キャプティブ 2022.03.10

CA35「東日本大震災級の海溝型巨大地震」に備えるキャプティブ

目次

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

本コラムでは、「プレート」という言葉をこれまで使ってきたが、改めてその意味を記すと、「プレート」とは、「大陸移動説」また「海溝型地震の発生原因」を解き明かす理論として1960年代に発展した地球科学の学説「プレートテクトニクス(プレート理論)」で、「地殻、地球の表面は十数枚以上のプレートという固い岩盤で構成されている」と定義されている言葉である。

IHO(国際水路機関)では、海底地形の名称として「海溝」を「細長く、特徴的に非常に深い、非対称断面を示す海底の凹地。比較的急峻な斜面を有する」と定義しているが、プレートテクトニクスでは、「海溝は、海洋プレートが他のプレートの下に沈み込む場所」と定義されている。海洋プレートは陸側のプレートに比べて比重が重く堅固であるため、海洋プレートが陸側のプレートの下に沈むこむ。

プレートが海溝から他のプレートに斜めに沈み込んでいく場所では、「プレート同士の接触によって地殻の歪みがたまっていく」が、この歪みが解消される動きによって大地震が起きる。これが、「海溝型地震」と呼ばれるものであり、「断層」によって起きる「断層型地震」に比べ、地震のエネルギー、規模は遙かに巨大なものとなる。

海溝と同様の海底構造に「南海トラフ巨大地震」で多くの人の知るところとなった「トラフ」がある。一般的にトラフは、「舟状海盆」というその訳語で明らかなように、「急峻な斜面を持つ海溝」と異なり「なだらかな斜面をもつもの」とされていて、また深さ6000m以上の海溝と区別され「深さ6000m未満の海底構造」である。

1.地震の分類

「CA34 『断層型地震』に備えるキャプティブ」に記したとおり、地震は発生原因によって大きく二つに別けられる。複数のプレートの境界で発生する地震「海溝型地震」、そして同一プレートの内部にできた断層で発生する地震で「断層型地震」と呼ばれるもの、この二つである。前者は複数のプレートによって生じる地震であり「プレート間地震」、後者は同一プレートの内部にできた断層で発生する地震であるため「プレート内地震」とも呼ばれるが、地震の起因を示すという点から、一般的には「海溝型地震」、「断層型地震」と呼ばれることが多い。

こういう呼称とは別に「直下型地震」(内陸地震)という分類を用いることもある。居住地域の直下で起こる震源の浅い地震のことを指し、多くは「断層型地震」であるが、地域によっては「断層型地震」ではなく「海溝型地震」として発生することもある。関東地方南部で繰り返し発生してきたマグニチュード(M)7クラスの大地震は、総称して南関東直下地震と呼ばれるが、これは「断層」が動いて地震が起きる「断層型地震」ではなく、関東地方の土台「北米プレート」に海側の「フィリピン海プレート」が沈み込んでいる場所、「相模トラフ」で発生する「海溝型地震」である。

2.マグニチュード

地震の大きさは「マグニチュード」という指標で表わされているが、この「マグニチュードが持つ意味」が一般的にはあまり理解されていないように感じている。お客様との話のなかでも「マグニチュード7とマグニチュード8は、倍ぐらいの違いですかね」という会話が幾度かあったことを記憶しているからである。

マグニチュードの数字が増えることで、どれくらい地震の規模が大きくなるのか、どれほど地震のエネルギー量が増えていくのか。小数点以下、マグニチュード0.1の差では、実は約1.4倍、マグニチュード0.2の差になると約2倍(101.5×0.2 = 100.3 ≒ 1.995)となる。そして、それが整数、例えばマグニチュード7とマグニチュード8の「マグニチュード1の差」では、マグニチュードの値の増加は測定された振幅の10倍の増加を示した数値とされているので、「マグニチュードが1増えると、10√10 =約30倍、2増えると(10√10)2 = 約1000倍、そのエネルギー量は増える」のである。つまりマグニチュード6.0と8.0の地震の規模は、約1000倍違うということである。

また、地震が発生した際、気象庁から発表されるマグニチュードは小数第1位まで発表されている。つまり、「M8.0」と発表された場合、その地震の規模は「M7.95〜M8.05の範囲内にある」と考えられる。M7.95とM8.05、この差はたった「0.1」であるが、マグニチュード0.1の差は実はエネルギーでは約1.4倍の差、「気象庁の発表の段階」で既に「地震の規模は最大で約1.4倍の開きがある」ということなのである。

また、地震のエネルギーは、地中、地表面を拡散されていくため地震のエネルギーを正確に測る方法が実は存在しておらず、あくまでも概算に近い数字であることにも注意が必要である。日本語の「マグニチュード」を英文に翻訳する場合、例えば、M7.4を翻訳する場合、その英文は「magnitude 7.4 on the Richter scale」となる。このマグニチュード(magnitude)とは、その訳語の後半部分に名前を残す、米国の地震学者チャールズ・リヒター( Richter)が地震のエネルギー量を表す指標値として考案、1935年に発表した値のことである。

「六甲・淡路島断層帯」の横ずれによって発生した「断層型地震」であった、1995年の阪神・淡路大震災は「直下型」であったためあれほど甚大な被害を出したが、そのマグニチュードの値は7.3であった。一方、日本周辺での観測史上最大の地震であった東日本大震災のマグニチュードは9.0であり、そのエネルギー量の差は300倍以上あったということである。プレート境界で発生する「海溝型地震の巨大さ」が理解されるであろう。

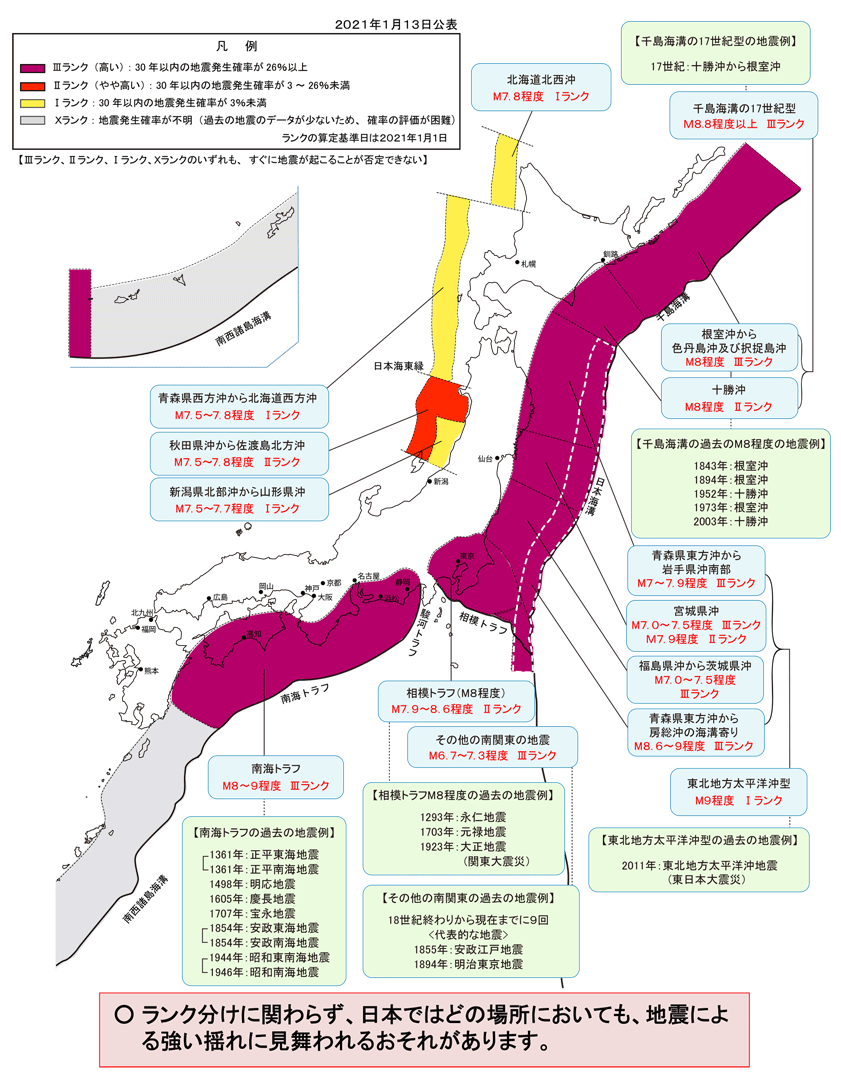

政府「地震調査研究推進本部」のホームページにあるものが、東日本大震災、南海トラフ巨大地震等を引き起す「海溝型地震」を記した「主な海溝型地震の評価結果」である。

On the website of the Government’s ” Earthquake Research Promotion Headquarters” is the “Evaluation Results of Major Trench-Type Earthquakes”, which describes the “trench-type earthquakes” that triggered the Great East Japan Earthquake and the Nankai Trough Mega Earthquake.

主な海溝型地震の評価結果

Evaluation Results of Major Trench-Type Earthquakes

出典:「主な海溝型地震の評価結果」(地震調査研究推進本部)

Source: “Evaluation Results of Major Trench-Type Earthquakes” (Earthquake Research Promotion Headquarters)

3.「海溝型地震に備えるキャプティブ」の特徴

海溝型の最大クラスの地震は、発生頻度は極めて低いものの、仮に発生すれば、広域にわたり甚大な被害が発生する。大きな地震のため地震の揺れによって建物、財物が被害を受けるが、2011年の東日本大震災の「津波」でもたらされた甚大な被害でも明らかなように、陸地から離れた場所に「海溝=震源」があるため、「揺れよりも津波」が最も警戒、対処しなければならないリスクなのである。

当然、キャプティブ・プログラムの対象とする「地震保険」でも、「津波リスクを手厚く補償する保険内容」にすべきであり、津波特有の補償条件等も、「キャプティブからの再保険を引受けるロンドン・マーケットの再保険会社」と交渉して、日本の元受保険会社では一般的に提供されない補償内容を付加することを検討すべきであると考える。

つまり、「津波」が低地に流れ込んだ場合、「長期間水が引かないリスク」があることに注意が必要ということである。「長期間水が引かない=インフラがダウンする」ということであり、長い間「電気」、「水」がストップする可能性や、事業所が工場であれば、工場は操業できても工場から長期間「製品を搬出できないリスク」があることに注意が必要である。

また、「被害も非常に大きくなる」ため、地震保険の補償金額も最大限確保可能な金額にしておく必要がある。そのためには、キャプティブからの再保険も単純な「クオーター・シェア」でおこなうのではなく、「レイヤリング」を使って高額補償枠の確保ができやすいようにすることも必要である。こういう点からも、キャプティブのコンサルティング会社は、非常に専門的な保険技術も持ち合わせている会社にすることが重要であるということがご理解頂けるであろう。

今回のまとめ

「断層型地震」に比べて規模が大きいのが「海溝型地震」であり、地震波の大きさは断層型地震の数十倍以上になる。また、海溝型地震によって引き起される「津波」は、東日本大震災でも甚大な被害を与えることになった。

東日本大震災までの多くの地震では、地震被害は「財物」が地震の揺れ、衝撃によって損害を受けることが多かったため、企業が一般的に購入してきた「地震保険(火災保険+地震補償特約)」では、「物的損害リスク(財物損壊リスク)」(英文では「Property Damage(プロパティ・ダメージ):PD」と呼ばれる)に限られていて、「地震保険=物的損害リスクへの補償」と見なされてきた。

無論、「津波補償」も「地震補償特約」の補償条項には入っているので、「補償金額までの損害であれば津波による損害も補償されること」になっている。しかし、問題はその「補償額」である。「津波」は「物的損害」を与えるが、それに付随して起きる派生的な大きな被害が発生する可能性のあるものが、「水が引かないリスク」である。企業の事業所、工場が津波によって浸水被害を受けることに加え、更に問題となるのが「道路、変電所等のインフラストラクチャー」が津波被害を受けて、「事業の継続が難しい状況」に立たされることである。

「海溝型地震」によって発生した大津波によるこれらの損害だけではなく、都市の直下で起きる「断層型地震」によって「堤防の破損、決壊」が起き、外水氾濫が発生、長く水が引かず事業の継続に大きな影響を与えることも考えられる。特に、東京の下町、また水都と言われる大阪は低地が多く、元々海であった場所を干拓して都市化しているため津波による外水氾濫の危険性が高い。

名古屋でも同様である、縄文時代中期には、名古屋の中央部から西側は岐阜県の大垣市付近まで「海」であった。河川の土砂堆積によって海岸線は徐々に南下していき、中世頃には「中川区」までが陸地となった。その後、新田開発、干拓が更に進んで今の名古屋市が形成された。このため、名古屋市の西側は「海抜の低い土地」であり、「津波」の被害に遭いやすい地形となっている。それを示すように、名古屋市のホームページ(「防災・危機管理」の箇所)には次のような記述がある。

南海トラフ巨大地震が発生した場合に津波浸水が予想される、中村区、瑞穂区、熱田区、中川区、港区、南区及び緑区に海抜を表示し、普段からの防災意識の高揚と発災時の迅速な避難の目安としていただけるよう、海抜表示を実施しています。

こういう津波による外水氾濫の危険が高い地では、とりわけ重要な「地震保険」の補償が「地震による事業の継続に問題が起き、事業収益が落ち込むリスク」に対応する補償、「事業中断リスク」(英文では「Business Interruption(ビジネス・インタラプション):BI」である。

先述の通り、しかし、日本では「地震保険=物的損害リスクへの補償」と見なされてきたため、損害保険会社からこの補償を受けることは一般的ではない。また、保険会社側にとっても「地震保険の引受キャパシティ(引受力=海外の再保険会社から提供されている再保険)」は、非常に大事な「虎の子」である。この「事業の中断による収益低下リスク」(英文では「Business Interruption(ビジネス・インタラプション):BI」を引き受けると引受リスクが増し「再保険キャパシティ」を大きく使うことになるから、この「事業の中断による収益の低下リスク」を補償をすることはしてこなかった。

このように、日本で一般的に販売されている地震保険は「物的損害」のみを補償するものであるが、欧米では、ごく普通に販売されている地震保険は「物的損害:PD(Property Damage)」に加え、この地震による「事業の中断による収益低下リスク」(英文では「Business Interruption(ビジネス・インタラプション):BI」)が補償されているものである、「物的損害リスク」だけでは片手落ちで「事業の中断による収益低下リスク」が無ければ「地震保険としての意味が無いから」である。

キャプティブを設立する大きなメリットはここにある。日本では一般的に手に入らない「地震保険の補償:事業の中断による収益低下リスク」をキャプティブからの再保険を受けるロンドン・マーケットの再保険会社で確保して日本の元受保険会社に提供する、このことによって、地震による「事業の中断による収益低下リスク」を補償することができるからである。

感染患者数は増えているが、「オミクロン株」へと「コロナ禍の弱毒化」が言われるようになってきて、コロナ禍の先に薄日が見えるようになってきたいま、「事業再構築」のためにも、この大きなメリットを活用して、「コロナ禍以上の最大級のリスク、巨大地震リスクに備える」ためキャプティブの設立を検討する良い機会ではないだろうか。

執筆・翻訳者:羽谷 信一郎

English Translation

Captive (CA) 35 – Captives for “a massive trench earthquake of the Great East Japan Earthquake magnitude

In this column, I have used the term “plate” in the past, but to reiterate its meaning, the term “plate” is defined in “plate tectonics,” an earth science theory developed in the 1960s to explain the theory of continental movement and the causes of trench earthquakes, as “the surface of the earth’s crust, or earth’s surface, is made up of more than a dozen plates of solid rock”.

The International Hydrographic Organization (IHO) uses the term “trench” as a name for a submarine feature: “a long, narrow, characteristically very deep, asymmetrical cross-sectional depression in the sea floor”. However, plate tectonics defines “A trench as a place where an oceanic plate subducts beneath another plate”. Oceanic plates are heavier and more rigid than land-based plates, so they sink beneath land-based plates.

Where a plate sinks diagonally from one trench to another, “crustal strain accumulates as the plates come into contact with each other”, and it is this movement that causes major earthquakes. This is called a “trench-type earthquake”, and the energy and scale of the earthquake is far greater than that of a “fault-type earthquake”, which is caused by a fault.

Similar to trenches, there is a submarine structure called a trough, which is well known to many people because of the huge Nankai Trough earthquake. In general, troughs are considered to be “gently sloping” as opposed to “steeply sloping trenches”, as is clear from the translation of the term “boat basin”. It is also distinguished from trenches over 6,000m deep, which are “submarine structures less than 6,000m deep”.

1. Classification of earthquakes

As described in CA34 “Captives for fault earthquakes”, earthquakes can be divided into two main categories according to their cause. There are two types of earthquakes: trench earthquakes, which occur at the boundaries of several plates, and fault earthquakes, which occur on faults within the same plate. The former are called “interplate earthquakes” because they are caused by multiple plates, and the latter are called “intraplate earthquakes” because they are caused by faults within the same plate. However, in terms of the origin of the earthquake, they are generally called “trench earthquakes” and “fault earthquakes”.

Apart from these terms, the classification “direct earthquake” (inland earthquake) is sometimes used. These are earthquakes with shallow epicentres that occur directly beneath the area of residence, and are mostly fault earthquakes, although in some areas they may occur as trench earthquakes rather than fault earthquakes. The magnitude 7 class earthquakes that have repeatedly occurred in the southern part of the Kanto region are collectively called the South Kanto Direct Subduction Earthquakes, but these are not fault earthquakes, in which a fault line moves to cause an earthquake, but rather earthquakes that occur in the Sagami Trough, the area where the North American Plate, the foundation of the Kanto region, is subducted by the Philippine Sea Plate on the ocean side as a trench earthquake that occurs at the Sagami Trough.

2. Magnitude

The size of an earthquake is expressed by an index called “magnitude”, but I feel that the meaning of “magnitude” is not well understood in general. I remember having a conversation with a client who said, “Is the difference between a magnitude 7 and a magnitude 8 about twice as great?”

How much does an increase in the magnitude number increase the size of the earthquake, and how much does it increase the amount of energy in the earthquake? To the nearest decimal point, a difference of 0.1 magnitude is actually about 1.4 times the magnitude, and a difference of 0.2 magnitude is about twice the magnitude (101.5 x 0.2 = 100.3 ≈ 1.995). And if it is a whole number, e.g. a “magnitude 1 difference” between magnitude 7 and magnitude 8, the increase in the magnitude value is taken to be a number representing a 10-fold increase in the measured amplitude, so that “an increase in magnitude of 1 means an increase of 10√ 10 = about 30 times, and an increase of 2 means an increase of (10√10)2 = about 1000 times the amount of energy”. This means that the magnitude of an earthquake of magnitude 6.0 and 8.0 is about 1000 times different.

Also, when an earthquake occurs, the JMA announces the magnitude to one decimal place. In other words, when an earthquake is announced as “M8.0”, the magnitude of the earthquake is considered to be in the range of M7.95 to M8.05.The difference between M7.95 and M8.05 is only 0.1, but the difference in magnitude of 0.1 is actually about 1.4 times the difference in energy. At the time of the JMA’s announcement, the magnitude of the earthquakes was already about 1.4 times greater than that of the previous one.

It should also be noted that there is no way to accurately measure the energy of earthquakes, as it diffuses through the ground and over the surface of the earth, so the figures are only approximations. When translating the Japanese word “magnitude” into English, for example M7.4, the English sentence would be “magnitude 7.4 on the Richter scale”. The magnitude is a value devised by the American seismologist Charles Richter, whose name appears in the second half of the translation, and published in 1935 as a measure of the energy of earthquakes.

The Great Hanshin-Awaji Earthquake of 1995, which was a fault-type earthquake caused by the lateral displacement of the Rokko-Awaji Island Fault Zone, was a direct earthquake and caused enormous damage, but its magnitude value was 7.3. On the other hand, the magnitude of the Great East Japan Earthquake, the largest earthquake ever recorded in the vicinity of Japan, was 9.0 on the Richter scale. The difference in energy is more than 300 times greater than the magnitude of the Great East Japan Earthquake. This will help us to understand the enormity of trench earthquakes that occur at plate boundaries.

3. Characteristics of the “Captive for Trench Earthquakes”.

The largest trench type earthquakes occur very infrequently, but if they do occur, they can cause enormous damage over a wide area. Although large earthquakes can cause damage to buildings and property, as evidenced by the devastation caused by the tsunami that followed the Great East Japan Earthquake in 2011, tsunamis rather than tremors are the most important risk to be aware of, as trenches are located far from land.

Naturally, earthquake insurance policies under the captive program should be designed to cover tsunami risks more extensively, and tsunami-specific coverage conditions should be negotiated with the London Market reinsurers that underwrite the reinsurance from the captive to add coverage that is not generally provided by Japanese primary insurers.

In other words, it is important to note that there is a risk that the water may not recede for a long period of time if a tsunami flows into a low-lying area. If your business is a factory, there is a risk that you may not be able to remove products from the factory for a long period of time, even if the factory can operate.

In addition, the amount of earthquake insurance coverage should be the maximum amount that can be secured because “the damage will be very large”. In order to achieve this, reinsurance from captives should be layered, rather than simply quarter-shared, in order to facilitate the securing of high value coverages. In this respect, it is important to ensure that the captive’s consulting company has very specialist insurance skills.

Summary of this issue

Trench earthquakes are much larger than fault earthquakes, with seismic waves tens of times larger than those of fault earthquakes. Tsunamis, which are triggered by trench earthquakes, also caused extensive damage in the Great East Japan Earthquake.

In most of the earthquakes before the Great East Japan Earthquake, property was often damaged by the shaking and impact of the earthquake, so the earthquake insurance (fire insurance plus earthquake compensation rider) that companies have generally purchased has been limited to “property damage risk” (called “property damage” in English), and has been regarded as “earthquake insurance = compensation for property damage risk”.

Of course, tsunami coverage is also included in the special clause for earthquake coverage, which means that tsunami damage is covered as long as the damage is up to the coverage amount. The question, however, is the amount of compensation. A tsunami causes property damage, but the risk that the water will not recede is an additional risk that can cause significant damage. In addition to the inundation of a company’s offices and factories by a tsunami, a further problem is the damage to roads, substations and other infrastructure, which can make it difficult to continue operations.

In addition to the damage caused by tsunamis triggered by trench earthquakes, fault earthquakes that occur directly beneath a city can cause levees to break or fail, leading to flooding and a long delay in releasing the water, which can have a significant impact on business continuity. The risk of tsunami inundation is particularly high in the downtown area of Tokyo and in Osaka, which is known as the “water city” because many low-lying areas have been reclaimed from the sea and are now urbanized.

The same is true of Nagoya. In the mid-Jomon period, the sea extended from the centre of Nagoya to the western side near Ogaki City in Gifu Prefecture. The coastline gradually moved southwards as rivers deposited sediment, and by the Middle Ages, the area up to Nakagawa Ward had become land. This was followed by further development of rice paddies and land reclamation to form the present-day city of Nagoya. As a result, the western part of the city is “low land” and prone to tsunamis. As an indication of this, the Nagoya City website (under “Disaster Prevention and Risk Management”) has the following statement

In the event of a major earthquake in the Nankai Trough, the elevation of the sea is displayed in Nakamura, Mizuho, Atsuta, Nakagawa, Minato, Minami and Midori wards, where tsunami inundation is expected.

In such areas where the risk of flooding due to tsunamis is high, it is particularly important to ensure that earthquake insurance covers the “risk of Business Interruption” (BI)in English.

As mentioned above, in Japan, however, it is not common for non-life insurance companies to provide this coverage, as earthquake insurance is regarded as compensation for the risk of property damage. Also, for the insurance companies, “earthquake insurance underwriting capacity” (reinsurance provided by overseas reinsurers) is a very important “precious thing”. The risk of loss of income due to business interruption (BI) would increase the underwriting risk and use a large amount of reinsurance capacity. This is why we have not covered this “risk of loss of earnings due to business interruption”.

Thus, earthquake insurance commonly sold in Japan covers only “property damage”, whereas in Europe and the United States, earthquake insurance commonly sold in Japan covers not only “property damage (PD)” but also the “risk of loss of profits due to business interruption” (in English, “business interruption risk”). Business Interruption (BI)” in addition to “Property Damage (PD)”, because “Property Damage” alone is not enough and without “Business Interruption (BI)”, “Earthquake Insurance is meaningless”.

Herein lies the major advantage of establishing a captive. The London Market reinsurance companies that receive reinsurance from the captive will secure the “earthquake cover: risk of loss of earnings due to business interruption”, which is not generally available in Japan, and provide this cover to the Japanese primary insurers. This would cover the “risk of loss of earnings due to business interruption” caused by the earthquake. Although the number of infected patients is increasing, the “weakening of the coronavirus” to the “Omicron strain” is being called for, and the sun is beginning to set on the corona disaster.

In order to “restructure” the business, it would be a good time to consider setting up a captive in order to take this significant advantage and “prepare for the biggest risk of all, the risk of a huge earthquake”.

Author/translator: Shinichiro Hatani