キャプティブ 2023.05.10

CA50 昔、多摩は海だった

目次

Copyright © Shinichiro Hatani 2023 All rights reserved

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

日本海側、金沢でマグニチュード6.5、震度6強の大きな地震が5月5日午後発生した。政府「地震調査研究推進本部」の公式WEBサイトには以下の記述がある。

石川県では、南海トラフ沿いの巨大地震のなかで、紀伊半島沖から遠州灘、駿河湾が震源域になった場合、地震の揺れによる被害を受けています。1944年の東南海地震(M7.9)では、県内で家屋全壊などの被害が生じました。

石川県の主要な活断層は、能登半島に邑知潟断層帯と、その延長上に森本・富樫断層帯があります。また、富山、岐阜県との県境付近に庄川断層帯が、福井県との県境付近に福井平野東縁断層帯があります。

また、石川県周辺に震源域のある海溝型地震はありませんが、前述のように、日本海東縁部や南海トラフ沿いで発生する地震で被害を受ける可能性もあります。

日本が現在位置している場所は元々は海、そこにユーラシア大陸から陸地が離れていき出来上がったのが日本列島である。「『南海トラフ巨大地震』と言ってもそれは太平洋側のこと、日本海側は関係無い」とは、言えないようである。

「昔、多摩は海だった」と書くと「どこの多摩?」と質問が飛んできそうだが、東京近郊の多摩地方にまで海、「古東京湾」と呼ばれる海が入り込んでいた。12万年前の出来事である。

「地球温暖化」という言葉が使われて久しいが、「東京湾の水位が上昇して東京ディズニーランドが水没した」というニュースは聞かない。しかし、昔、地球軌道の変化によって最終氷期を境にいくつか気温の変化はありながらも、地球の気温は継続的に上昇、氷が融け海洋に流出して海面が上昇していった時代があった。

「海進」と呼ばれる現象、海面が上昇して海岸線が内陸に移動する地質学的現象のことである。結果、「それまでの陸地が海になった」のである。この反意語が「海退」であり、この海退と海進は、造山運動などの地殻変動や氷河期などの大規模気候変動等によって引き起こされた。巨大な恐竜が跳梁跋扈した「ジュラ紀」、その後、現代から1億4,500万年前からおよそ6,600万年前まで地球の地質時代を指す「白亜紀」に起きた海進では、海面上昇の結果、北米大陸の中央部には海ができるなど陸地の面積が大幅に縮小した。

その「海進」の一つ、神奈川県にある地名「末吉」から取られた「下末吉海進」と呼ばれる海進は約12万年前に起き、東京の中央線沿線の三鷹市にまで海が入り込んでいた。その後、約2万年前に起きた「海退」により、今度は海面が現在より125メートルも低くなり東京湾も干上がって、巨大な関東平野が出現していた。

1.地球規模の環境変遷

「東京都葛飾区のホームページの『葛飾区史』」には次の記述がある。

12万年前は現在より海水面が高く、房総半島は島であった。この頃の内海を指して古東京湾と呼ぶ。旧石器時代は最終氷期にあたり、氷河が発達していたため海面が現在より著しく低く、浦賀水道付近以北は陸地となっており、「古東京川」と呼ばれる川が流れていた。

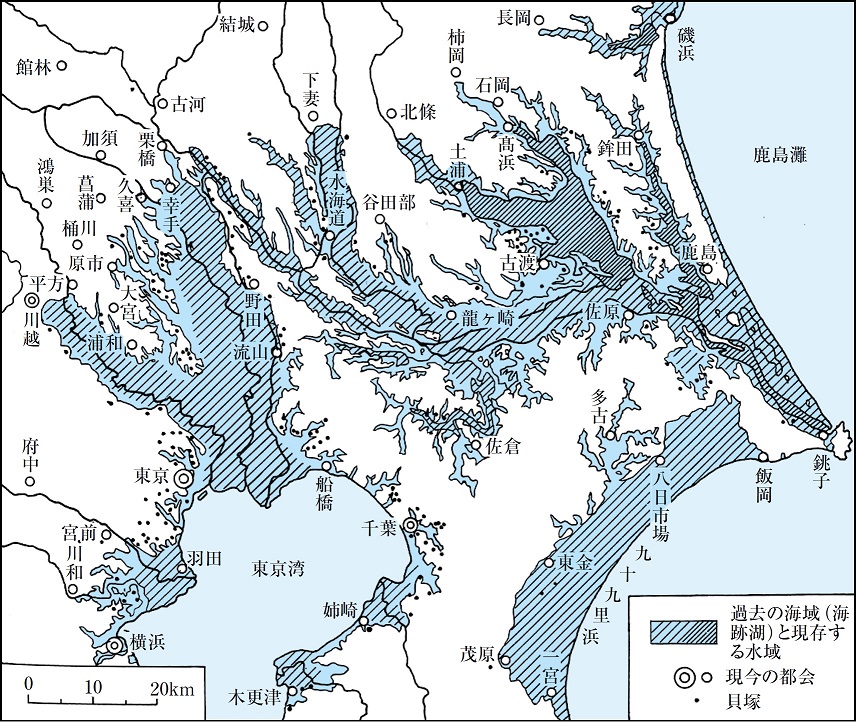

その後の地球の地質区分で「完新世」、また「ヒプシサーマル」と呼ばれている時期は、日本での「縄文時代」と重なり、日本列島のように、氷河から遠く離れた地域では海水面が大きく上昇、ピーク時である約6,000年まで上昇、海水面が5メートルほど高くなり、関東地方の貝塚の分析から「群馬県邑楽郡板倉町付近」や「埼玉県さいたま市」付近まで海が入り込んだことが裏付けられている。

「東京都葛飾区のホームページ」に掲載されている下図を見ると、当時、海が内陸部深くまで入り込んでいたことがよく理解できる。

(出典:「東京都葛飾区」ホームページ)

このヒプシサーマルの時期、氷河は北米やヨーロッパから姿を消し、グリーンランドと南極大陸に残るのみとなった。この氷河が溶けた水の流出は、かつて氷河があった場所からはその重みが無くなり、一方海底には新たな重みが加わり、結果、陸上では隆起運動、海洋では沈降運動が起き、その動きは現在でも続いている。この温暖化によって、地球各地では、湿潤化して森林が増加、草原の減少が起き、マンモスなど大型哺乳類を絶滅させることになったとされている。

現在のインドネシアやフィリピンなどがユーラシア大陸から分離して島となり、北米大陸もユーラシア大陸から分離、9600年前ころ、ドーバー海峡が出現、グレート・ブリテン島が大陸から切り離された時期である。

2.キャプティブの有用性

企業が工場で生産した製品は、できるだけ安価な輸送手段で消費地に届けたいと考えるため、工場は、一般的には港湾に近い場所に建設されるが、このことは「液状化」に遭うリスクを高めることにもなっている。しかも、「昔、海だった場所」が液状化するリスクは想像に難くない。その地域が関東平野全域に拡がっているのである。

地震が発生して工場の建屋や製品、半製品等が受ける直接的な損害のみならず、この液状化による損害は、東日本大震災の際に関東地域で発生した大規模な液状化現象による損害額が大きかったことは記憶に新しい。「キャプティブ」を介した地震保険プログラムの必要性が強く叫ばれる所以である。

この液状化リスクは「生産設備の回復遅れ」や「製品の搬出困難」を引き起こす。そのため、企業業績に大きな影響を与え、企業収益の低下をきたす可能性が高い。しかし、日本で企業向けに販売されている一般的な地震保険は、直接の「物的損害:PD (Property Damage(プロパティ・ダメージ)」のみが補償される傾向が強く、損害保険会社がこの「事業の中断による収益低下リスク:BI(Business Interruption)(ビジネス・インタラプション)」を積極的に引き受けることはないからである。

一方、欧米で普通に販売されている地震保険は「物的損害:PD(Property Damage) 」に加え、この地震による「事業の中断による収益低下リスク」(「Business Interruption(ビジネス・インタラプション):BI」)が補償されている、「物的損害リスク対応」だけでは片手落ちで「事業の中断による収益低下リスクへの対応」が無ければ「地震保険としての意味が無いから」である。ここにキャプティブを設立する大きなメリットが存在するのである。

日本では一般的ではない「地震保険の補償:事業の中断による収益低下リスク」をキャプティブからの再保険(保険契約者から見れば再々保険となる)を受けるロンドン・マーケットの再保険会社で確保して日本の元受保険会社に提供する、このことによって、地震による「事業の中断による収益低下リスク」を補償することができるからである。

今回のまとめ

「液状化」が考えられる地域は全国各地に存在する。

日本は、国土の約75%が山地であり、 山地は谷が細かく入り組み、その斜面は急傾斜となり「段丘」が多くの地で見られる。懸念されている「南海トラフ巨大地震」が発生した場合、その影響を受ける地域では建物の揺れによる倒壊だけではなく、「東日本大震災」の際、東京湾沿岸を中心に液状化に依る被害が広く発生したように、「大規模な液状化現象」が起きる可能性が高い。

液状化は、堆積した砂の地盤が、干拓地等で水を多く含んでいる場所で起こり、地盤が液体状となるため建物は沈み込んでいく。東日本大震災の際、千葉県浦安市の多くの住居に発生したことはマスコミでも多く取り上げられたが、東京湾の沿岸部にある多くの「工場」「事務所」等でも大きな損害が発生したことはあまりメディアには出ていないため知られていない。

工場が傾くと収容、装備されている機械類も傾く、そうなると生産が長期間不可能になり、企業収益に大きなマイナスの影響を与える。「地震リスク」と言うと多くの人が「建物が倒壊する、壊れるリスク」を考えるが、建物は土台さえしっかりしていればその復興に要する時間は短い、しかし「地盤の整備、強化」からおこなっていかなければならない「液状化リスク」は復興までの期間が長期化するという点で企業の収益に与える影響が実は大きいのである。

ただ、日本では「地震保険=物的損害リスクへの補償」と見なされてきたため、損害保険会社が、この「事業の中断による収益低下リスク」(英文では「Business Interruption(ビジネス・インタラプション):BI」を引き受けることは一般的ではない。ただでさえ不足がちな「地震保険キャパシティ(引受力)」を広範なリスクに適用して「地震保険キャパシティ」を払底させたくないからである。

一方、欧米で、ごく普通に販売されている地震保険は「物的損害:PD(Property Damage)」に加え、この地震による「事業の中断による収益低下リスク」(英文では「Business Interruption(ビジネス・インタラプション):BI」)も補償するものである、「物的損害リスク」だけでは片手落ちで「事業の中断による収益低下リスク」が無ければ「地震保険としての意味が無いから」である。

ここにキャプティブを設立する大きなメリットがある。この日本では一般的に手に入らない「事業の中断による収益低下リスクへの地震補償」をキャプティブからの再保険を受けるロンドン・マーケットの再保険会社で確保して日本の元受保険会社に提供する、このことによって、日本の元受保険会社は、地震による「事業の中断による収益低下リスク」を補償することができるからである。

「本当に怖いリスク、対処しなければならないリスク、経営に大きな影響を与えかねないリスク」に焦点を当てリスクマネジメント対応をするためには、キャプティブのこの大きなメリットを活かす必要がある。「コロナ禍以上、日本にとって最大級のリスク、巨大地震リスク」に備えるため、早急にキャプティブの設立を検討する必要があるのではないだろうか。

執筆・翻訳者:羽谷 信一郎

English Translation

Captive (CA) 50 – Tama used to be a sea

A major earthquake with a magnitude of 6.5 on the Richter scale and a seismic intensity of 6+ occurred in Kanazawa, on the Sea of Japan side, in the afternoon of 5 May.

The official website of the government’s Headquarters for Earthquake Research Promotion states;

Ishikawa Prefecture has suffered damage from seismic tremors when the epicentre area is off the Kii Peninsula to the Sea of Enshu and Suruga Bay in a major earthquake along the Nankai Trough.

The main active faults in Ishikawa Prefecture are the Ouchigata Fault Zone on the Noto Peninsula and the Morimoto-Togashi Fault Zone as an extension of the Ouchigata Fault Zone. There is also the Shogawa fault zone near the border with Toyama and Gifu prefectures, and the Fukui Plain East Rim Fault Zone near the border with Fukui Prefecture.

There are no trench earthquakes with epicentres in the vicinity of Ishikawa Prefecture, but as mentioned above, there is a possibility of damage from earthquakes occurring along the eastern margin of the Sea of Japan and the Nankai Trough.

The place where Japan is currently located was originally a sea, and the Japanese archipelago was formed there as land separated from the Eurasian continent. It seems that it is not possible to say, “When we say ‘Nankai Trough giant earthquake’, we mean on the Pacific Ocean side and not on the Sea of Japan side.”

When I write “Tama used to be the sea”, the question might be asked, “Where in Tama?” This happened 120,000 years ago.

The term “global warming” has been used for some time now, but we have not heard news of Tokyo Disneyland being submerged due to rising water levels in Tokyo Bay. However, there was a time in the past when changes in the Earth’s orbit caused a continuous rise in global temperatures, despite some temperature changes after the last ice age, and sea levels rose as ice melted and flowed out into the oceans.

This is a phenomenon known as “sea advance”, a geological phenomenon in which the sea level rises, and the coastline moves inland. As a result, “the land that had previously been land became sea”. The antonym of this is ‘sea retreat’, and this sea retreat and sea advance were caused by tectonic movements such as orogenic movements and large-scale climate changes such as ice ages. During the Jurassic Period, when giant dinosaurs roamed the Earth, and later during the Cretaceous Period, which refers to the geological age of the Earth from 145 million to 66 million years ago, sea-level rise resulted in a significant reduction in land area, including the formation of an ocean in the middle of the North American continent.

One of these “sea advances”, known as the Shimo-Sueyoshi sea advance, taken from the name of a place in Kanagawa Prefecture called Sueyoshi, occurred about 120,000 years ago, and the sea even entered Mitaka City along the Chuo Line in Tokyo. This was followed by the ‘sea retreat’, which occurred some 20,000 years ago, this time lowering the sea level by 125 metres below present-day levels and drying up Tokyo Bay, resulting in the emergence of the huge Kanto Plain.

1. global environmental change

The Katsushika Ward History on the Tokyo Metropolitan Government’s Katsushika Ward website includes the following statement: “120,000 years ago, the sea level was 125 metres lower than it is today”.

120,000 years ago, the sea level was higher than today and the Boso Peninsula was an island. The inland sea at this time is called Paleo-Tokyo Bay. The Paleolithic was the last glacial period, when the sea level was significantly lower than today due to the development of glaciers.

The period known as the “Holocene” or “Hypsithermal” in the subsequent geological classification of the Earth coincided with the “Jomon Period” in Japan, and sea level rose significantly in areas far from glaciers, such as the Japanese archipelago, until about 6,000 years, the peak period, when sea level rose by about 5 metres and the Analysis of shell middens in the Kanto region confirms that the sea entered as far as “near Itakura-cho, Ora-gun, Gunma Prefecture” and “near Saitama City, Saitama Prefecture”.

The diagram below from the Katsushika-ku, Tokyo website shows how the sea penetrated deep into the interior at that time.

(Source: “Tokyo Metropolitan Katsushika Ward” website)

During this Hypsithermal period, glaciers disappeared from North America and Europe, leaving only Greenland and Antarctica. The outflow of water from the melting glaciers has removed the weight of the glaciers from where they once stood, while adding new weight to the seabed, resulting in uplift movements on land and subsidence movements in the oceans, which are still occurring today. This warming is believed to have caused wetter conditions, increased forest cover and reduced grasslands in many parts of the world, leading to the extinction of large mammals such as the mammoth.

The present-day Indonesia and the Philippines separated from Eurasia and became islands, and the North American continent also separated from Eurasia, around 9600 years ago, when the Strait of Dover appeared and the island of Great Britain was cut off from the continent.

2. usefulness of captives

Factories are generally built in close proximity to ports, as companies want to deliver the products they produce in their factories to the point of consumption by the cheapest means of transport possible, which also increases the risk of encountering “liquefaction”. Moreover, it is not difficult to imagine the risk of liquefaction in “places that used to be seas”. This area extends over the whole of the Kanto Plain.

In addition to direct damage to factory buildings, products and semi-finished goods caused by earthquakes, the amount of damage caused by this liquefaction is fresh in the memory of the large scale liquefaction that occurred in the Kanto region during the Great East Japan Earthquake. This is why the need for an earthquake insurance programme via a ‘captive’ is so strongly called for.

This liquefaction risk causes “delays in the recovery of production facilities” and “difficulties in the removal of products”. It is therefore likely to have a significant impact on corporate performance and cause a decline in corporate earnings. However, general earthquake insurance policies sold to companies in Japan tend to cover only direct “property damage” (PD), while non-life insurance companies tend to provide coverage for this “risk of loss of earnings due to business interruption: BI (Business Interruption)”. Interruption (BI) (Business Interruption)” is not actively underwritten by non-life insurers.

On the other hand, earthquake insurance policies normally sold in Europe and the US cover “Business Interruption (BI)” in addition to “Property Damage (PD)”, which is the “risk of loss of earnings due to business interruption” caused by the earthquake. This is because ‘risk coverage’ alone is not enough, and “earthquake insurance is meaningless” if it does not “address the risk of loss of revenue due to business interruption”. This is a major advantage of establishing a captive.

The London Market reinsurers who receive reinsurance from the captive (from the policyholder’s perspective, this would be retrocession) will secure the “earthquake insurance coverage: risk of loss of earnings due to business interruption”, which is not common in Japan, and provide this to the Japanese primary insurers. This is because it compensates for the ‘risk of loss of earnings due to business interruption’ caused by earthquakes.

Summary of this issue

Liquefaction is possible in many parts of the country.

In Japan, approximately 75% of the country is mountainous terrain, with valleys and slopes that are steep and “terraced” in many places. In the event of a major Nankai Trough earthquake, which is a cause for concern, there is a high possibility of not only collapsed buildings in the affected areas but also large-scale liquefaction, as was widely observed during the Great East Japan Earthquake, especially along the Tokyo Bay coastline.

Liquefaction occurs in areas where the ground is made up of accumulated sand and contains a lot of water, such as reclaimed land, and the ground becomes liquid, causing buildings to sink. The fact that liquefaction occurred in many residences in Urayasu City, Chiba Prefecture, during the Great East Japan Earthquake was widely reported in the media, but it is not well known, as it is not often mentioned in the media, that many “factories”, “offices”, etc. in the coastal areas of Tokyo Bay also suffered significant damage.

When a factory tilts, the machinery in which it is housed and equipped also tilts, making production impossible for a long period of time and having a significant negative impact on company profits. Many people think of earthquake risk as the risk of buildings collapsing or being destroyed, but if a building has a solid foundation, the time required for reconstruction is short. However, the impact of liquefaction risk on a company’s profits is significant in that it takes a longer period of time to recover from liquefaction.

However, in Japan, non-life insurers do not generally underwrite the risk of business interruption (Business Interruption: BI), as earthquake insurance has been regarded as compensation for the risk of property damage. This is because insurers do not want to exhaust their “earthquake insurance capacity” by applying it to a wide range of risks for which they tend to have insufficient capacity.

On the other hand, earthquake insurance policies commonly sold in Europe and the US cover not only “property damage” but also “risk of loss of earnings due to business interruption” (Business Interruption: BI in English) caused by the earthquake. This is because ‘property damage risk’ alone is not enough, and without “risk of loss of revenue due to business interruption”, “earthquake insurance is meaningless”.

This is one of the major advantages of establishing a captive. The London Market reinsurers who receive reinsurance from the captive will provide the Japanese primary insurers with earthquake coverage for the “risk of loss of earnings due to business interruption”, which is generally not available in Japan. The Japanese primary insurers are not the only ones who are concerned about earthquake risk, as they are also able to compensate for the “risk of lost profits due to business interruption”.

This major advantage of captives needs to be exploited in order to focus risk management responses on “the really scary risks, the risks that need to be addressed, the risks that could have a major impact on business operations”. The establishment of a captive should be considered as soon as possible in order to prepare for “one of the biggest risks for Japan, beyond the Covid-19 disaster, the risk of a major earthquake”.

Author/translator: Shinichiro Hatani