キャプティブ 2022.12.28

CA46 巨大地震対策の切り札、「レイヤリング・キャプティブ」

目次

For those who prefer to read this column in English, the Japanese text is followed by a British English translation, so please scroll down to the bottom of the Japanese text.

「キャプティブ」が、日本企業にとってその効用を最も発揮する対象は「地震リスク」をおいて他に無い。その対象とする地震の規模が大きければ大きいほど効用は高い。地震による被害、損害の規模が大きく、「日本の損害保険会社が用意できる補償枠では到底足りない補償枠を『海外から調達することができるから』」である。

当時、世界最大と言われた米国最古の株式損害保険会社を傘下に持った保険コングロマリットCIGNA、その本社キャプティブ部門の主要幹部として多くのキャプティブの設立、運営に携わり、現在、日本で「キャプティブ・コンサルティング会社、株式会社グローバル・リンク」を経営、長くキャプティブ・ビジネスに携わってきた経験から、筆者はそう言い切れる。

地震の種類は、海側プレートの変動を受け陸上の断層が連動して発生する「断層型地震」と、海側プレートの動きそのものから発生する「海溝型地震」に大別されるが、「海溝型地震」は地球規模の地殻変動によって発生するため巨大な地震になることが多い。「大規模な海溝型地震に備えるためのリスク対応策として『巨額の地震保険補償枠を用意できるキャプティブ』が必須」とされる所以である。

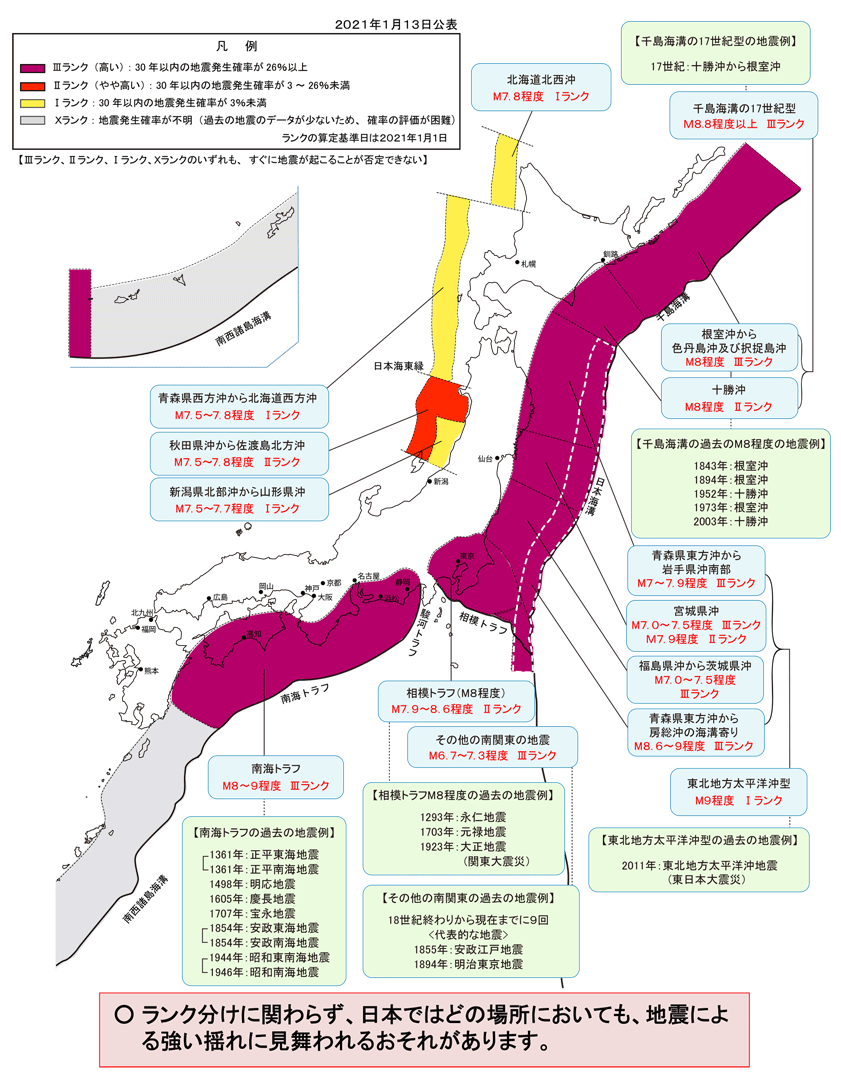

出典:「主な海溝型地震の評価結果」(地震調査研究推進本部)

Source: “Evaluation Results of Major Trench-Type Earthquakes”

(Earthquake Research Promotion Headquarters)

1.日本海溝・千島海溝沿いの巨大地震

現在、その発生が最も懸念されている「海溝型地震」は、昨年暮れ、2021年12月21日政府中央防災会議が被害想定を発表した「日本海溝・千島海溝沿いの巨大地震 」である。想定される地震規模は「マグニチュード8.8以上」であり、同報告で「Ⅲランク:地震の発生確率が高く30年以内の地震発生率が26%以上」とされている地震である。

「日本海溝・千島海溝沿いの巨大地震」のうち、「①千島海溝沿いの巨大地震」とは、海側の「太平洋プレート」が陸側の「北米プレート」の下に沈み込んでいる千島海溝付近で、300年から400年の周期で大津波を伴い発生している巨大地震のことを言う。

一方、「②日本海溝沿いの巨大地震」の代表例は2011年の東日本大震災であるが、発生が懸念されている巨大地震は、「北海道の沖合から岩手県沖にかけてマグニチュード9.1規模の巨大地震が発生して、岩手県宮古市では29.7mの大津波が発生する」と想定されている。この地震による最悪のシナリオは冬の深夜に地震が起きた場合である。住民避難も困難であるため、犠牲者は北海道で13万7千人、青森県4万1千人、岩手県1万1千人、宮城県8500人、他県も合わせて合計19万9000人、経済被害は31兆3千億円に及ぶと推定されている地震である。

北海道襟裳岬の東沖合を震源域と想定している「①千島海溝沿いの巨大地震」は、「②日本海溝沿いの巨大地震」よりも地震の規模は更に大きく、東日本大震災を上回るマグニチュード9.3の地震と想定されている。この超巨大地震では、最大27.9mの大津波が押し寄せ、犠牲者は北海道で8万5千人、他県も含めて合計で10万人、経済被害は16兆7千億円に及ぶと推定されている。

出典:内閣府公式WEBサイト 北海道・三陸沖後発地震注意情報の解説ページ

Source: Cabinet Office official website, Hokkaido/Sanriku-oki Late-Seismic Earthquake Warning Information Explanation Page.

2.「北海道・三陸沖後発地震注意情報」

2011年3月11日に発生した東日本大震災では、直前の3月9日にマグニチュード7.3の地震が起きた。このことから、「マグニチュード7クラスの地震が発生した場合、その後に『マグニチュード9クラス』の巨大地震が『後発地震』として発生する可能性が高い」として、政府、気象庁は「日本海溝・千島海溝沿いの巨大地震」へ備えるため「北海道・三陸沖後発地震注意情報」の提供を2週間前の12月16日から開始した。

ただ、筆者の目には「玉虫色の注意喚起情報」として映る。北海道から千葉県までの計182市町村対象として、その太平洋沖で、マグニチュード7クラスの地震が発生した場合、その後のマグニチュード9クラスの「後発地震」に対する注意喚起を求めるものであるが、「発生後1週間程度の期間、揺れを感じたり、津波警報が発表されたときは、ただちに避難できる態勢をとるよう呼びかける」のみで、「住民に事前の避難は求めないものだから」である。

気象庁の公式WEBサイトにある、本年2022年12月07日気象庁地震火山部が発表した「南海トラフ地震関連解説情報」には、「南海トラフ沿いの大規模地震(M8からM9クラス)は、『平常時』においても今後30年以内に発生する確率が70から80%であり、昭和東南海地震・昭和南海地震の発生から既に70年以上が経過していることから切迫性の高い状態です。」と記されているが、本コラムの冒頭の引用図、「主な海溝型地震の評価結果」(地震調査研究推進本部)には、「日本海溝・千島海溝沿いの巨大地震 」の発生確率は「Ⅲランク:地震の発生確率が高く30年以内の地震発生率が26%以上」とされていることがその背景にあるためであろう。

しかし、「リスクマネジメント」では、「分析してリスクが顕在化する可能性がある場合、その対応を明確にすることが必須」である。にもかかわらず、「『注意喚起』はするが、『その後の対応は自分で判断せよ』とは、住民側からすると『じゃあ、どうしたら良いの?』という疑問を持つばかりでかえって混乱を招くのではないか」と感じるのは筆者だけであろうか。

3.マグニチュード

地震の規模・大きさを示す数値は「マグニチュード」である。その大きさが際立った最近の地震が、2011年3月11日に発生した「海溝型地震」である東日本大震災であった。マグニチュードは9.0。

一方,内陸にある断層が動くことによって発生する「断層型地震」。その一例である1995年1月17日に発生した「阪神・淡路大震災」は、甚大な被害を与えた地震であったがマグニチュードは7.3であった。マグニチュード9.0とマグニチュード7.3、数値としては1.7の差であり、一見規模に大きな差は無いように見える。

しかし、マグニチュードは、7から8へ、1つ大きくなるとそのエネルギー量の増え方は単なる「プラス1」ではない、エネルギー量は一気に30倍になるのである。更に、マグニチュードが2つ違うと地震のエネルギー量は約1,000倍(≒30×30倍)、マグニチュードが3つ大きくなると地震のエネルギーは実に約30,000倍(≒30×30×30倍)になるのである。甚大な被害をもたらした阪神・淡路大震災のマグニチュードは7.3、東日本大震災のそれは9.0、エネルギー量の差は300倍であった。

小数点以下、例えばマグニチュード0.1の差でもエネルギー量では約1.4倍の差、マグニチュード0.2の差では約2倍(101.5×0.2 = 100.3 ≒ 1.995)となる。未曾有の被害をもたらした東日本大震災のマグニチュードは9.0を越えた地震であったが、「①千島海溝沿いの巨大地震」のマグニチュードは9.3と推計されている。ということは、この計算式から「東日本大震災の約2.8倍のエネルギー量を持つ超巨大地震」であることが解る。

4.レイヤリング・キャプティブ

冒頭述べたとおり、「海溝型地震」の場合、被害が甚大となるため、地震保険による備えとしては、「できるだけ支払限度額を高く手配する必要」がある。しかし、地震国日本では地震キャパシティ(引受力)に対して多くのニーズがあるため、十分な地震保険キャパシティの確保は非常に困難であり、キャプティブの力を借りる必要がどうしても出てくる。キャプティブを設立することによって、海外の再保険会社から日本で調達できない大きな地震キャパシティ(引受力)を再保険で得るようにするためである。

このキャプティブを設立する際、「より多くの地震保険キャパシティ」を確保するためには、再保険会社は一社ではなく、複数以上のサポートを確保する必要がある。

このためには、「単純な地震保険の再保険手配」ではなく、キャプティブからの再保険手配(元受保険会社から見た場合、「再々保険」)では、「レイヤリング」(階層引受)という損害保険の専門的な引受技法によっておこなう必要がある。地震保険の総補償額を金額で幾つもの「階層」に別け、それぞれの階層ごとに再保険会社を決める、また同じ金額の階層であってもそのなかで更に割合を決め細分化して、より多くの再保険会社による「分担引受」を可能にする再保険の引受手法のことである。

だからこそ、地震保険のように「大規模なキャパシティ」を確保する必要があるキャプティブを設立する場合には、再保険に関しても豊富な知見を持ち、再保険マーケットにも強固なネットワークを有する高度専門性を持つキャプティブ・コンサルティング会社を起用することが重要なのである。

今回のまとめ

日本で地震保険を引受ける保険会社である「元受保険会社」が、「大きな地震保険の補償枠」が提供できて一社単独で引受けることが可能であれば、「地震保険を非常に簡便に手配できる」というメリットはある。しかし、「果たして、保険料は低廉か?」という疑問が出てくる。

これまで、グローバル・リンクが携わった案件では、「その全てで、海外から得た再保険の方が遙かに低廉であった」という事実がある。だからこそ、グローバル・リンクは、「世界最大級の海外の再保険会社から低廉な地震保険を産地直送するキャプティブ・プログラム」をリスクマネジメントの切り札として推奨してきたのである。

なかでも、「地震保険補償枠が非常に大きな場合」は、「レイヤリング(レイヤー方式)」再保険手配による「内外価格差」は非常に大きなものであった。

「レイヤリング(レイヤー方式)」とは、保険金額やてん補限度額が大きくて、引受保険会社が、一社単独では全額の引受けが難しいリスクを「保険金額やてん補限度額を数段階以上の階層(レイヤー)に分け、それぞれの再保険を引受ける再保険会社が独立して階層(レイヤー)毎に自らの引受条件を決め、その階層部分のみを引き受ける方式」である。

このレイヤリング(レイヤー方式)では、レイヤーの上層部(高額な補償額)または下層部(低額補償額)か、その再保険会社が得意とする「再保険の補償額」、つまり「各再保険会社の引受姿勢」を良く見極めることが肝心である。こうすることにより、各再保険会社の特長を活かすことができ、キャプティブ保険プログラム全体を低廉な保険料・再保険料で構築することができるからである。

リスクマネジメントの最先端分野であるキャプティブを「企業経営に最も効用を与える存在として更に輝かせる再保険手法がこのレイヤリング」なのである。再保険マーケットに強固かつ豊富なネットワークを有する、高度な専門性を持つキャプティブ・コンサルティング会社の起用が如何に重要かが理解されるであろう。

執筆・翻訳者:羽谷 信一郎

English Translation

Captive (CA) 46 – Layering Captives – the trump card against huge earthquakes

Captives are most effective in seismic risk. The larger the size of the earthquake that causes damage, the greater the benefit. This is because the scale of damage and loss caused by earthquakes increases, and “in order to provide adequate compensation, it is necessary to ‘procure coverage from abroad’, which is far beyond what Japanese non-life insurance companies can provide”.

I can say this from the perspective of the author, who was involved in captives as AVP of the captive division at the headquarters of CIGNA, an insurance conglomerate that owned the oldest US equity property and casualty insurance company, then considered the largest in the world, and now runs a captive consulting company in Japan.

Earthquakes can be broadly classified into two types: fault-type earthquakes, which occur when faults on land move in response to movements of the oceanic plate, and trench-type earthquakes, which are caused by the movement of the oceanic plate itself.

This is why it is said that “A captive with huge earthquake insurance coverage is essential to prepare for large-scale trench earthquakes” as a risk response measure.

1. major earthquakes along the Japan Trench and the Kuril Islands Trench

The trench-type earthquake of greatest concern at present is the Japan Trench and Kuril Islands Trench Earthquake, for which the Central Disaster Management Council of the Japanese Government announced damage estimates at the end of last year, on 21 December 2021. The scale of the earthquake is estimated to be of magnitude 8.8 or greater, and the report states that it is a ” Rank III earthquake: high probability of occurrence with an earthquake occurrence rate of 26% or greater within 30 years”.

Of the “huge earthquakes along the Japan Trench and Kuril Islands Trench”, “(1) huge earthquakes along the Kuril Islands Trench” refers to huge earthquakes that occur near the Kuril Islands Trench, where the Pacific Plate on the ocean side subducts under the North American Plate on the land side, with a period of 300 to 400 years and are accompanied by large tsunamis.

On the other hand, the Great East Japan Earthquake of 2011 is a representative example of (2) a giant earthquake along the Japan Trench, and the giant earthquake feared to occur in the future is assumed to be a magnitude 9.1 earthquake that occurs from offshore Hokkaido to offshore Iwate Prefecture, causing a massive tsunami of 29.7 m in Miyako City, Iwate Prefecture. The worst-case scenario for this earthquake is if it occurs late at night in winter. As it would be difficult to evacuate residents, it is estimated that 137,000 people would be killed in Hokkaido, 41,000 in Aomori, 11,000 in Iwate, 8,500 in Miyagi and a total of 199,000 in other prefectures, and the economic damage is estimated to be 31.3 trillion yen.

The earthquake of magnitude 9.3, which is larger than the Great East Japan Earthquake, is assumed to have an epicentre off the east coast of Cape Erimo in Hokkaido, Japan, and is even larger than the earthquake of magnitude 9.3, which is assumed to have an epicentre in the area of (1) a huge earthquake along the Kuril Islands Trench and (2) a huge earthquake along the Japan Trench. It is estimated that a tsunami of up to 27.9 metres would be triggered by this super-mega earthquake, claiming 85,000 victims in Hokkaido, 100,000 in total including other prefectures, and causing economic damage estimated at 16.7 trillion yen.

2. “Hokkaido/Sanriku Offshore Late-October Earthquake Warning Information”

The Great East Japan Earthquake of 11 March 2011 was preceded by a magnitude 7.3 earthquake on 9 March, so the Government of Japan and the Japan Meteorological Agency (JMA) concluded that “in the event of a magnitude 7-class earthquake, there is a high possibility of a ‘magnitude 9-class’ giant earthquake occurring afterwards as a ‘subsequent earthquake'”. The Japan Meteorological Agency started providing ‘Hokkaido and Sanriku Offshore Subsequent Earthquake Warning Information’ two weeks ago, on 16 December, in order to prepare for “a huge earthquake along the Japan Trench and the Kuril Islands Trench”.

However, in the author’s eyes, it appears as “iridescent warning information”. The information is intended to alert a total of 182 municipalities from Hokkaido to Chiba Prefecture to the possibility of a magnitude 7 earthquake off the Pacific Ocean between Hokkaido and Iwate Prefecture followed by a magnitude 9 earthquake, but it also states that “if you feel a tremor or a tsunami warning is announced for a week, be prepared to evacuate immediately”. However, the JMA only “calls for residents to be prepared to evacuate immediately if they feel a tremor or a tsunami warning is announced during the week”, but “does not require residents to evacuate in advance”.

The “Nankai Trough Earthquake Related Explanatory Information” published by the Earthquake and Volcanoes Department of the JMA on 07 December 2022 on the JMA’s official website states that “a large-scale earthquake (M8 to M9 class) along the Nankai Trough has a 70-80% probability of occurring within the next 30 years even under ” normal conditions “, and that the Showa Tonankai Earthquake The Showa Tonankai and Showa Nankai earthquakes have already occurred more than 70 years ago and are therefore highly imminent.” This is probably due to the fact that the probability of a major earthquake along the Japan Trench and Kuril Islands Trench is ranked as “Rank III: Probability of earthquake occurrence is high and the probability of an earthquake occurring within 30 years is 26% or more”.

However, in ‘risk management’, “it is essential to clarify the response” when “there is a possibility that a risk may materialise after analysis”. Despite this, “if you give a ‘warning’ but say ‘you have to decide what to do afterwards’, the residents will only wonder ‘what should I do then?’” This only leads to confusion and confusion on the part of the residents.

3. magnitude

Magnitude is a numerical value that indicates the size and scale of an earthquake. The most recent earthquake that stood out for its magnitude was the Great East Japan Earthquake of 11 March 2011, a trench-type earthquake. It had a magnitude of 9.0.

On the other hand, a ” fault-type earthquake ” is caused by the movement of an inland fault. One example is the Great Hanshin-Awaji Earthquake of 17 January 1995, which caused extensive damage but had a magnitude of 7.3. Magnitude 9.0 and magnitude 7.3 are 1.7 apart, and at first glance there does not appear to be a significant difference in scale.

However, when the magnitude increases by one, from 7 to 8, the increase in the amount of energy is not just “plus one”: the amount of energy increases by a factor of 30. Furthermore, if the magnitude differs by two, the amount of energy of an earthquake increases by about 1,000 times (≈30 x 30 times), and if the magnitude increases by three, the energy of an earthquake increases by about 30,000 times (≈30 x 30 x 30 times). The magnitude of the Great Hanshin-Awaji Earthquake, which caused enormous damage, was 7.3, while that of the Great East Japan Earthquake was 9.0, a difference of 300 times the amount of energy.

The difference in decimal places, for example, a difference of magnitude 0.1 would result in a difference of approximately 1.4 times the amount of energy, while a difference of magnitude 0.2 would result in a difference of approximately twice the amount (101.5 x 0.2 = 100.3 ≈ 1.995). The magnitude of the Great East Japan Earthquake, which caused unprecedented damage, was an earthquake exceeding 9.0, but the magnitude of “(1) A giant earthquake along the Kuril Trench” is estimated to be 9.3, which means that this formula indicates that it is a “super earthquake with approximately 2.8 times the amount of energy of the Great East Japan Earthquake”.

4. layered captive

As mentioned at the beginning of this issue, in the case of a ” trench-type earthquake”, there will be extensive damage, so ” it is necessary to arrange as high a coverage limit as possible” as a preparation by earthquake insurance, but in earthquake-prone Japan there are many needs for earthquake capacity (underwriting capacity), and it is very difficult to secure sufficient earthquake insurance capacity. Therefore, it is inevitably necessary to seek the help of a captive. The purpose of establishing a captive is to ensure that large amounts of capacity that cannot be procured in Japan are reinsured from overseas reinsurers.

It should be obvious that in order to secure “more earthquake insurance capacity” when establishing a captive, it is necessary to secure the support of more than one reinsurance company. To this end, instead of ” simple earthquake reinsurance arrangements”, the reinsurance arrangements from the captive (“retrocession” from the perspective of the primary insurer) need to be made using a specialised property insurance underwriting technique called “layering” (tier underwriting). This is a reinsurance underwriting technique whereby the total amount of earthquake insurance coverage is divided into a number of “layers” by value, and reinsurers are chosen for each layer, or even within the same layer by value, reinsurers are further subdivided to enable “shared underwriting” by a greater number of reinsurers.

This is why, when establishing a captive that needs to secure ” large capacity” such as earthquake insurance, it is important to use a highly specialised captive consulting company with extensive knowledge of reinsurance and a strong network in the reinsurance market. The following is a summary of this report.

Summary of this issue

If a “primary insurer”, the insurance company that underwrites earthquake insurance in Japan, is able to provide a ” large earthquake insurance coverage quota” and underwrite the policy on its own, it would have the benefit of ” making earthquake insurance very easy to arrange”. However, the question arises as to whether the premiums are really low enough.

In all cases in which Global Link has been involved, reinsurance obtained from overseas has been far less expensive. That is why Global Link has recommended a “captive programme of low-cost earthquake insurance direct from the world’s largest overseas reinsurers” as a key risk management tool.

In particular, the “layered’ reinsurance arrangements” have resulted in significant price differentials between domestic and foreign reinsurers in cases where the earthquake insurance coverage is very large.

“Layered reinsurance” refers to a system whereby risks with large insurance amounts and coverage limits that are difficult for an underwriting company to underwrite in full on its own are divided into several or more layers of insurance amounts and coverage limits, and the reinsurers underwriting each layer independently determine their own underwriting terms and conditions for each layer. The reinsurance company underwriting each layer independently determines its own underwriting conditions and underwrites only that part of the layer.

In this layering method, it is essential to carefully assess whether the reinsurers underwrite the upper layer (high coverage) or the lower layer (low coverage), and the reinsurance coverage in which the reinsurers specialise, in other words, the underwriting attitude of each reinsurance company. This will enable each reinsurer to make the most of its strengths and build an overall captive insurance programme with low premiums and reinsurance costs.

This layering is a reinsurance approach that makes captives, a cutting-edge area of risk management, “shine even brighter as the most beneficial to corporate management”. The importance of using a highly specialised captive consulting company with a strong and extensive network in the reinsurance market will be understood.

Author/translator: Shinichiro Hatani