キャプティブ 2020.06.01

CA15 志賀櫻先生の教え Teachings of Mr. Sakura Shiga

目次

Copyright © Shinichiro Hatani 2020 All rights reserved

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

「中央 ロー・ジャーナル(2013年12月:中央大学法科大学院刊)」には:

皆さんもタックス・ヘイブンという言葉を聞いたことがあると思います。ケイマン諸島とかを利用していろいろな操作をして税金を払わないで済ませると言うことなのですが、これが世界的な規模でやられているということです。米国の巨大企業が、それを利用したとかで大きな記事になった時期がありまして、本年のG8(主要国首脳会議)でもそれが主要な議題として取り上げられました。ここで少し手前味噌の話になりますが、「タックス・ヘイブン-逃げていく税金」という志賀櫻という人が書いた本が、近頃岩波新書から出まして、その中で私の補足意見についてコメントがしてありました

との記述がある、「最高裁判所在任時代を回顧する」と題して、須藤最高裁判所判事が退官記念講演をおこなった際の講演録を掲載した「中央ロー・ジャーナル」からの抜粋である。

1.「タックス・ヘイブン-逃げていく税金」(岩波新書刊)

本コラムの「キャプティブ3-最高裁への鑑定意見書」にも記したが、2014年(平成26年)1月、グローバル・リンクは、志賀 櫻 氏を顧問として迎えた。当時、日本弁護士連合会税制委員会副委員長の要職にあり、国際租税学会理事日本国代表、東京税関長、大蔵省主税局国際租税課長、OECD租税委員会日本国代表という蒼々たる役職を歴任された弁護士であった。

「タックス・ヘイブン-逃げていく税金」(岩波新書刊)にはこうある。

「税制の根幹を破壊する悪質な課税逃れ。そのカラクリの中心にあるのがタックス・ヘイブンだ。マネーの亡者が群れ蠢く、富を吸い込むブラックホール。市民の目の届かない場所で、税負担の公平を覆す様々な悪事が行なわれている。その知られざる実態を明らかにし、生活と経済へ及ぼす害悪に警鐘を鳴らす。」

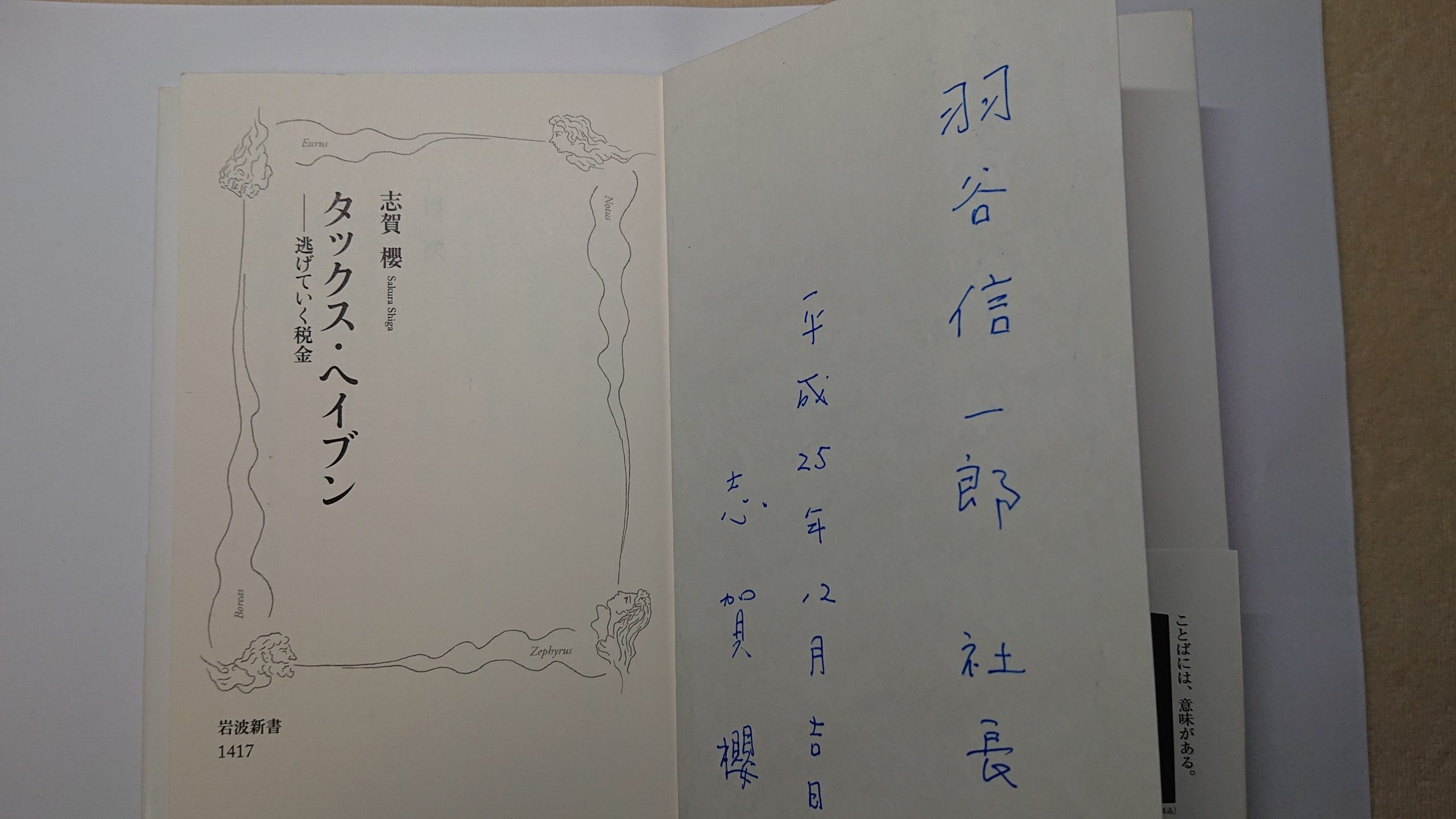

志賀櫻弁護士とは、思いもよらない不思議な巡り合わせでお会いできた。事務所に伺った時、出版されたばかりの「タックス・ヘイブン-逃げていく税金」を頂戴したが、その際、「実は、私の紹介が出ていまして」と、にこやかに微笑みながら併せて頂いた本が、冒頭の「中央 ロー・ジャーナル(2013年12月:中央大学法科大学院刊)」であった。

そして「羽谷さん、グローバル・リンクが、『キャプティブからの再保険をロンドンの再保険市場で世界最大級の再保険会社に的確に手配して、タックスヘイブンではない、米国、ハワイにキャプティブを設立する』というビジネスモデルは大変賢明なものであると思います。だから応援させていただきたい」とエレベーターホールまでお見送りいただいた際のお言葉は今でも耳朶に鮮明に残っている。

2.ガーンジー島事件

最高裁が、「タックス・ヘイブン対策税制」との関係で、非常に重要な判示を行ったのが、ガーンジー島事件である。

このタックス・ヘイブン対策税制とは、日本国内の納税者(個人又は会社)が、国が定める税率より低い外国・地域(タックス・ヘイブン(租税回避地))に会社等を設立した場合に、その外国会社の所得を国内の納税者の所得と合算して課税するというものである。日本の納税者が税率の低い国に会社を作って、本来は日本で課税されるべき所得をその会社に移転、課税を回避しようとすることを規制しようとするものであり、典型的な規制対象は海外のペーパーカンパニーである。そのため、「海外に子会社を設立する経済的合理性があると認められる場合」には、このタックス・ヘイブン対策税制の適用はない。

ガーンジー島という、英仏海峡にある、「イギリス王室属領であり、税金については英国本国と異なる制度が採られているタックス・ヘイブンの地」に、日本企業が子会社を設立、現地で税金を納めていたが、ガーンジー島においては、一定の要件を満たした外国資本法人の所得税(日本でいう法人税)については、税務当局の承認を条件に、「0%を超え30%以下の割合の中から税率を選択して申請することができる」という制度が採用されていた。その企業は、当時の日本では税率が25%以下の外国・地域については「タックス・ヘイブン対策税制」が適用されていたため、25%やそれより少ない税率を選択すると、タックス・ヘイブン対策税制が適用され、子会社の所得にも日本の税率が適用されて課税されることになるため、「26%の税率を選択」して納税をしていた。

この日本の企業を所轄する税務署は、「『税金』として払っているものは、日本の法人税法上の『外国法人税』には該当しないので、ガーンジー島子会社にもタックス・ヘイブン対策税制の適用がある」と主張、ガーンジー島子会社の所得も合算してその日本企業への課税処分を行った。

これを不服としてこの日本企業は提訴、東京地裁(第一審)及び東京高裁(控訴審)は原告敗訴で「税務署の判断を支持した」が、最高裁では、志賀櫻弁護士の「鑑定意見書(2007年12月28日付)」が決め手となり原告の逆転勝訴となった事案である。

3.キャプティブをどこにつくるか

キャプティブを設立する背景としては様々なことが考えられるが、「企業が成長するにしたがい、一般に販売されている保険では自社の複雑で巨大化するリスクに対応できなくなってきた」というものが一番多い理由である。

キャプティブの設立を検討していくと、「 キャプティブを使ったリスクコストの方が現在の保険プログラムよりも低いこと」、また「現在の保険プログラムの取り扱いと遜色のない利便性」、そして「日本で一般的に得られる保険よりも広範な補償が得られやすい」これらのことが認識されていき、グローバル・リンクのようなキャプティブ・コンサルティング会社との詳細な検討の結果、最適なキャプティブの設立地(ドミサイル)の選択がおこなわれる。

日本企業によるキャプティブの最初の設立の地は、バミューダと言われている。有名なタックス・ヘイブン(租税回避地)でありキャプティブの数が世界で一番多いドミサイルである。また、日本企業のキャプティブの誘致に熱心で、日本のタックス・ヘイブン対策の「トリガー税率」との対比からキャプティブの税率を決めたと言われているミクロネシア、シンガポール、マレーシアのラブアン、ヨーロッパのルクセンブルグ、米国のバーモント州、そしてハワイ州、前述のバミューダそしてケイマン諸島、これらの地が日本企業の代表的なドミサイルになっている。

4.これからのキャプティブの設立地(ドミサイル)

2017(平成29)年度の税制改正において、タックス・ヘイブン対策税制の大幅な見直しが行われた。それまでは、租税負担割合が20%未満か否かによって「特定外国子会社等」に該当するか否かを判定していた。この20%は、「トリガー税率」と言われ重要な意味を持つものであった。

しかし、明らかに受動的な所得しか得ていない、経済実体のないペーパーカンパニー等については、「租税負担割合が20%以上であるという事実だけで制度の適用を免除するのは問題がある」という議論により、制度適用免除基準としての税率基準(租税負担割合)は残されているが、トリガー税率は廃止された。また、ペーパーカンパニーや「事実上のキャッシュボックス」という新たな概念の定義があり、そのような会社に対しては、合算課税制度が創設された。このように、実際の「租税負担割合が20%以上」であったとしても、ペーパーカンパニー等に該当すると当該企業の全ての所得に対し合算課税が生じることになった。

タックスヘイブンの泰斗として著名であった志賀櫻先生の言葉、「グローバル・リンクが、キャプティブからの再保険を的確に得て、タックスヘイブンではない米国、ハワイにキャプティブを設立するというビジネスモデルは大変賢明であると思います。だから応援させていただきたい」は、「キャプティブの適格性」、また「ドミサイルの選択」に於いて非常に重要な示唆を与える言葉ではないだろうか。

今回のまとめ

2017(平成29)年度の税制改正によって、「グローバル・リンクが主唱してきた『ソリューション・キャプティブ®』こそ、リスクマネジメントを追求した本来のキャプティブ、適格なキャプティブである」ということが明確になったと考えている。

キャプティブからの再保険の手配さえできない、つまりは「的確なリスクマネジメントができないプレーヤーがつくるキャプティブはキャプティブではない」との表明であり、不適格なプレーヤーは市場から撤退し始めているようである。

新型コロナ・ウイルスの世界的な感染という非常に大きなリスクに遭遇しているいま、リスクマネジメントを推進していくことが、自社、そしてステークホルダーに与える効用は非常に大きい。こういう認識のもと、あらゆるリスクに真正面から向き合い、「ピンチをチャンス」に変えるソリューション・キャプティブ®を設立する絶好の機会が訪れたと言えるのではないだろうか。

昨日5月31日未明、北海道十勝沖を震源とする地震があり、釧路市や根室市などで震度4の揺れを観測した。本日6月1日午前6時2分頃、茨城県北部を震源とするマグニチュード5.3の地震が発生し、茨城県、栃木県、群馬県で最大震度4を観測した。首都圏では昨年末より立て続けに大きな地震が起きている。そして午前9時33分頃、鹿児島県で震度4の地震があった。日本列島の北から南まで「動いている」のが解る。

新型コロナ・ウイルスの感染拡大という大きなリスクよりも、更に大きな、一旦起きると『国難」とも言うべき甚大な損害を与える可能性のある、首都圏直下地震、南海トラフ地震に備えるため、広範な補償を有する地震保険をソリューション・キャプティブ®によって得ておく時が今ではないだろうか。

新型コロナ・ウイルスの感染拡大で学んだ通り、「起きてからでは遅いから」である。

執筆・翻訳者:羽谷 信一郎

English Translation

Captive 15 – Teachings of Mr. Sakura Shiga

In the “Chuo Law Journal” (December 2013: published by Chuo University Law School):.

I’m sure you’ve heard of the term “tax havens”. The idea is to manipulate the Cayman Islands to avoid paying taxes in various ways, but this is being done on a global scale. There was a time when it was reported that a huge company in the US took advantage of this, and this was the main topic of discussion at the G8 (Group of Eight) meeting this year. The book “Tax Havens – Escaping Taxes” written by Mr. Sakura Shiga has recently been published by “Iwanami Shinsho”, in which he commented on my supplementary opinion.

This is an excerpt from the “Chuo Law Journal”, which published the transcript of a lecture given by Supreme Court Justice Sudo at a memorial lecture for his retirement, titled “Retrospective on the Supreme Court’s tenure”.

1. “Tax Havens – Escaping Taxes” (“Iwanami Shinsho”)

As mentioned in “Captive 3 – Opinion to the Supreme Court” in this column, Global Link welcomed Mr. Sakura Shiga as an advisor in January 2014. At the time, he was a key member of the Taxation Committee of the Japan Federation of Bar Associations, and had served in a number of important positions, including Director of the International Taxation Society, Head of Tokyo Customs, Director of the International Tax Division of the Ministry of Finance’s Taxation Bureau, and Representative of Japan on the OECD Tax Committee.

In the book “Tax Havens – Escaping Taxes”(Iwanami Shinsho) , he writes: “Malicious tax dodging that destroys the very foundation of the tax system. Tax havens are at the heart of this scheme. It is a black hole in which money grubbers swarm, sucking up wealth. A variety of evil deeds are taking place out of sight of the citizens, which upset the fairness of the tax burden. This book exposes the hidden reality of these wrongs and sounds a warning about the harm they are doing to people’s lives and the economy.”

I met Mr. Sakura Shiga through a curious and unexpected turn of events. When I visited his office, he gave me a copy of the recently published “Tax Havens – Escaping Taxes,” which he gave me with a smile and said, “Actually, I was introduced in the book,” and the book he gave me was the “Chuo Law Journal (December 2013: Chuo University Law School)” mentioned at the beginning of this article.

He said, “Mr. Hatani, I think Global Link’s business model of establishing a captive in Hawaii, the U.S. , which is not tax havens, is a very wise one. That’s why I would like to support you,” he said as he escorted me down the elevator hall, a comment that remains vividly in my ear.

2. The Guernsey Incident

The Supreme Court made a very important ruling in the Guernsey case in relation to “tax havens”.

In this case, the tax havens measure is based on the idea that when a Japanese taxpayer (an individual or a company) establishes a company in a foreign country or region (a tax haven) with a lower tax rate than the national tax rate, the income of the foreign company is taxed by adding the income of the domestic taxpayer to that of the domestic taxpayer. The idea is to regulate the establishment of a company in a country with a lower tax rate by a Japanese taxpayer to transfer income that should be taxed in Japan to that company and avoid taxation. As a result, this anti-tax haven tax regime does not apply if “it is deemed economically reasonable to establish a subsidiary abroad”.

On the island of Guernsey, located in the English Channel, a Japanese company established a subsidiary and paid taxes there “in a tax haven which is a British Crown territory and has a different taxation system from that of the United Kingdom”. (the corporate tax referred to as “corporate tax”) was subject to the approval of the tax authorities, which allowed companies to choose a tax rate from among a percentage of more than 0% and not more than 30% to apply. That company was subject to the “anti-tax haven tax system” in Japan at that time for foreign countries and territories with a tax rate of 25% or less, so if it elected a tax rate of 25% or a lower rate, it would be subject to the anti-tax haven tax system and the income of the subsidiary would be taxed at the Japanese tax rate. It had “elected the 26% tax rate” and paid the tax.

The Japanese tax authorities had also added the income of the Guernsey subsidiary to the taxable income of the Japanese company and imposed a tax on the Japanese company, arguing that what the Japanese company was paying as ‘tax’ did not qualify as ‘foreign corporate tax’ under Japanese corporate tax law, and therefore the subsidiary was also subject to taxation.

The Japanese company was dissatisfied with this and filed a lawsuit, and the Tokyo District Court (first instance) and the Tokyo High Court (second instance) lost the case for the plaintiff and “upheld the decision of the tax office”, but in the Supreme Court, the plaintiff won a reversal of the case on the basis of “an expert opinion dated December 28, 2007”, written by attorney Sakura Shiga.

3. Where to establish a captive

There are many possible reasons for establishing a captive, but the most common reason for establishing a captive is that as a company grows, the commonly available insurance program is no longer able to handle the company’s increasingly complex and large risks.

When considering the establishment of a captive, it was recognized that the cost of risk using a captive is lower than current insurance programs, that it is as convenient as current insurance programs, and that it is easier to get coverage that is broader than what is typically available in Japan. After detailed discussions with a captive consulting firm such as Global Link, the selection of the most appropriate captive location (domicile) will be made.

It is believed that the first captive to be established by a Japanese company was in Bermuda. It is a famous tax haven and has the largest number of captives in the world. The states of Singapore, Labuan in Malaysia, Luxembourg in Europe, Vermont in the United States, Hawaii, as well as the aforementioned states, Bermuda and the Cayman Islands, and Micronesia which is said to be keen on attracting Japanese captives and to have determined the tax rate for captives based on the contrast with the “trigger tax rate” of Japan’s anti-tax haven policy, which are the leading domicile for Japanese companies.

4. The future location (domicile) of the captive

In the 2017 tax reform, the taxation system against tax havens was significantly revised. Until then, whether or not a company qualified as a “specified foreign subsidiary, etc.” was determined by whether the tax burden ratio was less than 20%. This 20% was referred to as the “trigger rate” and had an important meaning.

However, as for the paper companies without economic substance, which clearly have only passive income, the tax rate criterion (tax burden ratio) as an exemption criterion has been left in place by the argument that “it is problematic to exempt them from the application of the system only by the fact that the tax burden ratio is 20% or more”. Trigger tax rates were abolished. There is also a new definition of the concept of paper companies and “de facto cash boxes”, and a combined taxation regime has been created for such companies. Thus, even if the actual tax burden is 20% or more, if a company falls under the category of a paper company, etc., it will be subject to the combined taxation of all the income of the company in question.

In the words of Mr. Sakura Shiga, a famous tax havens expert, “I think the business model of Global Link getting reinsurance from a captive and establishing a captive in the US and Hawaii, which are not tax havens, is very wise. So we would like to support it” are very important implications in “captive eligibility” and in “choice of domicile”, I think.

Summary of this issue

We believe that the 2017 (Heisei 29) tax reform has made it clear that “the ‘Solution Captive®’ that Global Link has been championing is the original and qualified captive that pursued risk management.

The inability to even arrange reinsurance from a captive, in other words, a statement that “a captive created by a player who cannot manage risk accurately is not a captive”, and the ineligible players seem to be starting to exit the market.

At a time when we are facing the enormous risk of a global outbreak of a new coronavirus, the benefits to the company and its stakeholders of promoting risk management are enormous. With this in mind, there has never been a better time to establish a Solution Captive® to face all the risks head on and turn a pinch into an opportunity.

Yesterday, May 31, an earthquake centered off the coast of Tokachi, Hokkaido struck Kushiro, Nemuro and other areas, with a magnitude of 4 on the Japanese intensity scale. At 6:02 a.m. on June 1, an earthquake measuring 5.3 on the Richter scale struck the northern part of Ibaraki Prefecture, with a maximum magnitude of 4 on the Richter scale in Ibaraki, Tochigi and Gunma Prefectures. The Tokyo metropolitan area has been hit by a series of major earthquakes since late last year. At around 9:33 a.m., a magnitude 4 earthquake struck in Kagoshima Prefecture. It could be seen moving from the north to the south of the Japanese archipelago.

In order to be prepared for an even bigger earthquake in the Tokyo metropolitan area or the Nankai Trough, which could cause enormous damage and could be called a national crisis, now is the time to obtain earthquake insurance with extensive coverage through Solution Captive®.

As we have learned from the spread of the new coronavirus, “by the time it happens, it’s too late”.

Author/translator: Shinichiro Hatani