の入手が事業の進展のカギを握る』と考えてロンドン中央郵便局のすぐ隣に事務所を移転する」、「『リスクの分散が事業の安定性のカギを握る』と考えてLine slip(ライン・スリップ)を生み出す」等々、リスク・マネジメントの本義である「外的要因、内的要因を分析して対応してきた姿」で、明確にそれを示している。

だからこそ、本コラムに記した事柄も明日には大幅に変化している可能性もある。常に「進化」を考えている組織なのである。

「種の起源」(「進化論」)で有名なチャールズ・ダーウィンは、「この世に生き残る生物は、最も強いものではなく、最も知性の高いものでもなく、最も変化に対応できるものである」という考えを示したと言われている。

しかし、実のところ、「種の起源」にこの言葉はなく、「後世の創作」と言われているが、事業経営においてこれほど重要な言葉はないであろう。これを体現しているからこそ、ロイズ(Lloyd’s of London)は300年を超えて「損害保険の頂点」に立ち続けている。

これこそ、我々がロイズ(Lloyd’s of London)から学ぶべきことではないだろうか。

執筆・翻訳者:羽谷 信一郎

あとがき

1.長年、ロンドン・マーケットに通い詰め、ロイズ(Lloyd’s of London)については、シンジケートのアンダーライター達、ロイズ・ブローカー達から多くのことを学ぶことができました。また、「ロイズ(Lloyd’s of London)」全体の運営管理をおこなう組織である「Corporation of Lloyd’s」についても、同社の多くの方々と知り合う機会がありました。

その中心、「世界戦略を統括する取締役」であった、Jose Ribeiro(ホセ(英国人は、ジョセと発音)・リベイロ)」と初めて会ったのは、彼がロイズ(Corporation of Lloyd’s)に入社してすぐの2007年。それ以来、私のコンサルティング先であった損害保険会社にも何度も来社して親しい友人となり、ロンドンに出張した際には必ず彼と会っていました。

そんな彼を通して色々な方々とも知り合い、様々な情報にも接していたので、幸いなことにロイズ(Lloyd’s of London)についてはかなりの知見を得ることができていました。

(2015年:Jose Ribeiroと筆者)

因みに、彼はその後、ロイズ(Corporation of Lloyd’s)を退社、保険の格付会社のA.M.Bestの役員を経て、世界的に著名なロンドンのビジネス・スクール、インペリアル・カレッジ・ビジネス・スクール(Imperial College Business School))の客員講師に就任。

「(元々が教師だったので)落ち着いたのか」と思っていたら、数年前、また金融の世界にも関与することになり(https://www.nurole.com/news-and-guides/jose-ribeiro-non-executive-director-hansard-worldwide)、「NED(Non-Executive Director:非常勤取締役)」としてですが、「非常勤」としては異例の「月5日勤務」なので、客員講師、ポルトガルにあるワイナリーの経営と合わせて、更には世界的な損害保険会社のアジア・パシフィック、ラテン・アメリカのトップも務めるようになり、非常に忙しい日々を送っているようです。

2.コロナ禍も明けたようなので、彼をはじめ多くのアンダーライターやロイズ・ブローカーの友人たちに会いたいなと思っていたところ、先月、8月はじめ弊社の公式WEBサイトに、「ロイズのことを色々と調べていたのですが、よく解らなくて困っていたところ、貴社のホームページのコラム記事を見て・・」というお問い合わせがあり、このことがきっかけとなり、本小論考の執筆を決めた次第です。

「お問い合わせに、正しく、適切にお答えするために」と、改めて色々と調べてみましたが、ロイズに関する本は少なく、かつどれも40年程前に出版されたものばかりでした。

当時は正しかったのでしょうが、状況が大きく変化しており、「富裕層がアンダーライターをしている・・」と、現況とは全く異なっている記述も多く、またネット情報を調べてみても古いものばかり、新しいものでも2019年のロイズの組織変更以前のものしか見つけることができず、私が知る現状とは大きな乖離が感じられました。

また、「実際にロイズ(Lloyd’s of London)のシンジケートとビジネスをおこなってきた視点では書かれていないため、実像になかなか迫れないのでは・・・」とも感じ、「ロイズ(Lloyd’s of London)との実務経験者の視点で整理しておきたい」と思い立ちましたが、書き上げてみたら、「短く」と思って始めたにもかかわらず「5回連載の分量」となってしまいました。これも、長年、ロイズ(Lloyd’s of London)にお世話になってきた身として、ロイズ(Lloyd’s of London)のことを正しく理解していただく一助になればと思った次第であり、ご容赦頂きたいと思っております。

English Translation

Copyright © Shinichiro Hatani 2025 All rights reserved

Unauthorised reproduction, quotation or duplication of the contents within this column is strictly prohibited.

Captive(CA)79 Lloyd’s of London Series (All 5 instalments published together) – Where risk ultimately ends up from captives–

Regarding Lloyd’s of London, this series commenced on 29 August as “CA74 Lloyd’s of London – Part 1‘. Although its name is well known, its content is a highly specialised field that is not widely understood, even among employees of non-life insurance companies, except for those directly involved.

Despite being ’a highly specialised field, well-known by name yet little understood even by employees of non-life insurance companies outside the immediate circle ‘, we are grateful that a surprisingly large number of readers have viewed it and that we have received a considerable number of comments such as ’I now understand Lloyd’s much better than before”.

Simultaneously, many readers requested that we post all five instalments together for easy reference going forward. Therefore, to enable seamless reading, we have decided to republish all five instalments collectively below. Please note that combining five instalments of the column into one has resulted in a rather lengthy piece, but I would be most grateful if you would read it through to the end.

I was commissioned by a major zaibatsu-affiliated life insurance company to provide management consultancy for its newly established non-life insurance subsidiary and its operations, founded in 1997. For thirteen years, I travelled to the London insurance market (the London Market), centred on Lloyd’s of London, once every two months. Even after commencing captive operations, I continued to travel to London several times a year. Drawing upon the insights gained from this experience, I shall now outline the following points concerning Lloyd’s of London, an organisation not widely understood in Japan.

Contents

1. Introduction

2. The Emergence of Non-Life Insurance

3. The Birth of Lloyd’s of London

4. The Formative Years of Lloyd’s of London

5. The Development of Lloyd’s of London

6. Admiral Nelson

7. Lloyd’s of London Today

① The Market

② The Underwriting Rooms within the Lloyd’s Building

③ The Marine Floor

④ The Non-Marine Floor

⑤ The Reinsurance Market

⑥ Underwriters (Holders of Underwriting Authority)

8. Entities and Parties Involved with Lloyd’s of London

9. The Meaning Represented by Lloyd’s of London

10.The Mechanism and Structure of Lloyd’s of London

11. Transactions in the Lloyd’s Market

① Access to the Lloyd’s Building

② Lloyd’s broker

③Lessons from the London Market

④ Line slip

⑤ Lead Underwriter

⑥ Face to Face

12. Conclusion

1. Introduction

Following the Second World War, it is no exaggeration to state that the centre of the global economy shifted entirely from Europe, centred on Britain, to the United States, with the world’s economic activity now conducted around the US. However, this ‘one exception’ lies within the field of non-life insurance.

Unlike the life insurance sector, where one might say ‘the occurrence of unforeseen losses is scarcely conceivable’, the non-life insurance sector frequently underwrites enormous risks that threaten the very survival of insurance companies.‘Arranging reinsurance’ has become the paramount strategic imperative for these firms. Crucially, the venue for this reinsurance arrangement is not the United States, but the City of London – the financial district centred around Lloyd’s of London.

Insurance brokers, who facilitate insurance and reinsurance transactions between insurers worldwide and their clients, maintain numerous offices and business premises here.Conducting insurance and reinsurance transactions day and night, London is the global centre for insurance and reinsurance. It is referred to as the ‘London Market’, denoting the place for arranging property and casualty insurance, particularly reinsurance.

2. The Origins of Non-Life Insurance

Various theories exist regarding the birthplace of non-life insurance, including the Middle East and Greece. All theories agree that it originated as a means of risk hedging (mitigation) for cargo suffering damage during maritime transport for foreign trade. It is considered that forms similar to modern marine insurance represent the origins of non-life insurance.

This ‘marine insurance’ is said to have been largely perfected in 14th-century Italy, though its origins are traced to the ‘Bottomry’ used in Mediterranean trade, centred on Italy, during the 12th and 13th centuries.

However, these ‘Bottomry’ differed somewhat from the structure of modern marine insurance. In marine insurance, a merchant wishing to trade pays a premium to an insurer and, in the event of cargo loss, receives compensation for the loss amount from the insurer.

Bottomry, on the other hand, began with a merchant who wished to purchase goods, charter a ship, and engage in trade by asking for the necessary capital from a financier. If the voyage concluded safely, the merchant would repay the financier the principal sum plus interest. However, if the cargo was completely lost due to an accident or pirates, the merchant was exempted from repaying the loan to the financier.

In this sense, capitalists providing funds through Bottomry can be considered closer to modern venture capitalists than to insurance companies.

Consequently, the interest paid to the capitalists upon a successful voyage was exceptionally high, typically ranging from 20% to 30% per voyage. This also serves as evidence of how Mediterranean trade at the time was a venture characterised by high risk, yet offering the potential for immense wealth upon success.

Thus, Bottomry fulfilled two functions: ‘funding’ and ‘risk-bearing’. According to ‘The Theory and Practice of Marine Insurance’ (edited by Eiichi Kimura, published by Kōbundō), around 1230, Pope Gregory IX issued the Interdictum Usum Dignorum (the prohibition of usury), declaring that ‘receiving high interest through lending and borrowing contravenes the Christian teaching of charity towards one’s neighbour.’ This led to the prohibition of Bottomry.

However, as long as trade continued, financing and risk-sharing remained essential. Consequently, various methods were devised to circumvent the prohibition. By completely separating financing from risk-sharing, the prototype of modern marine insurance emerged in Italy around the 14th century, extracting solely the risk-sharing function from Bottomry, as described earlier.

The sophistication of the marine insurance clauses of that era was such that their essence is still largely preserved today in the Institute Cargo Clauses (ICC) used in international trade by the Institute of London Underwriters. This also suggests they contributed significantly to the stable operation of insurance companies.

3. The Birth of Lloyd’s of London

Whenever I travel to London on business, I stay at a hotel I have favoured for many years. It faces Hyde Park, a location perfectly suited to my hobby of jogging, and sits directly above Lancaster Gate Underground Station.

Each morning, I take the Central Line underground towards the City, heading for Bank Station. Upon arrival and emerging above ground, two roads lie before me, both leading to the City and its very heart, Lloyd’s of London. One is Cornhill, the other Lombard Street.

Lombard Street retains this name because it was a parcel of land granted by King Edward I (1272–1307) to immigrants from the Lombardy region of northern Italy. Many of these immigrants were goldsmiths, but financial and insurance systems, too, were introduced to England from Italy, then the most advanced nation.

(The site of the second Lloyd’s of London Coffee House at 16 Lombard Street)

This Lombard Street ends after about 400 metres where it meets Gracechurch Street; across the road, the street name changes to Fenchurch Street.

As will be mentioned later, midway along Lombard Street is the “blue plaque” (a type of historical information plaque installed throughout the UK) shown in the above photograph. This plaque marks the location where Lloyd’s Coffee House (now Lloyd’s of London) stood from 1691 to 1785.

This area served as the financial heart of London, England, and until the 1980s, the head offices of most banks headquartered in the UK were located on Lombard Street.

The name “Lloyd’s of London” first appeared in literature in an advertisement section of the Gazette newspaper, published in February 1688.This marked the first historical appearance of the name “Lloyd’s of London” as an insurer.

Thus, the then cutting-edge business model combining “finance” and “insurance” matured and developed centred on the City of London and Lombard Street. To this day, London maintains its status as the “world’s centre for non-life insurance”.

4. The Formative Years of Lloyd’s of London

Today, the Lloyd’s of London building stands just a few minutes’ walk from Bank station.

The Lloyd’s of London building, commonly known as One Lime Street. At its main entrance stands a large automatic revolving door – the kind that stops immediately if touched even slightly. Beside it, two staff members, also serving as security, keep a constant watch to prevent any unforeseen incidents.

In the late 1600s, Edward Lloyd opened a coffee house on Tower Street, beside Tower Bridge – then a popular social and commercial hub – which became a staple of London tourism. The establishment was named after him: Edward Lloyd’s Coffee House. This was the origin of Lloyd’s (Lloyd’s of London).

London is situated along the Thames estuary, where the river flows into the Atlantic. Consequently, many shipping merchants gathered at the coffee house, which became renowned for publishing maritime news. Where shipping merchants and cargo owners congregated, the central topic of discussion naturally became ‘how to manage maritime transport risks,’ leading to the organic emergence of merchants who undertook insurance.

Within the coffee house, boards displaying details such as ‘ship name, ship history, cargo, captain, voyage schedule, and so forth’ were displayed for underwriting consideration. Beneath these, the “underwriters” would note their share of the underwriting and sign their names. This tradition is still carried on today in the practice of signing at the bottom of an insurance policy. It is said that this is why the person underwriting the insurance came to be called an ‘underwriter’.

At that time, insurance companies did not exist; merchants underwrote insurance, and their employees circulated among other merchants to jointly underwrite policies. As the insurance business grew, individuals who had originally been employees of companies run by underwriters became independent. They began acting as intermediaries between underwriters and those wishing to take out insurance, establishing the “insurance brokerage” business. These individuals came to be known as “brokers”.Within the shop, an ‘insurance market’ emerged where these brokers collaborated.

A group formed comprising these wealthy individuals who undertook insurance, and over time, this collective underwriting organisation came to be known as a ‘syndicate’.Furthermore, brokers began facilitating arrangements where underwriting organisations would pool risks by underwriting jointly with other syndicates through broker intermediation. This practice – where underwriting organisations, through broker intermediation, underwrite jointly with other syndicates to spread risk – represents the origin of the modern Lloyd’s of London.

5. The Development of Lloyd’s of London

(Plaque: “The Old Post Office” 1678–1829)

As the scale of business grew, Lloyd’s Coffee House became too cramped. In 1691, Lloyd’s of London relocated to 16 Lombard Street, a corner of the City of London – then, as now, the heart of the business district – where the aforementioned “blue plaque” is located.

The reason for this move was that in 1678, the General Post Office was built immediately adjacent to this location. It was the spot closest to this “hub” where information from around the world converged via the postal system. Unlike today’s fully developed postal delivery systems, the quickest way to receive mail in the 17th century was to open a private letterbox installed within the post office.

Lloyd’s of London was the global institution that recognised the strategic importance of this postal system early on and reaped its benefits.

If asked, ‘Why did Lloyd’s of London, which was once merely an insurance broker, become the world’s largest insurance market today?’, one would answer: ‘Because it accurately understood, from a corporate strategy perspective, how crucial communication methods were to its own business, and formulated and executed that strategy.’

Following its relocation to the building of the “Second Lloyd’s Coffee House”, Lloyd’s of London gained the ability to obtain overseas information more swiftly than any competitor. By the 18th century, it had grown substantially as an insurer specialising exclusively in marine insurance. During the American War of Independence in the 1770s, it demonstrated the critical importance of marine insurance. As the largest provider, Lloyd’s of London evolved into a global dominator of marine insurance.

Had it not relocated near the General Post Office, this would not have occurred.Lloyd’s of London recognised the importance of rapid information transmission and grew into a global insurance institution.

6. Admiral Nelson

The armies of Emperor Napoleon, who had swept across the European continent, organised a massive invasion force to land in Britain. On 21 October 1805, they clashed fiercely with the British fleet off Trafalgar, Spain.This was the Battle of Trafalgar. Under the brilliant command of Admiral Nelson, who continued directing operations despite being struck down by a sniper’s bullet, the British forces achieved a decisive victory. Trafalgar Square, built in central London, commemorates this triumph.

The photograph below shows part of the Admiral Nelson Corner, located on the ground of the Lloyd’s Building – the headquarters of Lloyd’s of London, which has deep ties to the sea through marine insurance – displaying Admiral Nelson’s personal effects and memorabilia. ‘Nelson Corner’, which displays Admiral Nelson’s personal effects and memorabilia.

7. Lloyd’s of London Today

The most quintessentially British culinary tradition is arguably the ‘Pub’. It is almost certain that every town and village across Britain has a pub. In a sense, one might describe it as ‘a place like a café where you can have a drink’; however, as the nuance differs considerably when translated into Japanese terms such as ‘sakaba’ or ‘izakaya’, it is often referred to simply as a ‘pub’ in Japan as well.

In the past,Lloyd’s Coffee House served this purpose. However, the initial discussions of deals with Lloyd’s of London and reinsurance underwriters rarely take place within the Lloyd’s Building or their offices near Lloyd’s of London. Instead, they almost invariably occur in a pub – a well-established practice within London’s insurance industry.

The reason for discussing matters over drinks is that it better reveals both the “broker’s true nature” and the “real substance of the deal” – a form of risk management for the underwriters themselves.

From 10am, when “Lloyd’s of London opens”, pubs across the City simultaneously become “insurance markets”.

Traditionally, pubs not only offered affordable lodging but also provided relay horses for travellers, hence the adjoining stables. Today, City pubs serve as the ‘insurance market,’ where numerous underwriters and brokers, tipping pint glasses, discuss deals and assess ‘insurability.’ The pub is that ‘initial venue.’

(Current Lloyd’s Building)

① Market

A market is a place where goods are bought and sold. Tsukiji Market relocated to Toyosu, becoming Toyosu Market, where seafood and produce are traded. The term “market” referring to the buying and selling of insurance primarily denotes Lloyd’s of London. However, because thousands of insurance companies and insurance brokers (insurance intermediaries) from around the world have offices centred on Lloyd’s, the entire “Insurance Block” within the City (London’s financial district) is also called the “market”. This is the so-called “London Market”.

(The Underwriting Room within the Lloyd’s Building)

Insurance brokers act as intermediaries in the buying and selling of insurance. Lloyd’s of London, often described as “a market within the insurance market”, has its trading venue (the Underwriting Room) as shown in the photograph above.

Companies wishing to underwrite insurance at Lloyd’s of London – many of which are non-life insurance companies – seeking to form a syndicate, the organisational body to which the underwriters belong, must first establish a company to operate and manage the syndicate. This company requires approval from Corporation of Lloyd’s (commonly known as the Lloyd’s Corporation: the managing company overseeing the entire Lloyd’s of London). the company managing and operating the entire Lloyd’s of London) must first establish a company to manage and operate the syndicate. This company is called a “Managing Agent” (syndicate holding and management company). It employs underwriters, clerical staff, and others to enable the underwriting of insurance.

A Managing Agent may hold several syndicates under its umbrella, or it may hold only one syndicate.

(Inside the Lloyd’s of London Building, looking from the first floor (second floor in US/Japanese style) to the ground floor (first floor in US/Japanese style) Marine Underwriting Floor)

② Marine Floor

The Ground Floor is occupied by Marine underwriters’ syndicates. The organisational body to which underwriters belonging to the syndicate belong is the “syndicate”. It is acceptable to think of a “syndicate = the company underwriting the insurance = the insurance company”, but as mentioned earlier, it is not the insurance company itself. Rather, it is the organisational body established by insurance companies and others when underwriting insurance within Lloyd’s of London.

③ Routine Bell

A term indispensable when explaining Lloyd’s is the “Routine Bell”. It is located on the Ground floor (Marine floor) of the Lloyd’s Building. It is “the bell symbolising Lloyd’s of London”, rung once for bad news and twice for good news.

In the Battle of Trafalgar in 1805, the British fleet under Admiral Nelson defeated Napoleon’s French forces. They captured the French frigate La Lutine, renamed it HMS Lutine, and incorporated it into the Royal Navy. Twenty-five years later, this ship sank.

At that time, the insurer of the vessel and its cargo was, naturally, Lloyd’s of London. The insurance payout is said to have been one million pounds sterling. This equates to approximately £80 million in today’s value, exceeding ¥10 billion when converted to yen.

Lloyd’s of London made every effort to recover the vessel but failed. It was not until 80 years later, in 1859, that they finally succeeded. Among the salvaged items from the wreck,the ship’s bell was deemed the “most important item”. It was brought to Lloyd’s of London and has since remained, as a symbol of the organisation, centrally positioned in the Underwriting Room of the Lloyd’s Building.

(The Routine Bell, located on the ground floor of the Lloyd’s Building)

④ Non-Marine Floor

On the First Floor (UK level 1, Japanese level 2), underwriters from Non-Marine syndicates (covering all classes of insurance other than marine) have their “shops”.

The Second Floor (UK level 2, Japanese level 3) is called the Company Market, where insurance company underwriters are located.

Some thirty years ago, while employed by CIGNA Corporation (headquartered in Philadelphia, USA) at the time considered the world’s largest, I was sent on a three-month OJT training assignment to London. During that time, I worked as an underwriter on this Second Floor from 10:00 to 16:00. Before and after these hours, I carried out my work and post-work summaries at CIGNA’s building near Lloyd’s of London.

The syndicate’s “shop” within Lloyd’s of London is termed a Box. Underwriters stationed in the Box all day sit in chairs with backrests. As seen in the photograph above, the chairs without backrests along the aisle are occupied by the underwriter and the broker who has come to negotiate the acceptance or refusal of the risk.

I hear the reason for the lack of backrests stems from an unwritten rule at Lloyd’s of London: ‘Do not monopolise an underwriter for extended periods.’

As proof, if an inexperienced broker is found talking to an underwriter for over 15 minutes within Lloyd’s of London, they may be politely, or sometimes directly, asked to leave.

⑤ Reinsurance Market

Reinsurance refers to the act of an insurance company (or similar insurance institution) insuring the risk it has underwritten with another insurance company (or similar insurance institution) to transfer that risk. It is called “reinsurance” because it involves insuring the underwritten insurance “again”.

As noted at the outset, since the Second World War, all industries except non-life insurance have shifted from Europe, centred on Britain, to the United States, and the global economy now revolves around the US. However, insurance, particularly non-life insurance, is entirely different. The global centre for non-life insurance remains London.

In the life insurance sector, where underwriting is based on calculations by actuaries, “unforeseen losses” rarely occur. Consequently, reinsurance is not common in life insurance. In contrast, the non-life insurance sector underwrites massive risks that can threaten a company’s very survival. Therefore, “arranging reinsurance” is a paramount strategic priority. The global centre for reinsurance arrangements is the City of London; the financial district centred around the aforementioned Lloyd’s of London.

When an insured party purchases insurance from an insurer, the “transferred risk” is then transferred to the reinsurance market, composed of reinsurance companies, for further risk transfer (risk hedging). This movement and flow spreads out in multiple directions, much like a spider’s web. Consequently, the transfer of risk from the primary insurer to the reinsurance market is often referred to not as risk transfer, but as risk diversification.

The primary insurer, having underwritten the insurance policy from the policyholder, typically places reinsurance with specialist reinsurance companies. However, it is not only specialist reinsurance companies that conduct reinsurance business. It is also common for primary insurer groups, possessing reinsurance underwriting divisions (subsidiaries), to underwrite reinsurance themselves.

Consequently, the reinsurance market is a marketplace where numerous insurance companies (insurance institutions), not just specialised reinsurers, conduct transactions. Therefore, for insurance professionals worldwide, whether they are reinsurers or primary insurers, transactions in the location where the largest concentration of players willing to accept reinsurance is found globally are preferred, as they enable business to be conducted efficiently. That location, the global reinsurance market, is London.

⑥ Underwriter (holder of underwriting authority)

If an underwriter moves to another syndicate (another insurance company), it is very common for their clients to transfer to that syndicate as well. This illustrates how deep the relationship between underwriters and their clients (policyholders) can be.

8. Entities and stakeholders involved with Lloyd’s of London

The official Lloyd’s of London website categorises those conducting business related to Lloyd’s of London as follows:

The policyholder:

They could be businesses, organisations, other insurers and individuals from around the world looking to mitigate the impact of potential risks. And it’s not only the everyday risks they’re looking to cover. But also, complex and unique ones, like protecting a business from cybercrime or insuring first-of-its-kind technology.

The local broker (in the policyholder’s country):

They are the first point of contact for a policyholder. They operate within the local market where the policyholder is based. They will assess the policyholder’s needs and determine whether it is more suitable for the Lloyd’s of London marketplace.

The Lloyd’s broker:

They work on the policyholder’s behalf, negotiating with underwriters to create a tailored policy to insure the risk.

This section lists Marnix Europe Limited, a subsidiary of Marnix (Europe), a wholly-owned subsidiary of major general trading company Marubeni, as one of approximately 400 Lloyd’s brokers (as of end-2024) with whom our Global Link has a business partnership, as follows:

Marnix Europe Limited

River Plate House, 7-11 Finsbury Circus London United Kingdom EC2M 7AF

Tel: +44 (0)20 7826 8693 Fax: +44 (0)20 7826 8695

The underwriter:

They work with other specialist underwriters and the Lloyd’s of London broker to draw up the policy. Each underwriter will decide on the price and terms they’re willing to take.

Active Underwriter:

The individual at the underwriting box with principal authority to accept insurance and reinsurance risk on behalf of the members of a syndicate.

The syndicate:

They are made up of underwriters who group together to form a syndicate to write insurance at Lloyd’s of London. Underwriters enter into insurance contracts on behalf of Lloyd’s syndicates. Each syndicate is given a number by Lloyd’s to identify them.

Lloyd’s of London had over 80 syndicates in existence at the end of 2024.

The managing agent:

They are a company established to manage one or more syndicates. Managing agents are responsible for employing the underwriters.

As of the end of 2024, there are approximately 50 managing agents.

Among these “players”, Lloyd’s of London is the “insurance exchange” where the Lloyd’s broker and the underwriter conduct insurance transactions.

Consequently, if you ask a Lloyd’s underwriter or Lloyd’s broker, ‘What is Lloyd’s?’, they will all answer ‘The Market’ – that place is Lloyd’s of London.

9. The Meaning Represented by Lloyd’s of London

As the word Lloyd is a surname, there are indeed numerous companies bearing the name Lloyd, chief among them being the Lloyd’s Banking Group plc, the fourth largest banking group in the UK.Consequently, to distinguish it from these, the insurance institution and market known as Lloyd’s of London is referred to as Lloyd’s of London within the insurance industry.

The term ‘Lloyd’s of London’ carries the following two meanings:

• “Lloyd’s as the international insurance market”: The insurance market located in the City of London, UK, known as “Lloyd’s Market”.

• “Lloyd’s as the corporate body”: The Lloyd’s Insurance Association (*Not the official name, but a translation of the Japanese into English), a body incorporated by an Act of the British Parliament, whose members are brokers and syndicates. It is called the “Corporation of Lloyd’s” (also commonly known as Lloyd’s Corporation).

This Lloyd’s of London Insurance Association is a self-governing organisation whose members are brokers and underwriters. However, the Lloyd’s of London Insurance Association itself does not underwrite insurance; instead, syndicates (underwriters) underwrite the insurance. Corporation of Lloyd’s exists to own the Lloyd’s Building and provide its members with the trading venue (the Underwriting Room) and administrative services related to the underwriting business.

Traditionally, insurance underwriting was conducted by wealthy individuals (Names) bearing unlimited liability, with no cap on insurance payouts. However, the onset of significant asbestos-related insurance claims in the early 1990s led to the bankruptcy of many Names, causing their numbers to decline rapidly. Today, they provide only around 1-2% of the underwriting volume.

In their place, many large corporations, permitted to enter the market through the limited liability corporate membership system introduced in 1994, established managing agents and formed numerous syndicates. They now account for the vast majority of Lloyd’s of London underwriting.

10. The Mechanism and Structure of Lloyd’s of London

Mechanism

Lloyd’s of London is often introduced as ‘the British insurance company Lloyd’s’, but as repeatedly stated in this brief essay, ‘Lloyd’s of London is not an insurance company but an insurance market’.

One might grasp the mechanism of Lloyd’s of London by considering the Toyosu Market, which relocated from Tsukiji in 2018.

The Toyosu Market, a vital hub distributing seafood and produce from around the world, comprises the “Wholesale Market” where transactions for seafood and produce from domestic and international sources, such as tuna auctions, take place, and the “Middle Wholesale Market” where shops of middle wholesalers, who purchase seafood and produce from wholesalers and sell them to restaurants and retailers, are concentrated.

Conversely, Lloyd’s of London, as an insurance market, can be described as a venue for the “buying and selling of risk”. It is a place where “those wishing to sell their risk (i.e., seeking buyers)” conduct “individual auctions” with underwriters, facilitated by Lloyd’s brokers, to buy and sell coverage.

The mechanism of consolidating Toyosu Market’s “wholesale market” and “intermediate wholesale market” into a single location, the exchange known as the “underwriting room”, is precisely what constitutes Lloyd’s of London.

Lloyd’s of London, often translated into Japanese as “ロイズ保険組合(Lloyd’s Insurance Association (*Not the official name, but a translation of the Japanese into English))”.

On Lloyd’s official website, it is stated that there exists an organisation responsible for the overall operational management of Lloyd’s of London, described as ‘an independent organisation and regulatory authority that acts to protect and maintain the market’s reputation, providing services and unique research, reports, and analysis to the industry’s knowledge base.’

This is the organisation prominently introduced on Lloyd’s official website as ‘Lloyd’s Corporation’. However, at the bottom of that page, it states: ‘Lloyd’s of London Copyright 2025 Lloyd’s and Corporation of Lloyd’s are registered trademarks of the Society of Lloyd’s.’

(Source: Lloyd’s of London official website)

The official name under the Lloyd’s Act is ‘Corporation of Lloyd’s’, yet for some reason ‘both names are simultaneously used by Lloyd’s of London’.

Regarding this, the author considered that ‘Lloyd’s Corporation must be the common name’, but as I could not grasp the true intent, I asked an old friend, a seasoned Lloyd’s broker with decades of experience: ‘For some reason, Lloyd’s official website introduces it as “Lloyd’s Corporation”, yet its official name under the Lloyd’s Act is ‘Corporation of Lloyd’s’. ‘Why is that?’ The response was as follows:

‘No, do not really know why the two forms of reference are used !!’Even he couldn’t understand it. Truly a baffling phenomenon.

In any case, Lloyd’s of London is functionally differentiated in terms of corporate governance into the ‘syndicate collective body’ that underwrites insurance and the organisation that manages and governs that body, the Corporation of Lloyd’s (also commonly referred to as Lloyd’s Corporation).

Structure

This “Corporation of Lloyd’s” is the legal entity that sets the rules, regulates, manages, and operates the vast “insurance market” known as Lloyd’s of London. However, it is the individual “syndicates” that underwrite the actual insurance policies. Collectively, this entire structure is referred to as “Lloyd’s of London”.

The aforementioned Lloyd’s Act 1982, an Act of the British Parliament, establishes the governance structure and rules within Lloyd’s of London.

Under this legislation, the formal name of Lloyd’s of London is defined as the “Society of Lloyd’s”. Yet, curiously, neither underwriters nor brokers one knows refer to it as such; they invariably call it “Lloyd’s of London”.

The Lloyd’s Act 1982 stipulates that the Council of Lloyd’s ‘has responsibility for the management and supervision of Lloyd’s of London as a whole’.

The Council typically comprises three Executive Members, three External Members, and nine Nominated Members. The Executive and External Members are elected from among the Members of Lloyd’s of London. The Chairman and Deputy Chairman are elected annually by the Council from among its members.

The Council of Lloyd’s determines the rules and regulations governing Lloyd’s of London as a whole, but the day-to-day governance relating to the operation of the Lloyd’s market was previously delegated, for the most part, to the Franchise Board. While materials and reports concerning Lloyd’s of London exist reflecting this approach, in 2019 this delegation was abolished. Corporate governance was consolidated within the Council of Lloyd’s, and the organisational structure was changed as follows.

(Source: Lloyd’s of London official website)

Thus, the Council of Lloyd’s, through the aforementioned organisation, sets guidelines for all syndicates operating within the Lloyd’s of London market and continuously monitors business plans and their progress to ensure appropriate underwriting and risk management. However, it does not engage in the development of individual insurance products or in underwriting activities. This is because these are areas for the syndicates to handle.

11. Trading at the Lloyd’s Market

① Access to the Lloyd’s of London Building

During my time as a management consultant, I frequently travelled to London for meetings with partner insurance brokers and reinsurance companies—first to develop insurance products, and later, after launching the captive business, to arrange reinsurance from the captive. In the section introducing the Lloyd’s building, I described its location: ‘Lloyd’s of London is situated about four- or five-minutes’ walk from Bank station.’

As mentioned earlier, this is because the hotel where the author stayed regularly during his many years of travelling to London six times a year was located directly above Lancaster Gate station on the Central Line, which stops at that station. I used the Central Line underground to travel to the City and Lloyd’s of London. This underground line first ran through central London in 1863.

Two hundred years before, in 1666, a great fire ravaged this city of London. Today, one of the underground stations serving the area known as the City – now famous as an “international financial district” alongside Wall Street in the United States – is Monument Station, served by the District Line and Central Line.

Stepping out at Monument station, one finds, true to its name, a monument standing before the station. It is the Monument to the Great Fire of London, commemorating the conflagration whose ‘fury was such it seemed to consume the city’, as carved into its relief walls. Its height, 62 metres, matches the distance from this spot to the bakery identified as the fire’s origin.A few minutes’ walk from here lies Lloyd’s of London.

To enter Lloyd’s of London, the person who brought us along must present their “Lloyd’s Building Access Pass”. Beside them, accompanying visitors present their “business card” and “photo ID” (an ID card with a photograph) to receive a “date-specific access pass”.Five years ago, just before the covid-19 pandemic, when I visited London, it was a “paper” pass, but before that, it was a plastic card like the one pictured as shown in the photograph below.

This “access pass” has the following written on its reverse: “Please hand to reception or security on final departure or expiry”.

I usually returned it to reception with a “Thank you”. However, that day, I entered the Lloyd’s of London Building for business discussions in the morning, then went out for lunch with an underwriter. That lunch turned into a “long lunch” and lasted until dinner. Consequently, I was unable to return it and still have it in my possession.

The date is 26 June 2015, with the author’s name written below. Further down, it states ‘COSMOS GUEST’. This indicates entry to the Lloyd’s Building was facilitated by Cosmos Rusk Solutions, an insurance and reinsurance broker and wholly owned subsidiary of Itochu Corporation, with whom we had a business partnership at the time.

‘UWF’ (Underwriting Floor) is noted. ‘General visitors to the Lloyd’s of London Building’ are not permitted entry; this pass signifies ‘permission to enter the Underwriting Floor, where the actual underwriting boxes conducting insurance transactions are located’.

However, further down it states: ‘This pass does not permit the holder to conduct insurance business in the room’. Thus, as the author is not a Lloyd’s broker, it is explicitly stated that ‘this pass does not permit the holder to conduct insurance business in the underwriting room (floor)’, clearly indicating that ‘only Lloyd’s brokers may conduct insurance business within Lloyd’s of London’.

② Lloyd’s broker

Thus, within the Lloyd’s of London building, only underwriters belonging to insurance syndicates and approximately 400 authorised Lloyd’s brokers possess the authority to conduct insurance transactions.

Therefore, to conduct insurance negotiations within the Lloyd’s of London building, entry must be accompanied by a Lloyd’s broker. Furthermore, as stated in the proviso of the aforementioned Pass: ‘This does not permit insurance transactions to be conducted in the Underwriting Rooms (Floor)’, clients cannot discuss insurance transactions, development, or similar matters with underwriters within Lloyd’s of London without being accompanied by a Lloyd’s broker.

However, in 2008, the aforementioned Lloyd’s Act was amended, permitting transactions with brokers meeting certain criteria, not just Lloyd’s brokers. In practice, however, little has changed, and it remains common industry knowledge that ‘transactions at Lloyd’s of London are conducted through Lloyd’s brokers’.

This, however, strictly applies only to transactions within the underwriting rooms of the Lloyd’s of London Building. Conversations about insurance transactions held at offices maintained by syndicates outside the Lloyd’s of London Building are a separate matter.

Managing agents and syndicates, primarily insurance company-affiliated entities that own and manage Lloyd’s of London syndicates, often possess local subsidiaries of insurance companies in addition to their underwriting boxes within the Lloyd’s Building. Consequently, it is common for them to suggest conducting discussions at their offices.

This practice stems partly from a desire to avoid contributing a percentage of premium income to the “Central Fund” as “stabilisation capital” for the entire Lloyd’s of London syndicate. However, a more significant reason is to prevent others from realising that highly confidential deals or discussions about major projects are taking place within the underwriting room, where brokers are constantly waiting their turn around the boxes.

The non-life insurance company for which the author was commissioned as a management consultant for many years developed insurance products in collaboration with a Lloyd’s of London syndicate and provided reinsurance to that syndicate.

Presumably because the loss ratio was exceptionally favourable – meaning highly profitable – the managing agent once requested a change of reinsurance provider, directing business to an insurance company established by its parent reinsurance firm. As this insurer posed no security concerns for reinsurance, the change was made without objection, as I recall.

In the 1960s, and 1970s, the term ‘London Market’ for reinsurance generally referred to Lloyd’s of London. However, for the reasons outlined above, and particularly since global reinsurance companies established significant bases in London, the term has increasingly come to denote the insurance and reinsurance companies operating within the City of London, including Lloyd’s of London.

③Lessons from the London Market

Lloyd’s of London and the London Market are characterised by ‘risk sharing’.Recently, in Japan, the practice of non-life insurance companies sharing underwriting responsibilities (“sharing”) with other non-life insurers for large corporate insurance transactions has, for some reason, been viewed critically. To this writer, this appears truly peculiar.

The reason is that, unlike life insurance, the risks covered by non-life insurance are highly uncertain, making unforeseen events more likely. Therefore, it is crucial to have as many and as robust risk-hedging measures as possible.

The method devised for this risk dispersion is reinsurance. Naturally, dispersing risk across the reinsurance networks of multiple non-life insurers yields greater benefits than relying on a single insurer’s network. It creates a larger risk dispersion network, enhances the stability of compensation, and consequently increases the stability of the non-life insurer itself, as well as the certainty of claim payments. From these perspectives too, the risk dispersion method that should be promoted is precisely ‘sharing the risk’.

Lloyd’s of London has navigated numerous challenging circumstances and endured for over 300 years. This resilience can be attributed solely to its thorough implementation of this “risk diversification” principle.

④ Line slip

The very method of risk diversification and risk sharing practised at Lloyd’s of London and in the London Market is the line slip.

The official website of Lloyd’s of London states the following regarding line slips, which is quoted below.

A line slip is an agreement whereby a Managing Agent delegates its authority to enter into contracts of insurance to be underwritten by the members of a syndicate managed by it to another Managing Agent or authorised insurance company in respect of business introduced by a Lloyd’s Broker named in the agreement.

Managing Agents do not require approval from Lloyd’s to operate under a line slip.

Once the Managing Agent or insurance company acting as the line slip lead underwriter has entered into a contract of insurance with the insured, the evidence of insurance will normally be issued by means of a MRC contract or via a certificate / policy. The format of the insurer authorised documentation will be determined within the line slip agreement.

Indeed, the document indicating “sharing” (share) of underwriting with other syndicates and/or non-life insurance companies is the “Line slip”.

The actual document consists of a form like the one pictured above, to which the syndicate or the insurance company’s underwriter attaches a signed document containing pages such as “Details of Cover”, “Agreed Terms”, and “Policy Conditions”. In the example pictured, as indicated by “page 6 of 12” in the top right corner, the document comprises a total of 12 pages.

Though faint, the words ‘Broker at Lloyd’s’ appear in the bottom right corner. This signifies that the document was ‘prepared by’ a Lloyd’s broker.

In Japan, ‘most insurance contracts involve an “insurance agency”, which is an “agent” of the non-life insurance company’. Therefore, ‘insurance policy documents guaranteeing cover’ are all prepared by the non-life insurance company. However, the London Market is a ‘broker market’. Consequently, such Line slips (which, like insurance policies, guarantee cover) are prepared by the broker and brought to the underwriter.

Upon obtaining underwriting approval, the Line slip is finalised and cover commences when the syndicate or insurer’s “stamp” is applied as evidence of this approval and the underwriter “signs” it.

I considered it important to see the “actual item”, so I insisted on the “actual item” rather than a “blank line slip”. This is a line slip from when, ten years ago on 20 July 2015, a major reinsurance company – one of the world’s largest with a significant presence in the London market – underwrote reinsurance from a captive established in Hawaii by a certain company, facilitated by our firm Global Link’s consultancy. Whilst publishing the “physical document”, please understand that, due to confidentiality obligations, we have opted to display a “line slip that is no longer in force” whilst still being “as old as possible”, and have further applied “black masking”.